Trending

Written by: John Lin

Investors are asking tough questions about China as hope for its post-COVID resurgence gives way to concern about its economy. Despite the uncertainties, we think China remains investible and a value-oriented approach that targets companies aligned with government policies can deliver long-term results.

In January, it appeared as if 2023 was shaping up to be China’s year. The economy reopened to great fanfare after a prolonged lockdown and consumer spending surged. But unlike in many Western economies, aggressive government stimulus did not follow, and momentum faded. On the corporate side, sporadic lockdowns over the past three years kept the recovery fragile. It has since been weakened further by policymakers’ efforts to delever the property sector, which have slowed economic growth. Chinese stocks reflect the disappointment. The MSCI China A fell by 4.1% in local-currency terms this year through September 20, trailing both developed and emerging stocks in a rising global market.

The government’s restrained response to the challenges the economy faces has left many investors scratching their heads. Why have policymakers relied on such a limited set of stimulative measures that have as yet failed to reignite economic activity?

The answer may have had to do with diverging priorities when 2023 began. Should officials focus on the long-standing structural imbalances that have accumulated over the past two decades of debt-financed spending on infrastructure and property? Or should they address more immediate issues, including weak consumer and business confidence and slower growth? Consensus has been hard to come by, making it difficult to rally around cohesive and decisive policy action.

Facing the Music

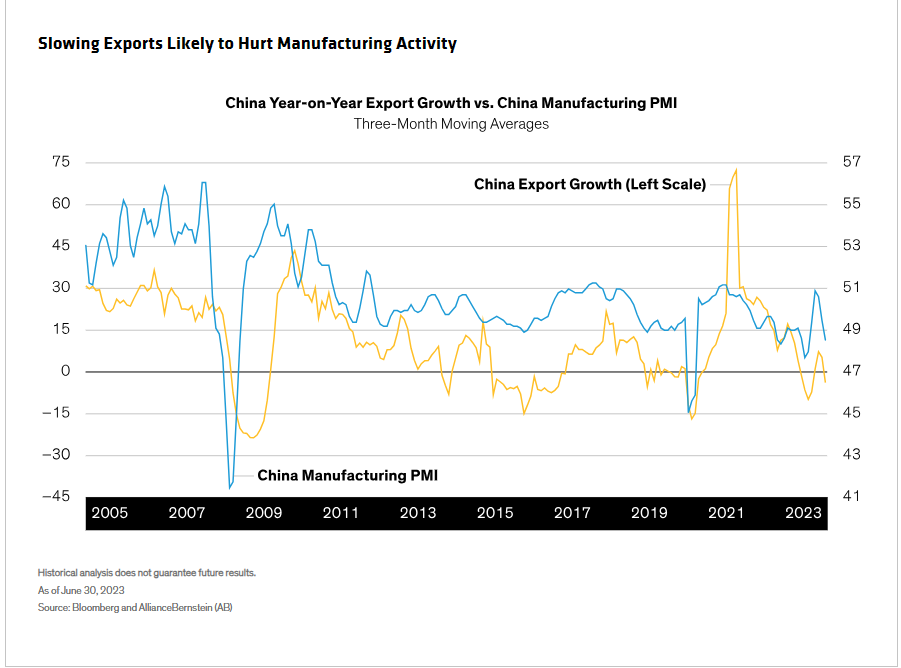

But the risks posed by declining consumer and business confidence and slower growth have become harder to ignore. Manufacturing activity, for example, has been declining for months (Display)—partly the result of slowing export growth—while activity in the services sector, which includes construction, has also dipped.

In residential property markets, sales are down and real, or inflation-adjusted, prices have started to decline. That’s helped to provoke a more pointed policy response from the People’s Bank of China, which slashed interest rates on existing mortgages and reduced down payment requirements for first and second home purchases.

The New Normal: Slower Growth

For investors, it all adds up to yet more uncertainty and a rocky road ahead. China faces multiple near- and medium-term growth challenges, with the structural slowdown in the property sector near the top of the list. Highly levered firms may face distress and property developer defaults could hurt local government finances or cause some banking stress. It will take time before the resulting economic contraction runs its course.

Here’s one thing we’re not expecting: systemic collapse. China’s banking system has grown more resilient over the past decade, thanks to prudent regulation. It has substantial capital buffers, and the central bank has been swift in responding to bank failures. Local government debt, another source of investor angst, is still sizable, but growth has slowed over the past decade. If necessary, we believe those obligations will be assumed—reluctantly, to be sure, but assumed nonetheless—by the central government, which has a pristine balance sheet.

It’s also worth pointing out that slower growth is an inevitable consequence of China’s ongoing transition to a more balanced economic model. Moving away from heavy industry and exports results in slower growth until those resources are redeployed.

For equity investors, an ideal outcome would be the stabilization of China’s near-term growth outlook, accompanied by economic reforms that help to shift China from a debt-dependent growth model to one that promotes innovation in consumption, services, technology and manufacturing.

A Value Investing Approach Aligned with Policy Priorities

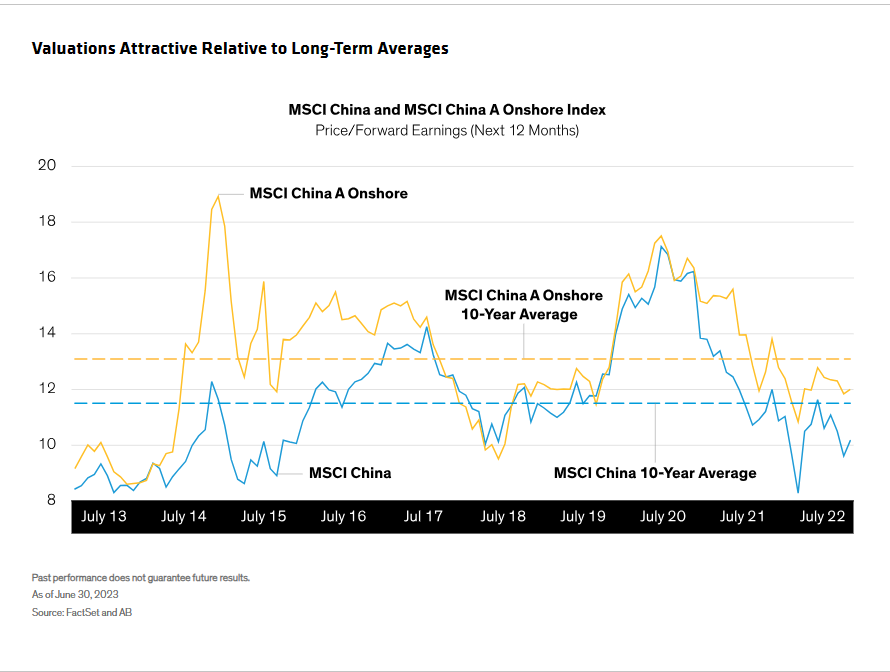

Despite China’s challenges, we believe the long-term outlook for Chinese equities is promising. Valuations in the offshore and onshore markets are attractive versus the last 10 years, in our view (Display). Chinese equities also look cheap relative to the MSCI World Index of developed-market stocks.

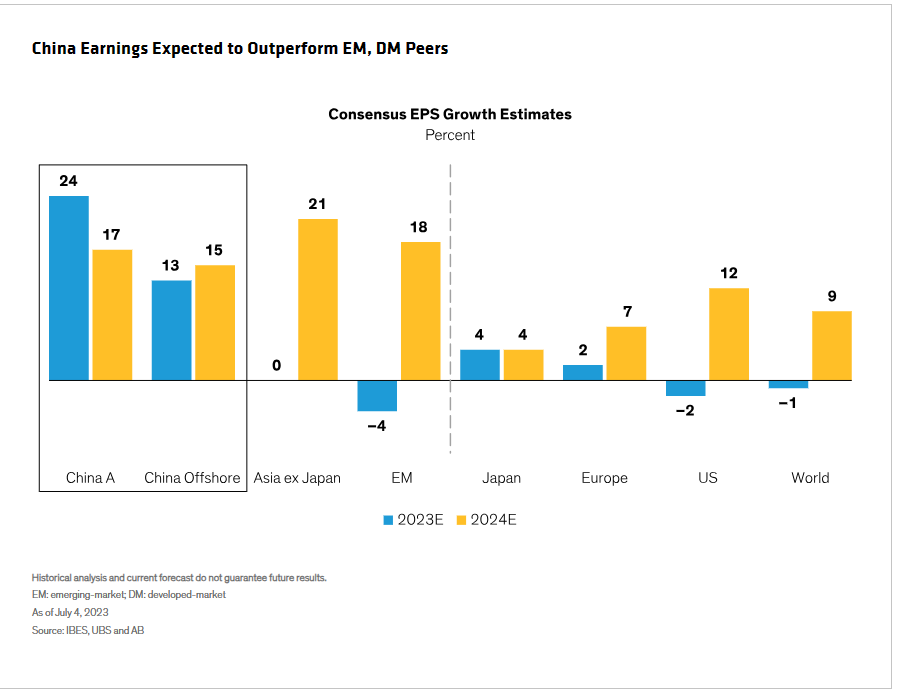

What’s more, the potential for an earnings rebound is high, in our view, though that may not happen until sometime in 2024. Eventually, though, we expect Chinese earnings to outpace those in stocks from major developed and emerging markets (Display).

And any future US dollar weakness could attract additional inflows into the country, potentially benefitting equities and the renminbi.

In this new era of reduced growth, we expect value investing to trump growth-oriented strategies that traditionally have been more popular among investors in China. Identifying strong companies with robust cash flows at reasonable valuations will be critically important and, we believe, will provide investors access to stocks in China’s large and liquid equities market with the most attractive alpha potential.

The most compelling opportunities, in our view, are likely to be found in companies aligned with the government’s commercial and policy objectives, including technology security and domestic decarbonization. We also see opportunities in industrial cyclical companies such as bus makers and forklift manufacturers that have developed compelling products with a strong international footprint. These companies straddle domestic and export markets, offering multiple avenues for success.

Similar opportunities, in our view, exist in other sectors, including home-use medical devices, home appliances and e-commerce. All of these options offer attractive ways to access China’s dynamic equity market, in our view.

China may be relinquishing its role as the primary engine of the global economy—a role it has played effectively for many years. The next stage of China’s evolution will create challenges for investors and, for now, calls for a more value-oriented approach to the equity market. With a strategy that is attuned to the unfolding changes, we believe long-term investors can gain confidence to include Chinese equities as a standalone component within a diversified global equity allocation.