Trending

Written by: Jordan Jackson

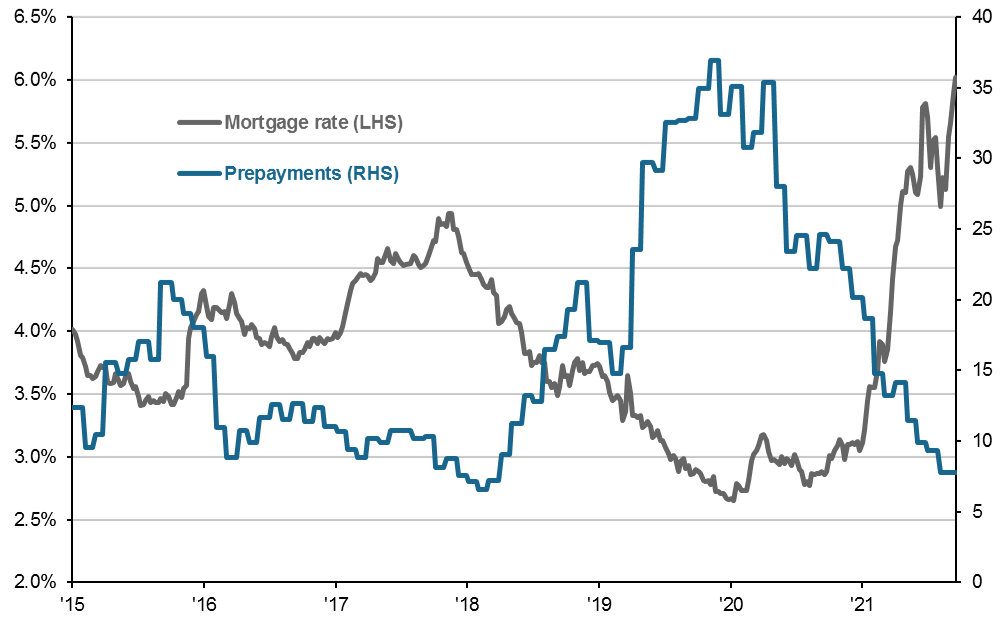

The housing market has had a difficult year. Mortgage rates have skyrocketed from 3.1% to over 6.0% and home prices are up 18% year-over-year. As a result, housing affordability has been crushed leading to a sizeable decline in single-family housing construction and mortgage origination activity. Given the slowdown in the housing sector, investors are curious how this may impact the mortgage-backed securities (MBS) portion of the Federal Reserve’s (Fed) balance sheet under their quantitative tightening (QT) program and the investment implications for mortgage investors?

For the Fed and MBS investors, the move higher in mortgage rates has two important implications:

- It reduces mortgage prepayments. When mortgage rates rise, homeowners are less likely to prepay their mortgage or refinance into a new mortgage (as it would be more costly). Therefore,

- Higher interest rates increase the duration of MBS securities. Because prepayments have slowed, the duration of MBS investment increases as owners continue to make mortgage payments for longer, extending the maturity profile of these securities.

The reduction in mortgage prepayments has consequences for the Fed’s QT program specifically:

- Because prepayments have slowed, the level of mortgages rolling off the balance sheet will fall well below the Fed’s 35 billion USD monthly cap for some time. In fact, we estimate a roughly 20 billion USD pace of MBS paydowns though the middle of next year.

- Compositionally, the Fed’s share of mortgages on its balance sheet may increase even as the overall size of the balance sheet declines due the higher runoff cap of U.S. Treasuries and slower MBS prepayments.

The issue for the Fed is most committee members would prefer a U.S. Treasury-only balance sheet given the Fed now owns ~30% of the MBS market. For this to be achieved, the Fed would need to sell mortgages. If they were to do so, a reasonable assumption could be selling the difference between actual paydowns and the 35 billion USD monthly cap.

For MBS investors, the feedthrough of slowing prepayments increasing mortgage duration poses a challenge. Taking a step back, MBS securities are attractive to institutions and banks given their unique characteristics to traditional bonds. Unlike traditional bonds, when MBS yields rise, duration also increases, this is known as negative convexity. Indeed, the option-adjusted duration for the broad MBS index has risen from 1.1 years in May 2020 to 5.8 years. With yields rising rapidly as Fed tightening expectations are ratcheted higher, the macro environment has made it less attractive for institutions to hold MBS given their preference for shorter-maturity paper.

All things considered, the combination of softer institutional demand and Fed QT paint a challenging backdrop for MBS investors. That said, selectivity is key; higher-coupon mortgages in specified pools where the details of the bonds are known appear most attractive in today’s environment.

The spike in mortgage rates has led to a collapse in prepayments

Average 30-yr. fixed mortgage rate, prepayments (FN30yr monthly CPR)

Source: Fannie Mae, Bloomberg, J.P. Morgan Asset Management. Data are as of September 20, 2022.