Trending

Written by: Marc Odo | Swan Global Investments

Choosing Between Income Today vs. Potential Growth Tomorrow

A fundamental lesson in finance is a security’s price should be the present value of all future cash flows. Cash flows typically consist of a regular string of dividend payments and an assumed liquidation value at the end of the time horizon. These investment gains are classified as “income” and “capital gains,” respectively.

The management of an individual company tries to strike the proper balance. Does the company distribute earnings to shareholders for the immediate gratification of income today? Or does management re-invest earnings in the company, hoping that the growth will compound at a higher rate, and the shareholders will ultimately be better served with the delayed gratification of more capital gains in the future?

This is one of the fundamental questions of corporate finance: do we distribute income today versus seeking higher potential growth tomorrow?

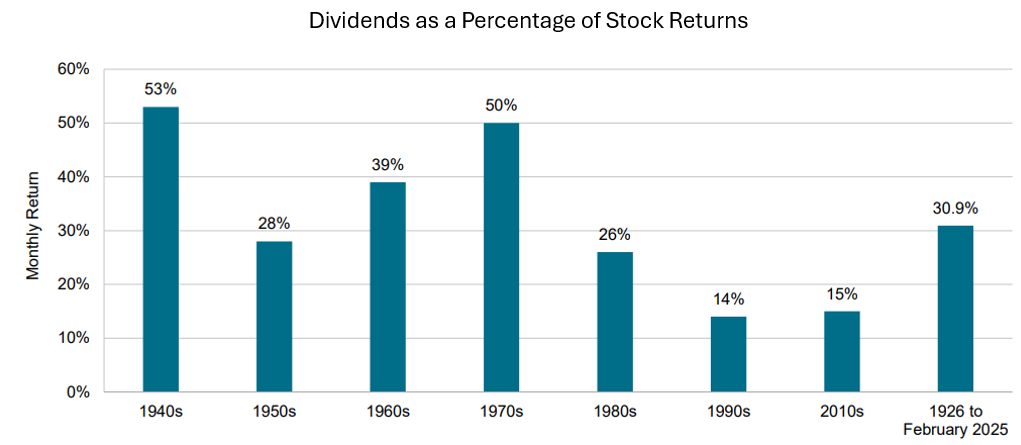

Over the last century roughly a third of the S&P 500’s total return has come from dividends. However, since the 1990’s the balance has shifted to less dividends and more towards re-investment[i].. In recent decades dividends make up around 15% of total returns, half of its historical average. Currently the dividend yield on the S&P 500 is about 1.2%.

[i] The reasons for this shift are far too many to discuss here, but typically include the idea that management seeks to drive the share price up via share repurchases or high-growth opportunities, rather than dividends. In a nutshell, high stock prices are typically good for a company’s management and dividends are taxed at higher rates.

If an individual investor prefers the immediate gratification of “income today” over the delayed gratification of “growth tomorrow”, what options do they have?

- They could invest only in bonds, but then they lose the upside potential of equities.

- They could invest in an ever-shrinking pool of dividend-paying stocks, but these tend to be concentrated in staid, mature industries.

- They could follow a scheduled, liquidation strategy where a portion of the portfolio is sold on a regular basis, but investors are typically reluctant to “dip into capital.”

Covered Call Writing: An Option Strategy for Current Income

There is another option. A covered call strategy allows an individual investor to override a company’s income-vs-growth policy with their own preferences.

With a covered call strategy, the investor owns a stock or a portfolio of stocks. They are fundamentally bullish on the stocks; otherwise they wouldn’t own them in the first place. However, with a covered call strategy the investor prioritizes “cash in hand”, even if it comes at the expense of potential capital gains in the future.

This is accomplished via the writing of call options against the long equity positions. When writing (or selling, or shorting) a call option, the investor agrees to forgo capital gains past a certain price point in the stock. In exchange for surrendering upside opportunity beyond a price, the call writer receives an immediate cash payment, or “premium.”

This is analogous to the fundamental decision that firm’s management makes when they set their company’s dividend policy. Do their shareholders prefer cash-in-hand or long-term growth? An investor considering a covered call strategy must ask himself the same question. Does that investor prefer to write some options and “take some chips off the table” or do they “let it ride” and hope for future gains?

It is important to realize that this represents a trade-off between immediate and delayed gratification. It is tricky to have both.

Typical Investor Misconception: Investors unfamiliar with options often hold a misconception that a covered call strategy on a stock, group of stocks, or equity index simply means they’ll gain some extra income on top of the price growth potential of their holdings, and there is no trade-off.

In an ideal world an investor could write calls all day and retain all the upside potential, but you can’t have your cake and eat it too. Before embarking on a covered call strategy investors should understand the fundamental trade-off between immediate income from covered call writing and potential long-term capital appreciation.

In addition, it should be noted that comparing a covered call strategy to a company’s dividend policy is an analogy, and it isn’t a perfect one. Dividends tend to be much more stable and predictable, whereas the profits and losses on a call writing strategy can be volatile. The analogy is useful in framing the trade-off between a known, immediate profit and uncertain future growth, but premium (or income) from call writing is not the same as dividends.

Since call writing can be volatile, it is Swan Global Investments’ opinion that actively managing a covered call strategy offers advantages over a passively managed approach. If a fund is passively managed a trade is established and then nothing is done until the options expire. This “set it and forget” passive approach will sacrifice capital gains should the written calls go in-the-money.

That scenario creates another dilemma. If the strategy or fund has advertised or seeks to target a specific yield (or amount of income), and the manager cannot generate sufficient gains from options trades, dividends, nor capital appreciation of the stock or index, then the manager will need to dip into the investment capital of the fund (investor’s money) and issue a return of capital to meet that target yield. In other words, return a portion of the investor’s original investment, less a management fee.

Alternatively, an active portfolio manager seeks to manage those risks. An active covered call strategy gives the portfolio manager the freedom and flexibility to change the terms of the trades in an attempt to strike the right balance between immediate income and future gains.

Summary

Covered call writing is one strategy an investor can employ to augment their immediate income needs. However, another fundamental finance lesson should be remembered – there is no free lunch.

Related: They Say My Expectations Are Too High—Here’s Why I’m Keeping Them That Way