Trending

Written by: Gabriela Santos

After an equity market correction of 63% from February 2021 to October 2022, Chinese equities are up 53% since their October lows and the Chinese Yuan is stronger by 7%. Chinese policymakers' more pragmatic economic policy turn at the end of 2022 has contributed to a turn in sentiment, flows and performance. Several pro-growth changes occurred late last year that investors should not ignore: support to the real estate sector, conclusion of the regulatory review of the internet sector, dialing down of geopolitical tensions – and crucially, a changing of the “Zero COVID policy". This year, China is unavoidable for investors. 5 key things to know about China this year:

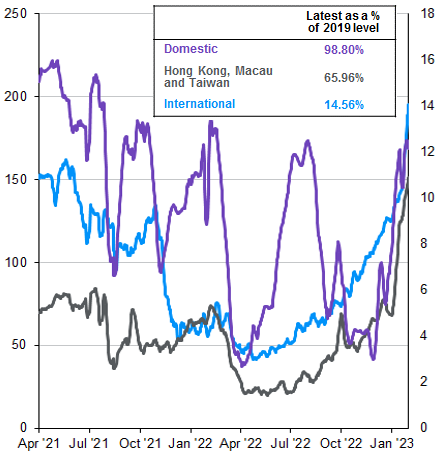

- COVID reopening boom is already here and it’s fast, pulling forward China’s consumption rebound from late this year to starting now. Looking at high frequency data, the peak of the COVID infection wave seems to have occurred at the end of last year. Mobility indicators have bounced back quickly, with subway flow and traffic congestion in major cities back to 80% and 97% of 2019 levels, respectively. Air travel has also rebounded with domestic flights back to 99% of 2019 levels. International flights should continue to pick-up as more flights are added, now at 15% of 2019 levels.

- Three years of pent-up demand of 15% of the world’s population - and the world’s second largest consumer - can’t be ignored. Chinese households have pent-up demand, especially for services, and have excess savings to spend. This rebound of the world’s second largest consumer should support global growth through higher goods and commodity imports and the return of Chinese tourists. This can be a powerful support to other EMs and Europe as China goes from headwind to tailwind.

- China’s policy pendulum has swung fully to pro-growth side: The change in policy has not only involved the pandemic. Policy has also turned more pragmatic involving previous areas of concern for investors, with the focus now on supporting real estate, reassuring private business, and trying to lower the volume on geopolitical noise. As a result, property stocks and bonds, as well as internet application companies have rebounded strongly.

- Initial market bounce was powerful and valuations back to average: U.S. listed Chinese companies (ADRs) are up the most (75%), Hong Kong-listed companies (+44%), and A-shares (+35%), bringing valuations back to long-term averages. However, low global investor positioning suggests more upside, as foreign investors feel more confident to return to Chinese market. The key now is to invest thoughtfully, based on “waves of reopening” (services then discretionary goods) and “beyond reopening” themes (green economy and advanced manufacturing sectors).

- Still the same China beyond 2023: Chinese policymakers will continue to explore the opportunities to direct private capital to different areas of the economy depending on China’s phase of development. These periods of policy reforms have and will likely continue to lead to periods of volatility from time to time. However, in the long-term, we believe the rewards of investing in China outweigh the risks due to low correlation to global markets and higher return potential. The key is to focus on portfolio sizing and active management.

China's high frequency mobility data is improving rapidly

Daily flights dispatched, 7-day moving average

Source: Wind, Civil Aviation Administration of China, J.P. Morgan Asset Management. Guide to China. Data are as of February 8, 2023.

Related: Will Disinflation Be Transitory?