Trending

Could 2H 2025 EPS expectations be at an inflection point?

Market Recap

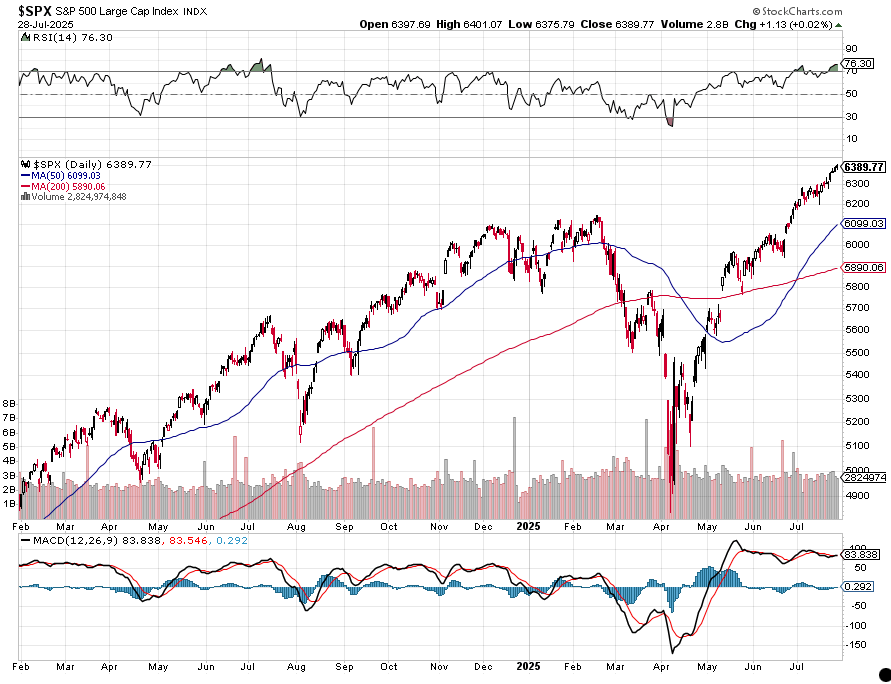

As we discussed in our latest Week Ahead video Sunday night, markets took in last week and Sunday’s tariff news and decided it was enough to push the S&P 500 (0.02%) and Nasdaq Composite ( 0.33%) to new all-time highs. For reference, the S&P 500 has hit new all-time highs in 13 of the past 21 trading sessions. Four of seven Mag 7 names helped the S&P 500 into positive territory, although it most likely was Monday’s midday Samsung (SSNLF) / Tesla (TSLA) chip supplier announcement that made the difference there. With the Dow falling 0.14% and the Russell 2000 declining 0.19% along with eight of eleven sectors ending the day lower, there are signals that while there is optimism about big tech earnings this week, tariff announcements aren’t necessarily the panacea for everyone’s ills.

The Cboe Market Volatility index (VIX) ticked higher to 15.03 and gold softened slightly to $3,310.10/oz, indicating that while there still are some concerns, they’re not enough to send anyone into a tailspin.

The Tematica Select Model Suite saw mixed results with leadership coming from CHIPs Act (CHIPS), followed by EPS Diplomats (DIPLOMTS), Cash-Strapped Consumer (PINCH), and Digital Lifestyle (DLIFE). Laggards included Guilty Pleasure (GUILT), Rebuilding America (REBUILD), and EV Transition (EVTRANS), as that strategy was dragged lower by ChargePoint (CHPT) falling over 18% during its first day of trading following its 20:1 reverse split.

An Overbought Market Faces Big Tech Earnings and Powell

After eking out another record closing for the S&P 500, equity futures point to the recent momentum continuing when US equity markets open later this morning. That “good news” means the relative strength index (RSI) for the S&P 500 would inch ever higher, pushing further past the 70 level that denotes that market barometer being overbought.

And if you’re thinking the setup for the Nasdaq Composite is any different ahead of quarterly results from Microsoft (MSFT), Meta (META), Amazon (AMZN), and Apple (AAPL) this week… let’s just say that isn’t the case.

We’ve wagged our chins quite a bit over the last few months about declining EPS growth expectations in 2H 2025 compared to 1H 2025. That move lower continued last week with the consensus EPS growth for the S&P 500 falling to 7.9% in 2H 2025 compared to 1H 2025 vs. 13.9% at the end of March. With the Trump administration announcing trade deals and the Flash July PMI report depicting a US economy growing above trend, the market will be keenly interested in the guidance issued from those four companies later this week.

Why? For a few reasons, but the one we’re referring to is that those four companies constitute 20% of the S&P 500’s weighting. And if we go one step further and collect the aggregate capital spending guidance from Meta, Microsoft, and Amazon, and factor in Alphabet’s (GOOGL) spending increase, we can add Nvidia (NVDA) to the lot, which alone accounts for another 7.6% of the S&P 500. With more than 25% of the S&P 500 in the guidance crosshairs this week, we could see an inflection point higher for 2H 2025 EPS expectations.

That would be a positive for multiple Tematica models, including Artificial Intelligence (AI), Cloud Computing (CLOUD), and Digital Infrastructure (DIGI), as well as Nuclear Energy & Uranium (NUKE). If that is the scenario that plays out, it would also help remove some of the growing concern over the market’s valuation that has developed as those new closing records have been while EPS expectations have been creeping lower.

While we keep an eye on that, the other item we’ll be watching this week won't be the Fed’s policy decision on Wednesday, but rather what Fed Chair Powell says during the post-policy presser and how he says it. No one expects the Fed to deliver a rate cut tomorrow, but the market is once again in hopium mode when it comes to a September rate cut. As of this morning, the CME FedWatch Tool shows a 62.9% probability for such a cut. However, when we look at that Flash July PMI report, we see the following:

Price pressures intensified across both manufacturing and service sectors during July, widely blamed on higher goods prices due to tariffs, but also in some cases due to rising labor costs. Average prices charged for goods and services rose at a rate just shy of May’s recent high to register the second-strongest monthly increase since September 2022…

Close to two-thirds of all manufacturers reporting higher input costs attributed these to tariffs, whilst just under half of respondents explicitly linked their increased selling prices to tariffs. However, the tariff impact was by no means limited to factories, as around 40% of service providers reporting higher selling prices explicitly mentioned tariffs.

That linkage between tariffs and inflation pressures is what the Fed has been looking to assess, and those findings suggest we are likely to see another step higher in July inflation data and potentially August. And that’s where things could get troublesome for the market - while the market is digesting trade deal headlines, should the inflation data continue to ticker higher or even remain at elevated levels, the likelihood of the Fed delivering a September rate cut is questionable. That’s why we’ll be keenly focused on what Powell says tomorrow afternoon and the language he uses.

To prepare for that, we’ll note that the Volatility Index (VIX) is below 15, which in layman's terms means the market is flashing a signal of complacency. While not indicating Extreme Greed is in the market, the Fear & Greed Index is firmly in Greed mode. And trading volumes are a tad lighter than usual. Those tea leaves, along with the market being overbought, suggest that if Powell’s message is less dovish than the market anticipates, we could see the upward trend challenged.

Not a bad thing if you’re an investor looking for opportunities to put fresh capital to work, but if those Big Tech companies fail to wow the market with their 2H 2025 guidance, we could be in for something more.

Related: Market Volatility Ahead: What Investors Need To Watch This Week