Trending

Written by: Lei Qiu and Wentai Xiao

Artificial intelligence (AI) is creating lots of buzz, and for good reason. New forms of machine learning have the potential to ramp up productivity, and the many potential applications of AI are just now being discovered. But has market enthusiasm for the technology gone too far?

Massive spending on supercharged computing is raising concerns about a return to the dot-com bubble of the late 1990s and early 2000s, when inflated technology share prices eventually imploded. While we understand the comparisons, we believe they’re largely unfounded.

To understand why, we need to travel back in time and understand what drove the dot-com bubble.

The Dot-Com Bubble: A Lesson in Unsustainable Business Models

At the dawn of the internet era, telecom and cable providers poured billions of dollars into web infrastructure, while easy financing and investor exuberance drove tech-stock prices to new heights. But the business models needed to leverage this infrastructure weren’t fully developed, and tech-stock valuations got ahead of company fundamentals. Eventually, a long line of start-ups became overvalued, capital dried up and the bubble burst.

Some might argue that today’s build-out of AI servers harkens back to the dot-com heyday, which didn’t end well for investors. After all, by the end of 2024, more than $100 billion will have been invested in AI infrastructure by enterprises, cloud companies and governments.

But that’s where the similarities end.

AI Infrastructure Is Being Financed by Revenues—Not Speculation

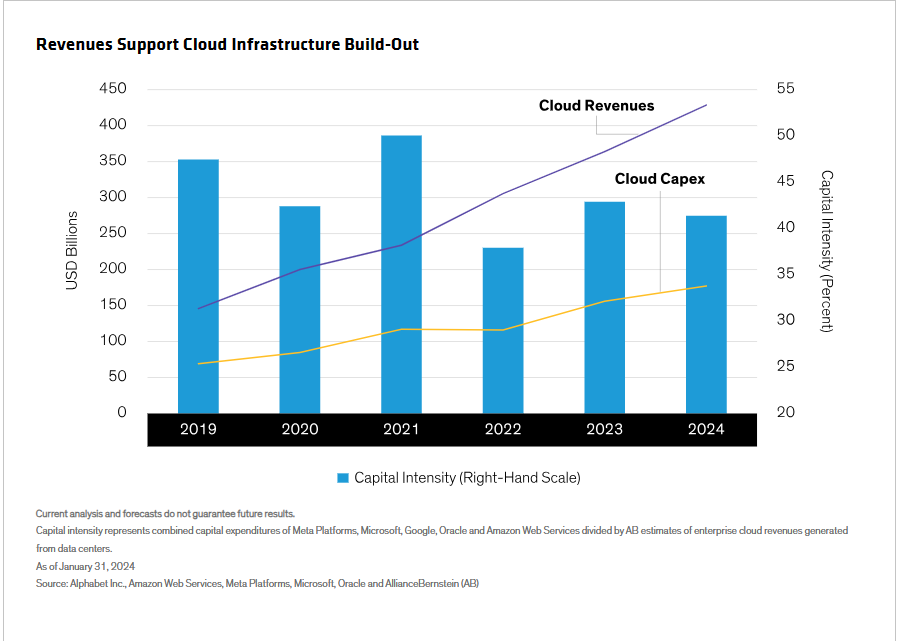

Unlike many companies in the dot-com era, the mega-caps behind the current build-out of cloud infrastructure are already profitable. Substantial revenues are being generated on cloud infrastructure, from cloud application and infrastructure software to social media advertising. This is reflected in cloud capital intensity (capital expenditures as a percentage of total revenues), which has held steady because the infrastructure being built is already supported by demand (Display).

Rather than anticipating the next big product—a failed tactic of the dot-com boom—today’s profitable AI stalwarts are spending on cloud infrastructure primarily to improve efficiency. In fact, that’s perhaps the best way to view artificial intelligence—as an efficiency driver.

AI Spending Has More Room to Run

The current spending boom is centered on building the next layer of digital infrastructure—known as “accelerated compute”—where generative AI is just one among many applications. Accelerated compute is a more efficient form of computing infrastructure that supports both AI and non-AI workloads—everything from social media–content recommendations to probabilistic targeting to drug-discovery simulations. Much of this infrastructure is cloud based. The cloud can be thought of as a utility grid for advanced computing functions—akin to the electricity grid that powers the physical world. The resulting efficiency gains—and returns on investment—are driving faster AI adoption rates than many expected.

Accelerated compute represents a new paradigm for making feasible workloads that were previously impractical. ChatGPT estimates that it would have taken more than five years to train a 175-billion-parameter large-language model on general-purpose computing using high- end server CPUs. By contrast, using high-end server GPUs on accelerated compute, it would have taken two to four months. Simulation company ANSYS estimates that running a high-end aerodynamics simulation on accelerated compute could speed up simulation time by as much as 33 times.

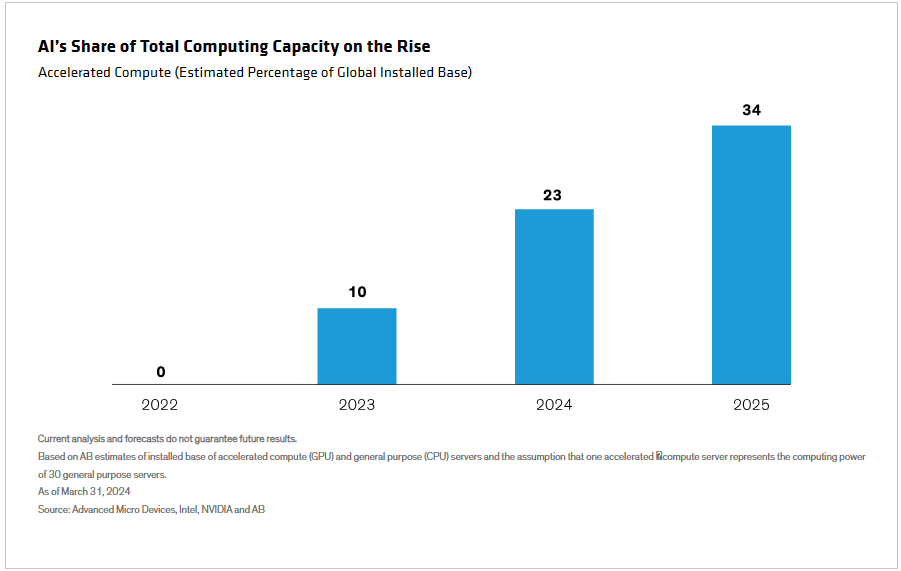

And there’s still plenty of room to run. Currently, between 10 to 15 million CPUs are being shipped annually, compared with fewer than one million accelerated servers. We estimate that less than 25% of global installed computing-power capacity is accelerated (Display), up from close to zero just two years ago.

Are Tech Stocks Overvalued?

The promise of a quantum leap in productivity is real, in our view. Yet, the adoption and application of the technology will play out over years, and it will take time for investors to identify the long-term business beneficiaries of this dramatic technology paradigm shift.

We’ve arrived at an inflection point that began in the early 1990s—a journey that has taken us from narrowband to broadband to mobile and now generative AI. Instead of comparing this stage of the technology evolution to the dot-com bubble, we believe it’s more useful to view it as an extension of Web 3.0—a vastly more efficient, decentralized internet connected by peer-to-peer networks and powered by machine learning.

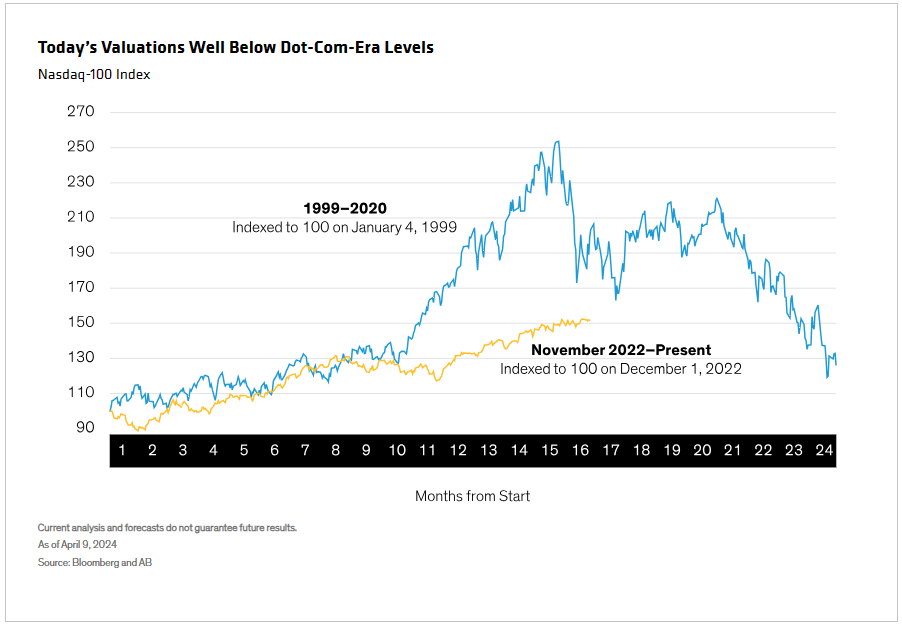

In that context, we believe a good degree of market excess was already wrung out in 2022, when technology stocks fell sharply in a down market. While tech stocks have partially recovered from that shock, we don’t believe they’re as overvalued as some investors believe—and they’re certainly not at the levels seen during the dot-com era (Display).

Seismic technology cycles have inevitable ups and downs. But regardless of market conditions, equity investors can benefit from the return opportunities afforded by innovative disrupters. In the past, successful enablers of transformational innovation have enjoyed surprisingly large and lasting growth trajectories. So, we think companies that build differentiated competitive moats driven by AI have the potential to deliver long-term earnings growth for investors.

Today, we’re in the very early stage of a transformational digital infrastructure upgrade and product cycle. Industry trends suggest that this is not another technology bubble. With a patient and disciplined approach, we believe equity investors can identify companies with sustainable AI business models built on real profits, rather than false promise.