Trending

Written by: Mike Rode, CFA | American Century

Another wild year for markets, another subpar showing for U.S. small-cap stocks compared to large-caps.

Despite entering 2023 with inexpensive valuations, small-caps faced several performance headwinds, such as continued interest rate hikes, a mini regional banking crisis, a perpetually looming recession and endless flows into the Magnificent 7 (Apple, Alphabet, Microsoft, Amazon, Meta, Nvidia and Tesla).

In this environment, it’s easy to forget that small-caps have historically outperformed mid-cap and large-cap stocks since 1925, according to Furey Research.

As we step into 2024, we believe U.S. small-caps look compelling.

-

Underowned: Small-caps now represent just 4% of the broader U.S. stock market versus the long-term average of nearly 8%. This low percentage has occurred only twice before, in March 2020 and back in the 1930s.

-

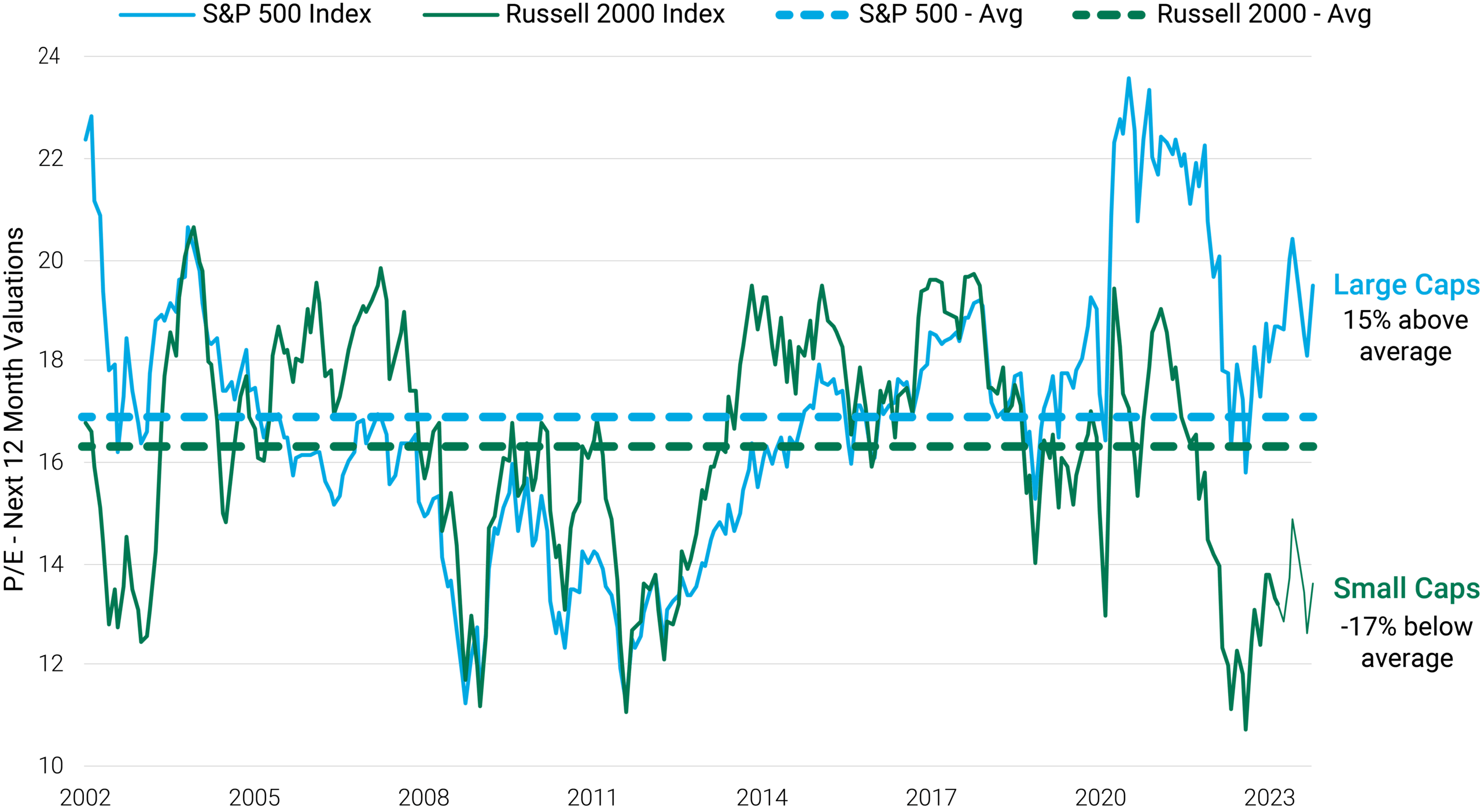

Valuations: Small-caps are trading nearly 20% below average compared to large-caps trading at 10%-20% above average. The spread between small and large has rarely been this wide and has historically been followed by a sharp reversal.

-

Reshoring: Small-cap company fundamentals may be poised to benefit from the ongoing trend of bringing manufacturing operations back to the U.S. This shift is driven by geopolitical risks, dwindling cost advantages and fiscal stimulus programs like the U.S. CHIPS Act and Inflation Reduction Act.

Here are five common questions we get about small-cap investments.

1. How can small-cap stocks outperform in a recessionary environment if one materializes in 2024?

It’s true that small-cap companies have historically underperformed in the first half of a recession because they are generally more economically sensitive businesses. On average, small-caps have declined approximately 14% in the first half of a recession versus a smaller decline of 10% for large caps.1

However, we believe a moderate recession is largely priced in at this point, given the valuation disparity, as shown in Figure 1, and the fact that small-caps are down almost 30% since their November 2021 peak.

Small-caps have historically led all asset classes out of recession, beating large-caps by 4%, on average, in the second half of a recession and 17% one year after a recession ends.2

Figure 1 | Value Disparities Between Large- and Small-Cap Stocks

Data from 2/28/2002 – 11/30/2023. Source: FactSet. Past performance is no guarantee of future results. Price to Earnings Ratio (P/E) is defined here.

2. Over one-quarter of small-cap companies are losing money today. Is this a risk to small-cap stocks?

Let’s look closer at the 27% of small-cap stocks that aren’t making a profit.

Over one-third of these unprofitable companies belong to the biotech and pharmaceutical industries. That’s why we believe investors should use active management to help choose potential winners (often acquired by Big Pharma) and help avoid potential losers.

Most companies prioritize developing new drugs in these sectors rather than making money, which explains their lack of revenue and earnings. Over time, returns from this group have been solid, though highly volatile.

The remaining two-thirds of unprofitable companies come from various industries, and many of these companies might be at risk of going bankrupt if there’s a significant economic downturn (hard landing) or interest rates stay consistently high.

Historically, profitable small-caps have outperformed unprofitable companies. (Source: FactSet.) Active managers can help navigate recession and high interest rates by avoiding lower-quality companies with heavy debt loads and minimal or no profits.

3. Companies choosing to stay private longer has resulted in fewer publicly traded investment options for small-cap managers. Is this a drawback for small-cap stocks?

Companies have been staying private for longer. In 1980, the median age of a company before its initial public offering (IPO) was six years versus 11 years in 2021.3

Still, the small-cap pond is deep, with over 1,500 publicly traded companies with $1 billion to $8 billion in market capitalization for small-cap managers to choose from. Indeed, the top five companies in the Russell 2000® Index represent less than 2% of the index. Compare that to the highly concentrated world of large-caps, where the top five holdings represent nearly 22% of the S&P 500® Index.

In addition, the IPO market has been robust when market conditions are favorable. For example, 2021 set a record with 1,035 IPOs. We expect a resurgence of IPOs when markets cooperate led by later-stage, higher-quality companies first to market.

4. Regional banks occupy a big space in the small-cap universe, particularly on the value side, with a nearly 16% weight in the Russell 2000® Value Index. Do regional banks pose a risk for small-caps, and how is the American Century Small Cap Value team positioned?

Small-cap banks struggled in 2023 with the failures of Silicon Valley Bank, Signature Bank and others early in the year, sending the group down 40% at one point as measured by the KBW Regional Bank Index (KRX).4

Though most banks addressed liquidity concerns, the industry fell more than 20% by the end of the third quarter in 2023. Lower profit margins helped drive the decline. Margins are under pressure because the difference between a bank’s short-term borrowing cost and the revenue generated by its long-term loan business is narrowing. Exposure to commercial real estate and worries that a recession could lead to delinquencies or defaults also weighed on banks.

These concerns have many investors shying away from banks, evidenced by the average small-cap value manager being significantly underweight small-cap banks compared to the benchmark, according to FactSet. On average, asset managers focusing on small-cap value stocks now hold smaller positions in banks than the benchmark, signaling a lack of confidence.

The American Century Small Cap Value team has a contrarian viewpoint. We see an opportunity with small-cap banks because we believe their valuations are attractive, and based on our analysis, we believe the quality of select institutions is better than many perceive. We see this in capital levels that are higher than before the financial crisis of 2007-2008, and in the more disciplined lending standards they’ve adopted over the last decade.

Although current profitability faces challenges, we expect improvement in the second half of 2024.

5. What if inflation picks up again?

Historically, inflation of 2%-4% has been a positive environment for small-cap performance because more cyclical businesses benefit from slightly higher inflation. That’s because higher rates are typically associated with stronger economic growth, which benefits small-caps, given their higher exposure to cyclical businesses.

A resurgence in inflation from these levels and a resumption of Federal Reserve interest rate hikes would challenge small-cap performance relative to large-cap companies.

But small-cap company valuations remain compelling, reaching levels not witnessed for decades. In our view, this creates a solid foundation for the asset class and an attractive entry point for patient, long-term investors.

In 2023 the markets had some unexpected twists, especially for smaller companies. Despite challenges, we think there are solid reasons to consider investing in small-cap stocks in 2024.

They have attractive valuations* and may be poised to benefit from global trends like deglobalization and the reshoring of manufacturing back to the U.S.

Related: 3 Timely Sources of Yield Potential to Enhance Returns