Trending

“The most inappropriate monetary policy that I’ve seen maybe in my lifetime.”- Paul Tudor Jones on the Federal Reserve via CNBC

The Federal Reserve has three mandates per their Congressional charter. They are to effectively promote maximum employment, stable prices, and moderate long-term interest rates. The Fed has met the first goal, employment is largely maximized. As far as the other two, the Fed is running monetary policy consistent with destabilizing prices and doing it with interest rates that are well below moderate.

Why are they employing the “most inappropriate monetary policy” that famed investor Paul Tudor Jones has seen in his lifetime? Maybe the better question is, is such an aggressive policy, which purposely goes against their mandate, hiding something?

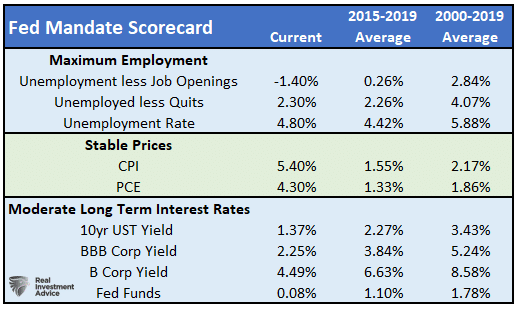

Fed Mandate Scorecard

To provide context to the questions, let’s review the three Fed mandates and compare their current standing to the past.

Maximum Employment

The unemployment rate is slightly above the average of the five years leading to the pandemic but over 1% below the longer-term average. The two alternative employment measures, which factor in job openings and those willingly quitting jobs, show the adjusted unemployment rate is well below the 20-year average.

Traditional measures of employment are essentially fully recovered from the pandemic. Alternative measures, such as those above, tell us the labor market is healthier than almost any time in the last 20 years.

Stable Prices

Inflation measured by CPI and the Fed’s preferred method, PCE, runs two to three times the rate of the last five and twenty years. Five-year market-implied inflation expectations are up to 2.90%, about twice that of the previous ten years. Consumer inflation expectations, measured by the University of Michigan, are nearing 5%, also twice that of the last ten years.

Prices are far from stable. All measures of inflation are running hot and showing signs they may be more persistent than the Fed’s verbiage “transitory” would have us believe. Even Jerome Powell is finally admitting as such. Per a recent speech, he had this to say in regards to inflationary pressures: “have been larger and longer-lasting than anticipated,”

Moderate Long Term Interest Rates

Interest rates for just about everything is well below average. The Fed still has the Fed Funds rate pinned near zero with no intentions of raising it anytime soon. Corporate yields and mortgage rates are also at or near record lows.

With the Fed seemingly ignoring its three congressional mandates, we look at the amount of monetary stimulus the Fed is applying to the system.

Measuring the Extremeness of Monetary Stimulus

The Fed conducts monetary policy via manipulating the Fed Funds rate. In 2008, when the rate hit zero, the Fed wanted to do more. Unwilling to lower rates below zero, they introduced quantitative easing or QE. QE effectively lowers rates by buying Treasury and mortgage securities. The reduction of supply leads to higher prices and, therefore, lower interest rates and yields.

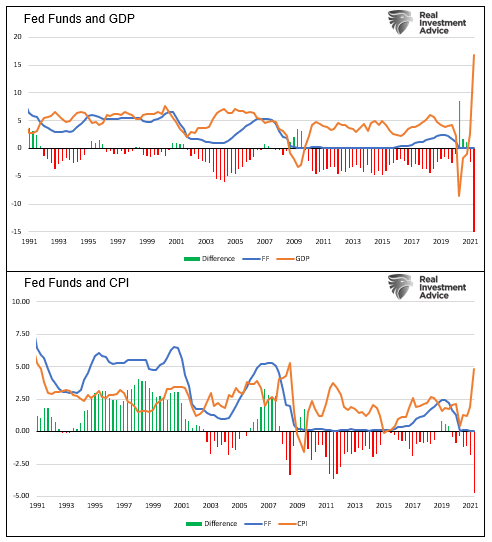

Fed Funds

Before 2008 we could measure how aggressive monetary policy was by comparing Fed Funds to measures of economic growth. The graphs below, for instance, compare nominal GDP growth and CPI with Fed Funds.

In the top graph, the Fed has kept Fed Funds well below the economic growth rate over virtually the entire period since the Financial Crisis. The second graph shows they have held the real Fed Funds rate (inflation-adjusted) negative since 2008.

As shown, the Fed is increasingly using more stimulative rates of Fed Funds. This latest dose of stimulus is even more excessive than prior ones when compared to economic conditions.

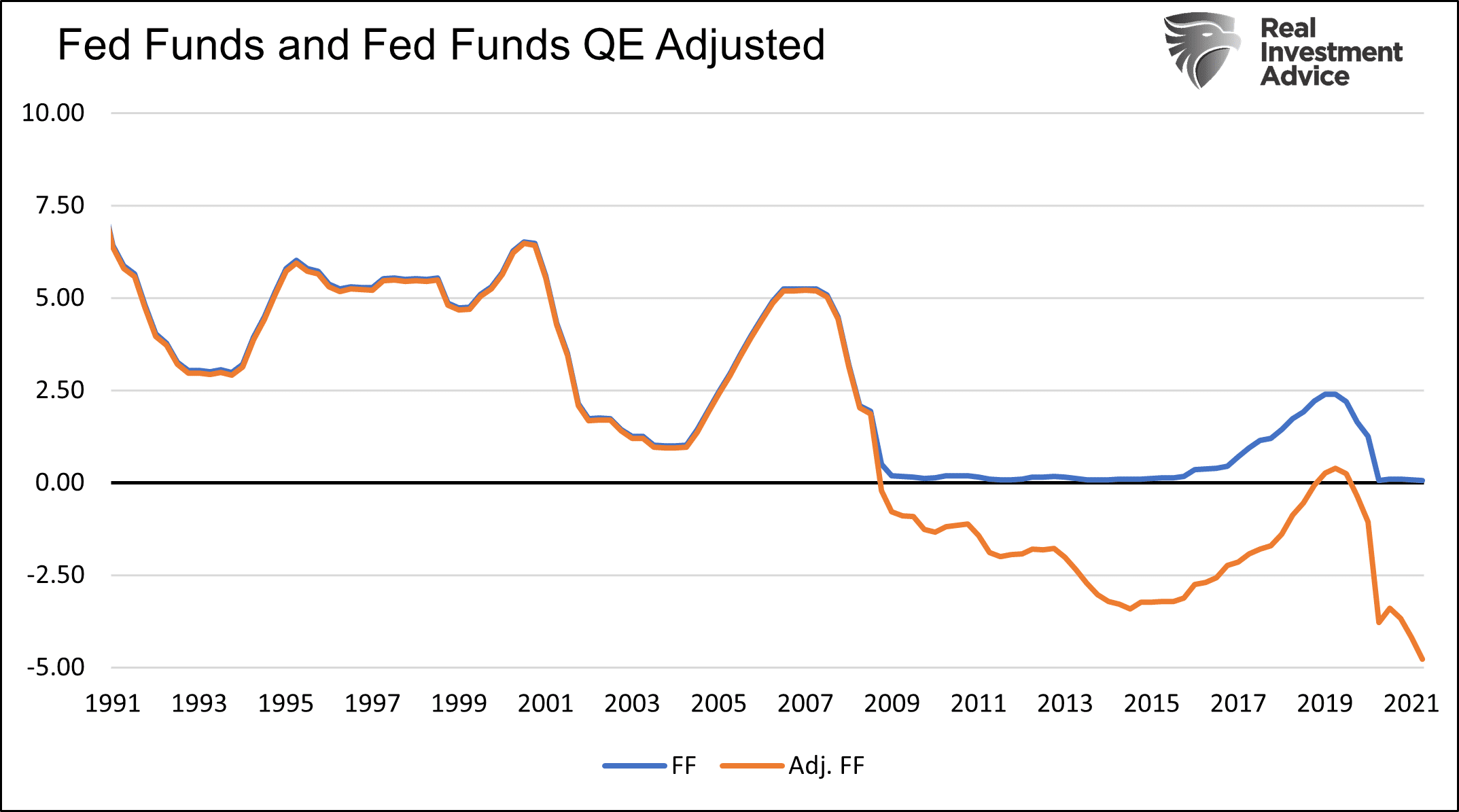

QE

Since the birth of QE, the graphs above do not paint a complete picture of monetary policy. To do that, we must factor in QE and the effect it has on interest rates.

Ex Fed Chairman, Ben Bernanke, estimates every additional $6-10bn of excess reserves held by banks (a byproduct of QE) is roughly equivalent to lowering interest rates one basis point.

The “Bernanke adjustment” to Fed Funds results in the effective level of Fed Funds being 5% below the current level. To repeat, Fed Funds are effectively at -5%.

Looking back at the last ten years, Fed Funds were effectively 2.00 to 2.50% lower than the stated rate.

We can do a similar analysis using an alternative model which the Fed tracks closely.

Per the University of Chicago Booth Business School: “Chicago Booth’s Jing Cynthia Wu and Fan Dora Xia, now at the Bank of International Settlements, devised an alternate shadow Fed Funds rate that can be negative, reflecting the Fed’s additional easing through unconventional policies.”

Like our adjusted Fed Funds rate above, the Wu Xia Shadow Rate quantifies the effective Fed Funds rate accounting for QE. As we show below, the Wu Xia model estimates that Fed Funds are essentially negative 2.50% today.

Why?

With the data above showing the unprecedented nature of monetary stimulus, we must ask why the Fed continues to drag its feet and maintain extreme crisis level policy. Maybe Congress should ask Powell why is he ignoring their mandate?

We think there are two answers.

Market Fragility Frightens the Fed

First, the financial system is highly fragile. QE helps stabilize falling markets and provides a solid tailwind for asset prices. However, it does little to incentivize borrowing and economic growth.

The S&P 500 is up 34% since the pre-pandemic highs. Over the same period, real GDP has grown less than 1% and S&P 500 earnings by 14%. Further, junk ccc-rated bonds now yield 7.5%, down 4.5% from pre-pandemic levels. There are many more examples of asset prices that have exceeded the fundamentals backing them.

Asset prices and valuations, which were already historically elevated, have become even richer. The markets are banking on the Fed to keep stimulus rolling. The Fed understands its role. They have repeatedly mentioned that they will be very slow to remove stimulus to not upset “financial stability.”

Financial stability is code for asset prices, and the last thing the Fed wants to do is pop a bubble, especially since they blew it up.

Debt Fragility Frightens the Fed

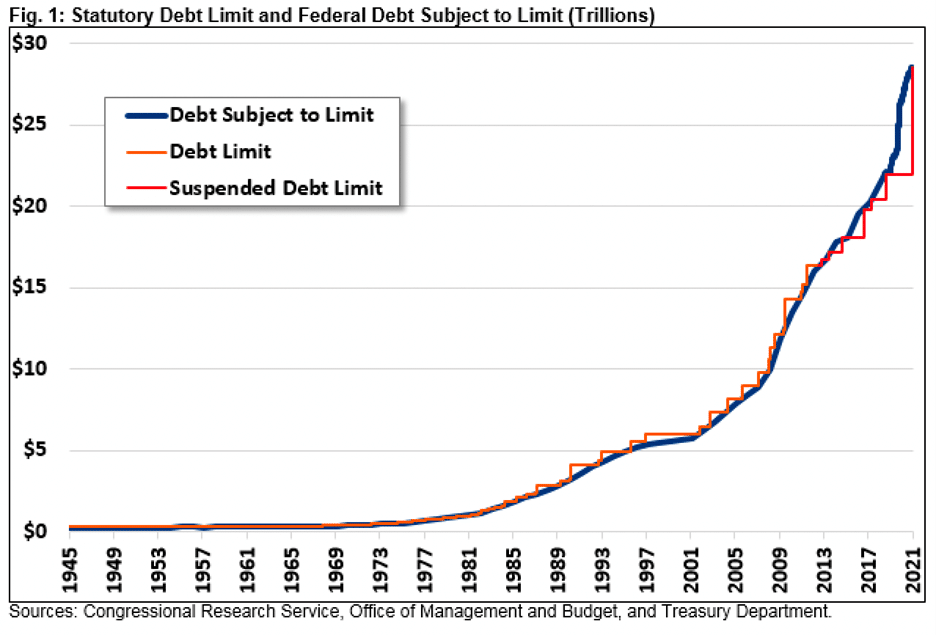

Second, fiscal prudence is a joke, as we were recently reminded when Congress raised the debt ceiling for the 81st time.

Increasing debt is not necessarily bad. However, when it grows much faster than the ability to pay for it, it becomes problematic. The ratio of Federal debt to GDP now stands at 125%, up from 105% before the pandemic and more than double the percentage from before the financial crisis.

The Treasury needs low-interest rates and consistent buyers of their debt to keep such an unsustainable pace going. Through zero interest rates and purchases of $80 billion Treasury notes a month, the Fed fills both needs.

Without extremely low-interest rates to make the new and existing debt affordable, economic growth would disappear, and financial defaults would be plentiful. The Fed must believe they must help Congress worsen the nation’s fiscal imbalances versus dealing with the problem in a sustainable manner. Expediency at tomorrow’s cost, once again, seems to be winning the day.

Summary

The Fed does not want to pierce multiple asset bubbles or force the Treasury to pay normal market interest rates. The financial markets are extremely fragile, and the debt situation is unsustainable. Hiding such actions under the guise of appropriate monetary policy seems to be their modus operandi.

They will continue to use gibberish arguments to avoid addressing the real problems. William White, a distinguished economist with significant central bank experience, writes: “Perhaps the real framework is anything that justifies not tightening?“

Use caution when investing. “The most inappropriate monetary policy” is the sole bedrock supporting the most egregious asset valuations in well over 100 years.

Related: What Causes “Transitory” Inflation to Become “Persistent”?