Trending

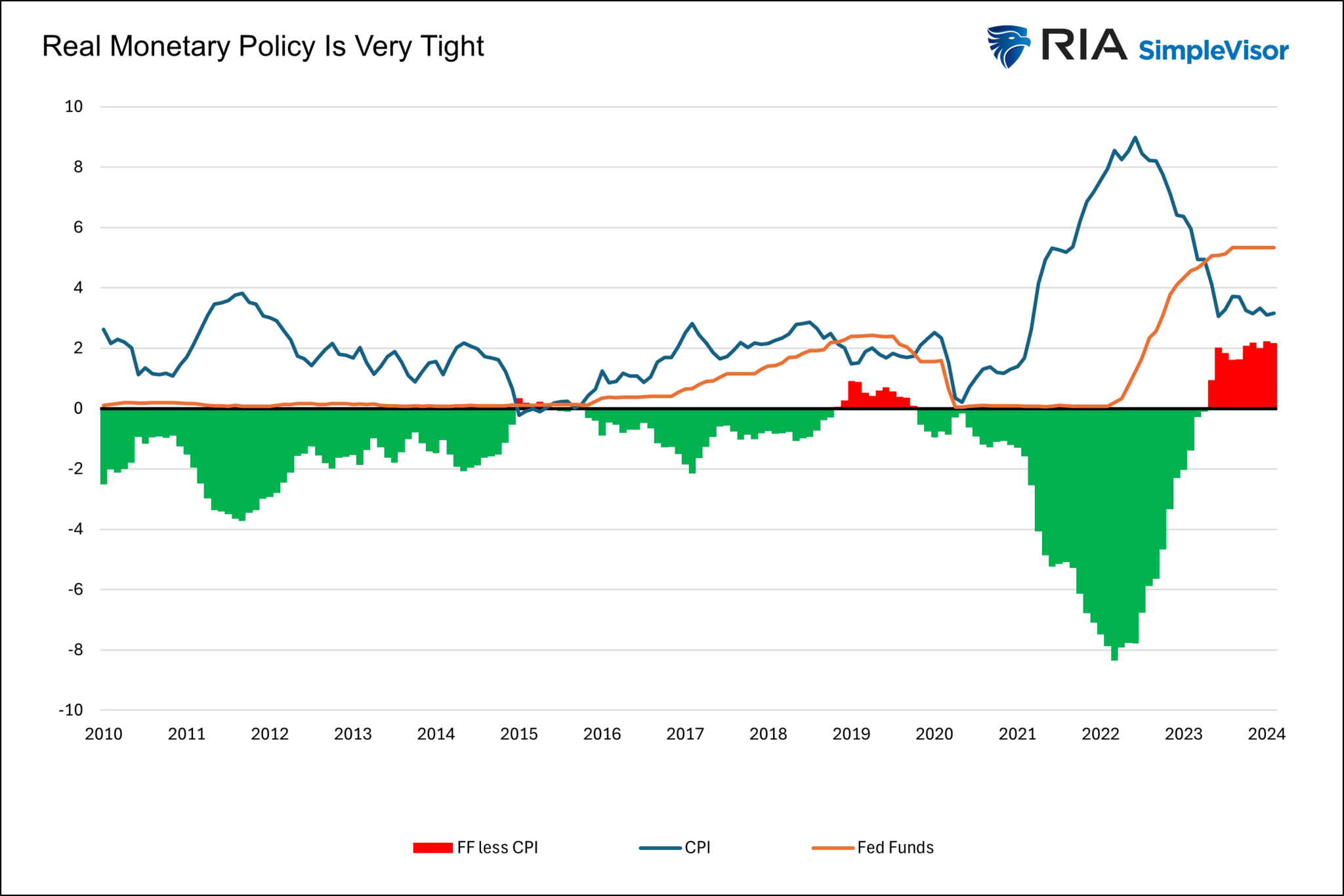

Over the last few months, the downward inflation trend has slowed appreciably. Such leads some to conclude that inflation is sticky and likely to stay around current levels instead of returning to the Fed’s 2% target. As we have noted on numerous occasions, we think inflation will continue to decline over time. The pandemic-related damage to the supply side of the economy is fixed. Further, demand for goods and services is normalizing quickly as pandemic-related savings are largely spent. Additionally, labor markets are no longer tight, meaning upward pressure on wages is diminishing rapidly.

As they always have, monetary policy and economic conditions will determine the longer-term inflation trend. With economic conditions normalizing rapidly, we should shift our attention to monetary policy. On that front, the Fed Funds rate is 2% higher than inflation. The green and red bars show this is the tightest Fed policy in well over 15 years. Even if inflation remains sticky, the Fed Funds can decline by at least 1% and still be tight. However, since 1950, tight monetary policy has, with only one exception (1995), led to a recession. A recession would likely cause inflation to fall to 2% or lower. The Fed would cut rates significantly in that circumstance.

What To Watch

Economy

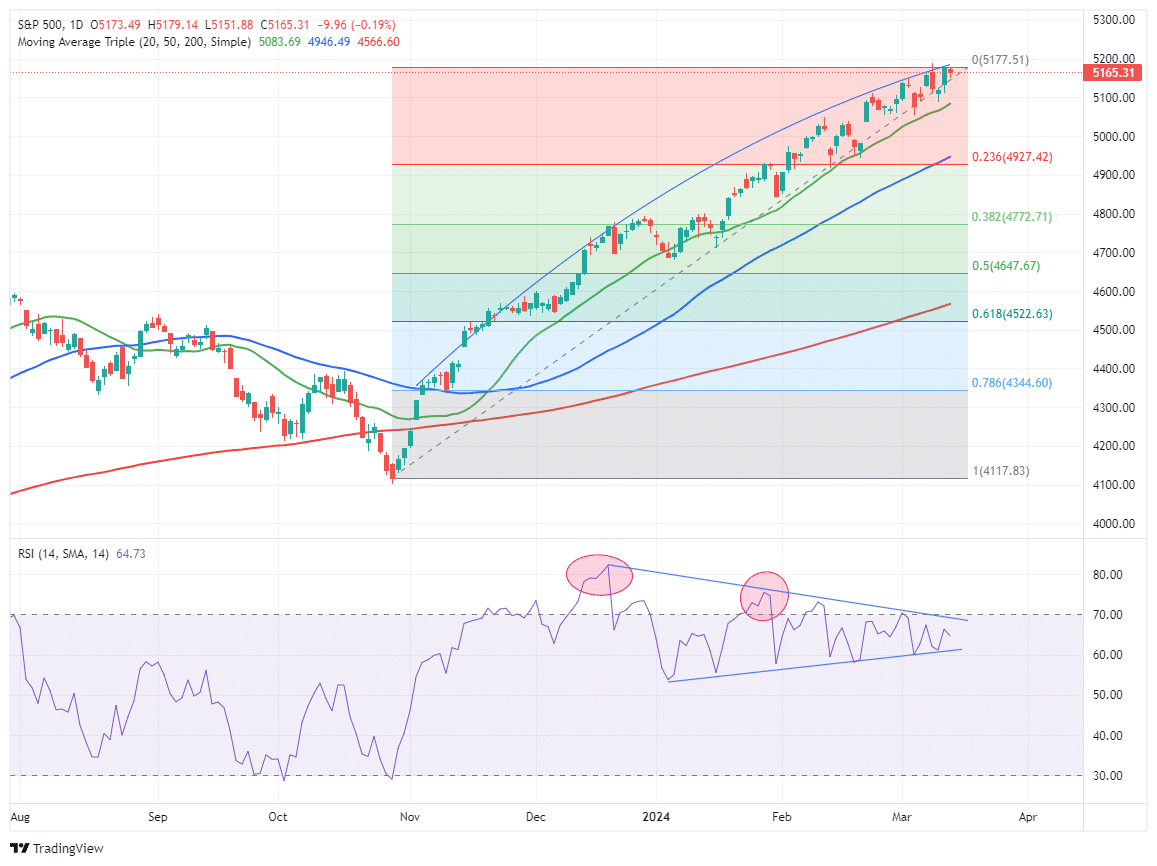

Market Trading Update

As the market continues to trade in the same narrow bullish trend since the beginning of the year, the angle of ascent is beginning to narrow to the 20-DMA, which has acted as consistent support. With relative strength continuing to diverge negatively, the risk of a correction continues to remain. Today, we are updating our Fibonacci retracement levels, which will establish potential levels of support during a corrective phase.

If the 20-DMA support line is broken, the first important support level becomes the 50-DMA at 4927. If that level fails, a bigger correction is in process, and the 38.2% retracement level is the next support, which takes the market back to the beginning of the year. However, there is very little support at that juncture. While the 50% correction retracement level should encompass the bulk of the bullish decline, by the time the market retraces to that level, such should coincide with the 200-DMA. Given the current deviation from the 200-DMA, a correction to that level, which would be around 4600, is entirely possible, as we saw in October last year.

So far, there is no evidence of a larger correction in the works. However, it is worth understanding the potential retracement levels to evaluate the risk in your portfolio. It is also important to realize that at some point, without a doubt, the market will retrace to the 200-DMA. It is only a function of time and the right catalyst. Manage your risk accordingly.

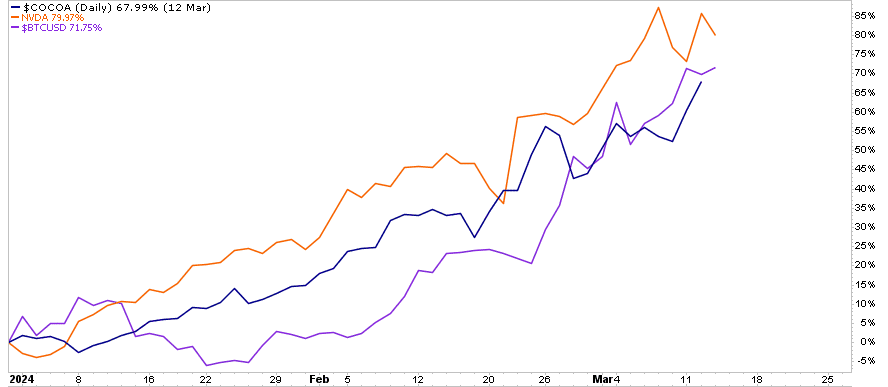

Add Cocoa To The List Of “Mooning” Assets

While everyone is following the prices of Bitcoin, Nvdia, and a handful of other assets whose prices are soaring, few appreciate the recent price action of cocoa. The graph below shows that the year-to-date performance of cocoa is nicely aligned with that of Bitcoin and Nvidia. However, unlike the prices of Bitcoin and Nvidia, cocoa is not necessarily a speculative mania. Per NPR:

Cocoa’s troubles stem from extreme weather in West Africa, where farmers grow the majority of the world’s cacao beans.

“There were massive rains, and then there was a massive dry spell coupled with wind,” says CoBank senior analyst Billy Roberts. “It led to some pretty harsh growing conditions for cocoa,” including pests and disease.

Now, cocoa harvests are coming up short for the third year in a row. Regulators in the top-producing Ivory Coast at one point stopped selling contracts for cocoa exports altogether because of uncertainty over new crops.

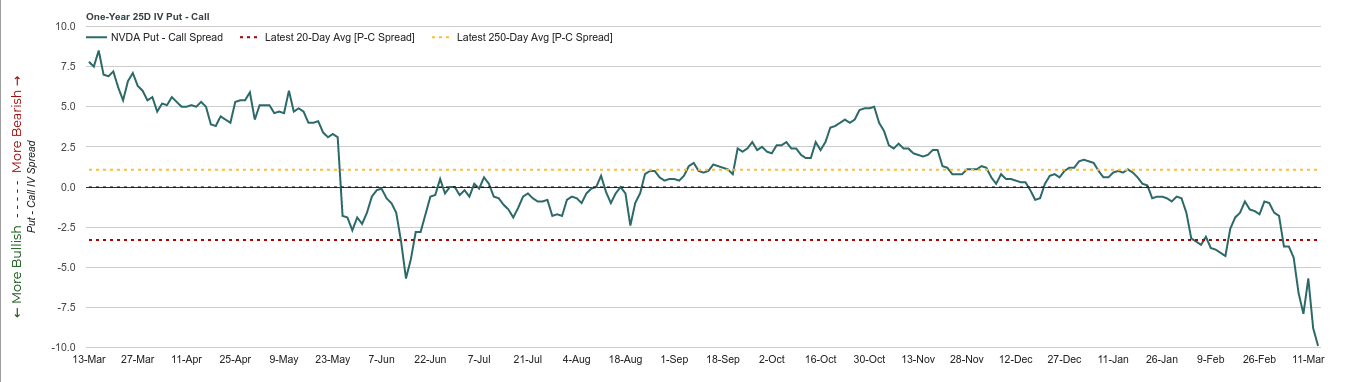

Nvidia Put Call Skew Shows Extreme Sentiment

Option put call skew measures the pricing of puts versus calls. It uses out-of-the-money puts and calls with strike prices of equal distance to the current price. If the skew is negative, it means investors are paying more for calls than puts. Under normal circumstances, the put call skew is positive.

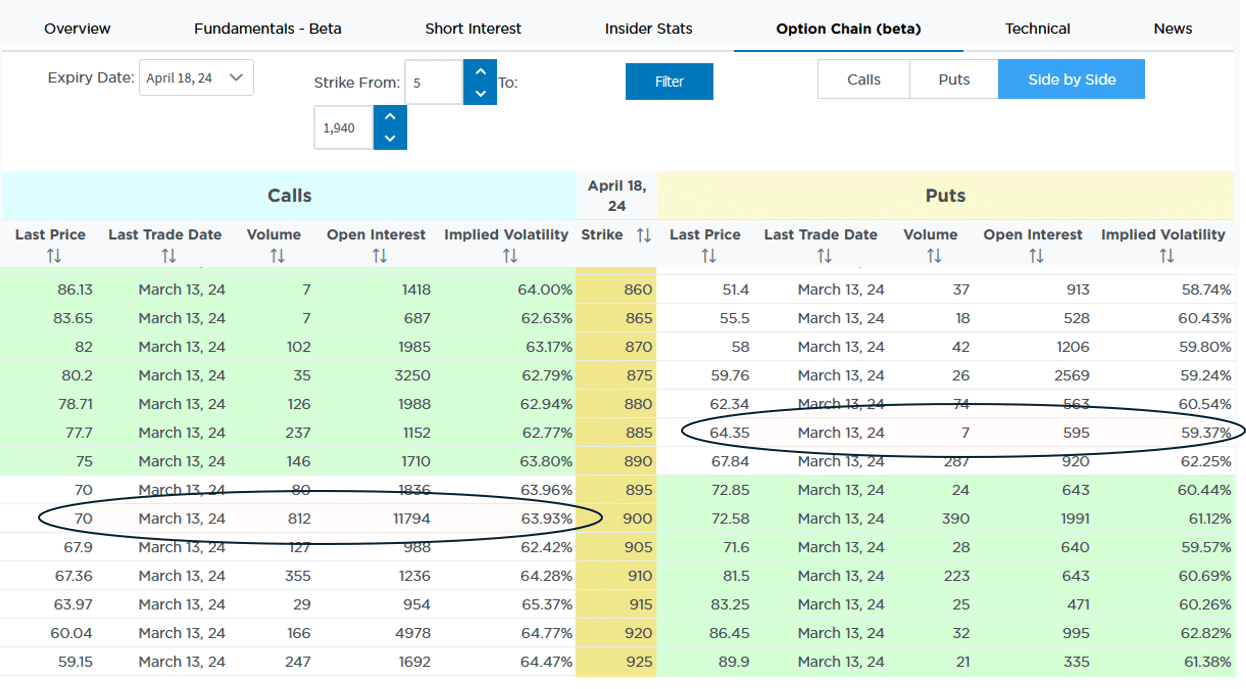

As we share below, the put call skew on NVDA is exceptionally negative, meaning investors are heavily buying calls and shunning puts. More simply, investors are incredibly bullish. The second graphic below, courtesy of SimpleVisor, shows Nvidia put and call option pricing for April expirations. When we clipped the screen, the circled puts were 7 points out of the money, and the circled calls were 8 points out of the money. As it shows, the calls trade for $70 while the puts are $64.35. Furthermore, the open interest in the calls dwarfs that of the puts. In more simple terms, sentiment in Nvidia is off the charts!

Tweet of the Day

“Want to have better long-term success in managing your portfolio? Here are our 15-trading rules for managing market risks.”

Related: Employment Reports: Navigating Household vs. Headline Discrepancies