Trending

Tenured investors understand they’re deploying capital during two of the greatest unknowns in recent history. It’s important for all investors to maintain perspective and use the following three ways to navigate 2023’s greatest unknowns.

After over a decade of decadent Fed policy, investors are asking themselves the following questions:

- Will the stock market’s bullish trend continue, or is a reversion of long-term averages imminent now that the Fed is increasing interest rates at the fastest pace in four decades?

- How do investors and portfolios navigate one of the most globally synchronized quantitative tightening cycles in the last twelve years?

Unfortunately, I do not have the answers. Only time will tell. However, I will provide three ways to navigate 2023’s greatest unknowns. Perspective, rules, and unemotional considerations are most important.

To stay grounded, I never forget the seminal advice from legendary market pundit Martin Zweig:

Don’t Fight the Fed.

Well, here’s the gist of what he wrote, a bit more eloquent: The market’s major direction is dominated by monetary considerations, primarily Federal Reserve policy and the movement of interest rates.

He penned those words in his 1970’s book Winning on Wall Street, and they’ve stood the test of time. And while I certainly can fool myself into thinking otherwise (investors do that a lot), it’s important for me to prick my own emotional balloon by remembering his sage advice often.

As a matter of fact, I created an adage of my own: The Fed is my greatest ally or vilest foe.

By the way, the revised version of Winning on Wall Street is well worth a read for every investor, especially those just starting out.

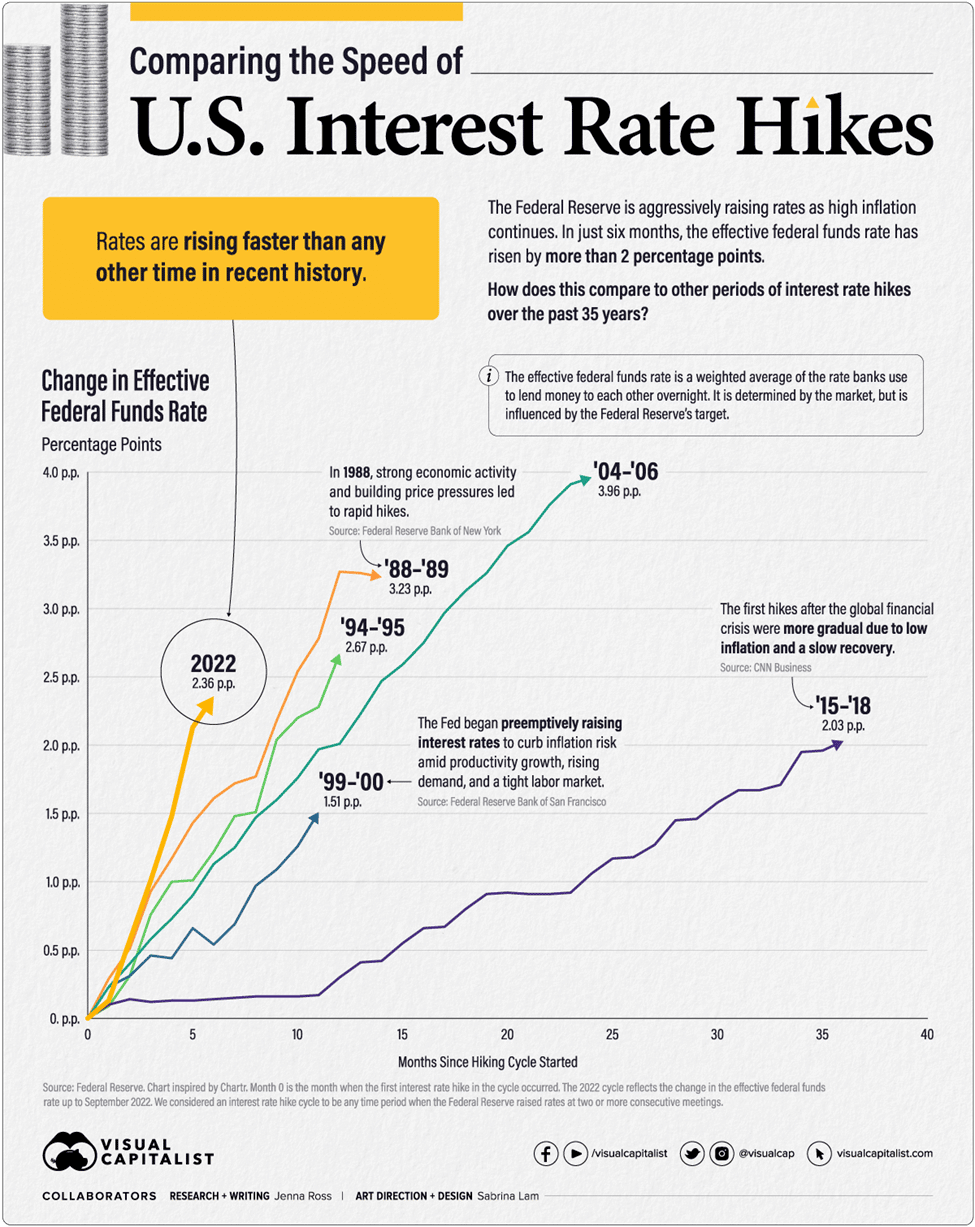

As we know, the Fed has been a market nemesis since its initial rate hike in March. Nothing spells out ‘foe’ like the following chart from Visual Capitalist.

The Fed is serious. There’s no pivot, just a market of denial.

Certainly, the Fed can slow down the speed and size of rate hikes, but I’ll outline why I believe not only that interest rates may be higher than longer, but also their nebulous 2% inflation target requires revisiting.

According to economist Larry Summers, the Fed’s inflation goal should be 3%. In a report, Joseph Quinlan, head of market strategy for Merrill and Bank of America Private Bank, outlines how the Fed’s 2% target, which began in 1996, was based on the growing popularity of globalization and efficient supply chains. The current target won’t work going forward and requires revision.

One of the best cases for deglobalization is made by Peter Zeihan in his recent book. Click here to watch his analysis.

Currently, the global macro trends appear to be moving in the opposite direction. Deglobalization and structurally upended supply chains are on the horizon for the next economic cycle.

Although we’ve seen some relief to supply chain inflation, the following data convinces me the Fed will remain a market nemesis for longer.

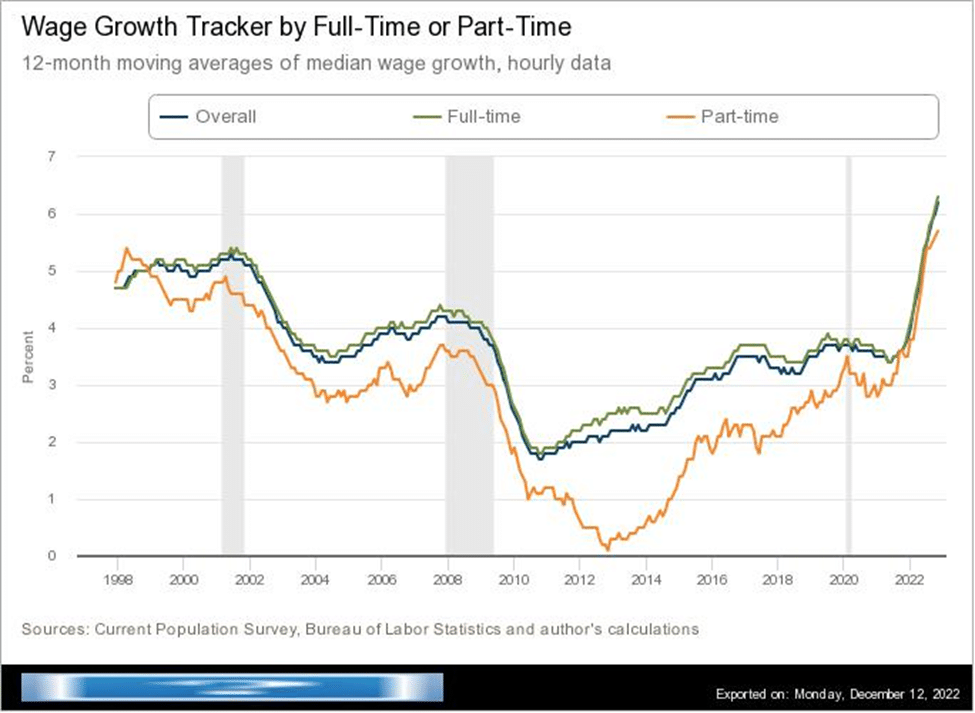

Per the Atlanta Fed’s Wage Growth Tracker, there’s been little relief from wage inflation which tends to be tough to break. After all, once companies raise wages, they don’t tend to retract them.

Trimmed-mean inflation filters out the transitory variation to provide a clearer view of the rate of change and exhibits less real-time bias than ex-food-and-energy core inflation. The trimmed mean is more tightly linked to labor-market slack than headline inflation or the conventional core (per the Federal Reserve Bank of Dallas).

The six-month PCE inflation, the annual rate below, is increasing again.

| May-22 | Jun-22 | Jul-22 | Aug-22 | Sept-22 | Oct-22 | |

| PCE | 7.1 | 8.0 | 6.7 | 6.0 | 4.7 | 5.0 |

| PCE vs. F&E | 5.0 | 5.2 | 4.3 | 4.7 | 4.9 | 4.7 |

| Trimmed mean | 4.5 | 5.0 | 4.5 | 4.8 | 5.0 | 5.1 |

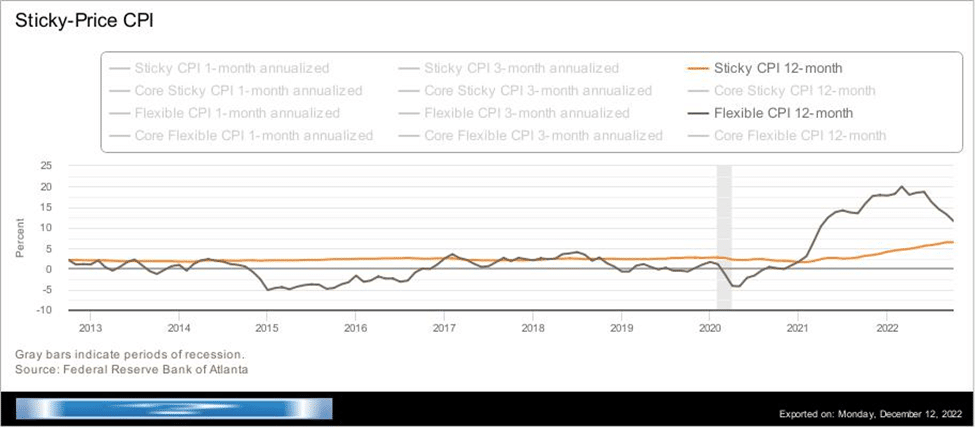

The Atlanta Fed’s Sticky-Price CPI sorts the components of the CPI into flexible or sticky (slow to change).

The News Isn’t All Bad.

On a positive note, flexible prices for goods such as used cars and trucks, cereal, baking products, apparel, and fresh fruit and vegetables are headed in the right direction. However, they still have a way before reverting to longer-term trends. Sticky CPI – prices for rent, water, sewer, and trash collection remain stubborn.

Even in the latest CPI report from December 13, although headed in the right direction, owner-equivalent rents (sticky inflation) increased. From the BLS report:

The index for shelter was by far the largest contributor to the monthly all items increase, more than offsetting decreases in energy indexes. The food index increased 0.5 percent over the month, with the food at home index also rising 0.5 percent. The energy index decreased 1.6 percent over the month as the gasoline index, the natural gas index, and the electricity index all declined.

I won’t say the current report wasn’t an improvement. I will say it’s not enough for the Fed to pivot anytime soon. After all, their target is 2%, and there’s a long way to go. Another reason why you’ll need to understand the three ways to navigate 2023’s greatest unknowns.

Overall, this inflationary condition post-pandemic is a bit of ‘no man’s land’ for economists. Therefore, equity investing will remain volatile through 2023 and continue to shake out weak holders.

In light of this information, here are three ways to navigate 2023’s greatest unknowns.

Place An Investment Foot In The Saver Camp.

Investors and financial professionals have experienced the worst performance in 60/40 portfolios in their investment lifetimes. While the Fed remains an investment foe, it’s an ally to savers.

Stocks haven’t worked (especially growth style), and bonds have been disappointing. So why not allocate a portion of your portfolio to Treasury Bills, high-yield or brokerage CDs from online banks and brokerages, respectively, and investment-grade corporate debt?

Market Timing Doesn’t Work.

All out or all in when it comes to your allocation to stocks is a loser’s game. I work with investors who attempt it. Emotional decisions impact their returns. Second, market timing differs from risk management, which includes minimizing losses and trimming profits based on a rules-based system.

Third, the best market days occur during the most turbulent market cycles. Like some form of torture, to get the highest returns, investors must earn their equity risk premiums by riding the wave, so to speak.

Remember, per JP Morgan, over the last 42 years; markets have fallen 14% during the year yet finish positive 75% of the time. Volatility, as investors have forgotten, is the price of market admission. With the Fed as a foe, investors are reminded of this fact.

Rate Volatility And Market Volatility Are Connected.

Last, it’s through these times I’d rather ride a hobby horse vs. a T-Rex. Therefore, shrinking the portfolio allocation to stocks, building cash, or utilizing short-term fixed-income instruments, could bolster you in your seat during the ride. Remember, you mount your investment saddle on a tamer beast when the Fed is a foe.

Speaking of tamer horses: Synchrony offers a 15-month certificate of deposit at 4.5% APY. A 3-month Treasury bill has a yield-to-maturity of 4.4%. See where I’m going?

When the Fed isn’t your friend as an investor, the best we can do is take a lesson from savers and consider how they’re like kids in a candy store at this juncture, and we like candy too!

Prepare For A Hard Landing.

Many investors were not prepared emotionally for this year’s market ride. I hope they can get their emotions in check for 2023. It’s rare to impossible for the Fed to navigate a soft landing. So, preparing for the worst regarding your emotional response to market volatility is best.

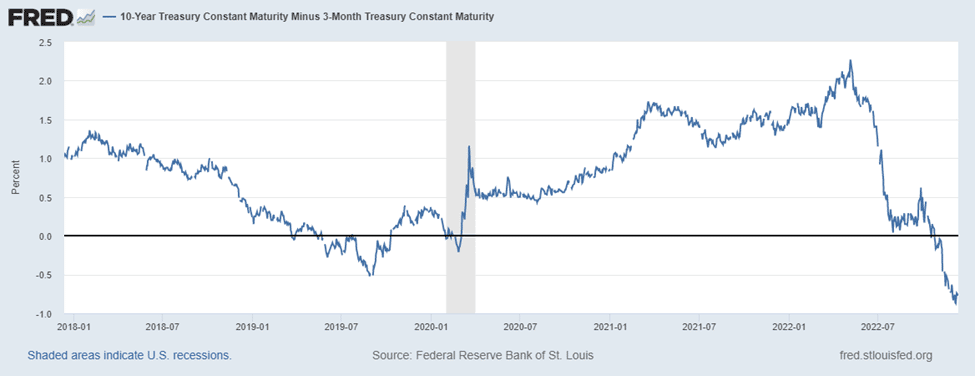

Per Jonathan Pain, author of the Pain Report and Director of JP Consulting NSW Pty Ltd, the metric worth your attention is the 3-month vs. 10-year yield inversion.

Here it is currently:

Jonathan mentions that the type of inversion above has preceded every recession since 1960. On average, a recession followed in 16 months. Although there was one false signal in 1966. Due to fiscal spending for the Vietnam war, a recession was averted. Notice the inversion currently vs. 2019.

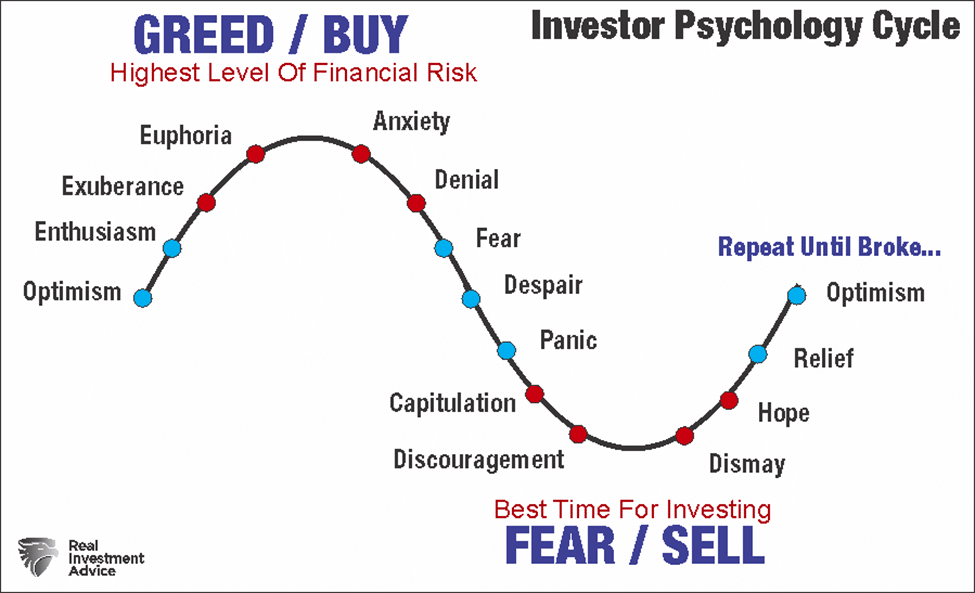

Our Gut And Market Cycles Don’t Mix.

Currently, I believe we’re vacillating between anxiety and despair. The endless talk of a Fed pivot, a slight improvement in inflation, and reluctance to decrease 2023 S&P earnings estimates have kept our ‘lizard brains’ in a consistent state of manic but just not negative enough. Next year, we may find our emotions in the basement of capitulation and then discouragement. At these times, we should commit capital to stocks (just when we don’t want to).

Active Management May Be Back

Financial professionals have done a magnificent job of selling products or outsourcing money management which ostensibly distances themselves from ground zero of an imminent explosion (hey, it’s the market, not me), to possibly re-think their careers. Take on a fiduciary calling.

Perhaps a bear market is required to cleanse the system and drain the swamp by migrating miscreants to more fitting livelihoods like pushing phone service deals at T-Mobile or taking roles as activities directors for Carnival Cruise Lines. We’re due.

The front-line consultant of a publicly-traded big box financial retailer is under never-ending pressure to increase shareholders’ margins. The performance of the stock price is the priority. I have never forgotten this lesson from working on the brokerage side of the fence.

Active Investing To Navigate 2023.

With Fed as a foe, passive indexing may not perform as well as good, old-fashioned balance sheet, cash flow, and income statement analysis. Understanding equity balance sheets, cash flows, and dividend growth models and creating rules to help clients navigate risk can be rewarding for financial professionals.

In addition, investors will learn that investing solely to beat some arbitrary index is a fool’s game. What’s the point? To provide conversation fodder for holiday parties?

Financial Planning To The Rescue!

I’ll beat the drum again over comprehensive financial planning whereby investors get to know their PRR or personal rate of return required to meet specific, goals-based milestones such as retirement or saving for college.

For example, If your PRR is 3.62%, then we know, as planners and asset allocators, that there’s no need to take on additional risk than necessary.

Overall, I expect 2023 to be an investing challenge and an inevitable recession. I hope I’m wrong. The three ways to navigate 2023’s greatest unknowns should provide some guidance.

In the meantime, here’s some sage commentary from my favorite Bloomberg Opinion columnist:

The Fed has told us very clearly that it’s more hawkish than we thought, and it’s inherently very dangerous to ignore it.

Read his full commentary here.