Trending

Written by: David Lebovitz

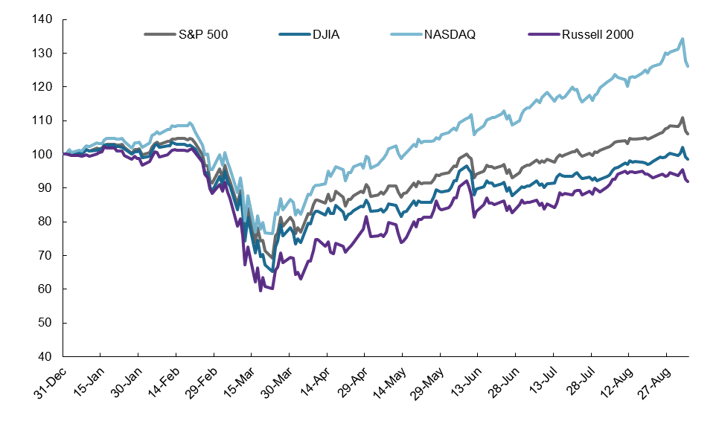

After a strong run, the end of last week saw U.S. equity markets come under pressure. This caught some investors off guard, as U.S. case growth had been slowing, the 2Q20 earnings season was better than expected and the economic data had been surprising to the upside. Specifically, technology stocks, which had been untouchable in recent months, led the move lower. Is this a healthy pullback within the context of a broader bull market? Or is it the beginning of a broader downturn?

By our lights, recent market action represents a healthy consolidation. It appears that some of this price action may have been technical in nature, as positioning was extended and valuations were rich. Furthermore, credit spreads have been relatively stable and the outlook for earnings has not materially changed; this suggests that fundamental risks are limited, and that this change in market behavior should not necessarily be viewed as a harbinger of things to come.

The bottom line, however, is that volatility looks set to persist. The immediate issue facing investors is how monetary and fiscal policy will evolve in the coming months, as a continuation of the recovery requires current policies to remain in place. While the Federal Open Market Committee (FOMC) has suggested it is comfortable allowing the economy to run hot, thereby implying an accommodative stance for the foreseeable future, the fiscal side of things has left something to be desired. We still expect more fiscal stimulus in the coming weeks, as neither party wants to be seen as impeding a deal in the run-up to the election; once a deal is done, however, investor focus will shift to the November election.

The market is gradually becoming more comfortable with the virus itself, but that means the trajectory of policy, profits and the economy will become increasingly important. Spending on consumer goods has rebounded strongly in recent months, and it appears that an inventory build may be underway. On the other hand, the services side of the economy is yet to fully come back online. With that as the backdrop, we expect that value and cyclicals will outperform as the economy continues to show signs of improvement, whereas more structural trends should support technology and growth stocks over the longer-run.

Technology and growth names finally coming under material pressure

Price levels, indexed to 100 on 12/31/19