Trending

A few years ago, Paul Wallace penned an article entitled: “GDP Is A Grossly Defective Product.” The recent release of the Q2-2020 report reminded me of it as the media fawned over the 7.6% print.

“Yet despite its theoretical appeal, GDP is, in practice, a fallible measure. It is increasingly becoming one that could be described as a grossly defective product.

While seemingly strong at the headline, the recent report leaves much to be desired when looking below the surface.

Estimates Missed By A Mile

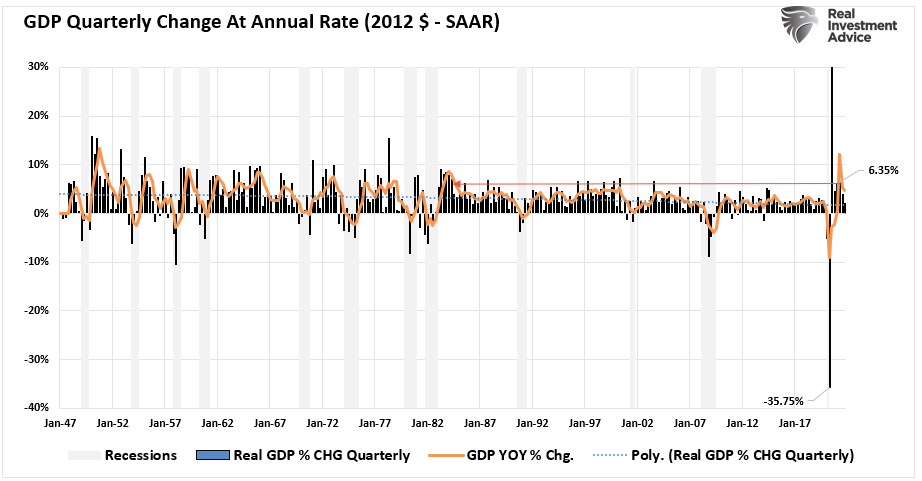

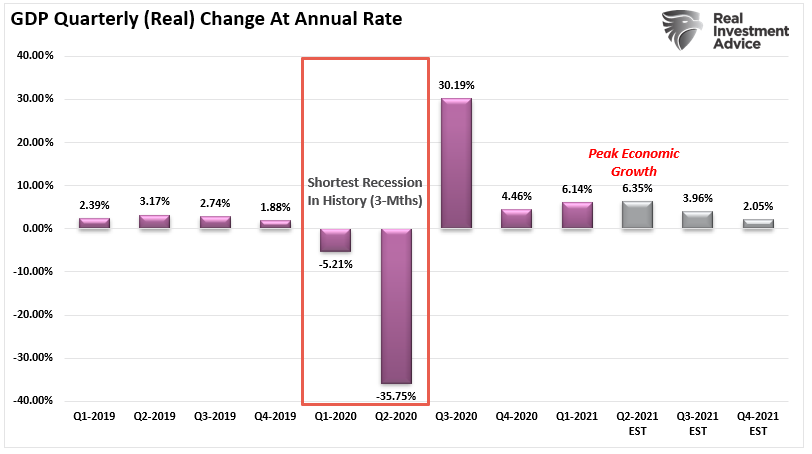

The headline print of 6.35% was one of the most robust rates of “annualized” growth since the early 1980s. However, there are two significant takeaways from this data. First, while the growth rate is impressive, it is $5 trillion in Government spending during the recession that boosted growth. (Chart below is current through Q2 and estimated through Q4)

Secondly, the growth rate is substantially weaker than earlier estimates of more than 13% and a full percentage point lower than the Atlanta Fed’s GDPNow forecast of 7.6%. It also likely represents the peak of the economic recovery. (This is a topic we will address more next week.)

Over the next two quarters, the rates of economic growth will continue to weaken. Such will be due to the massive amounts of direct stimulus fading from the system.

By late 2022 the economic growth rate will likely set a new lower growth trend below 2%. Such will be weaker than the growth trends before the past two “real” economic recessions.

As is always the case, economists and analysts are always overly optimistic in their assessments. But, while being overly optimistic is undoubtedly a media preference, it leads to potential misallocations of capital by investors.

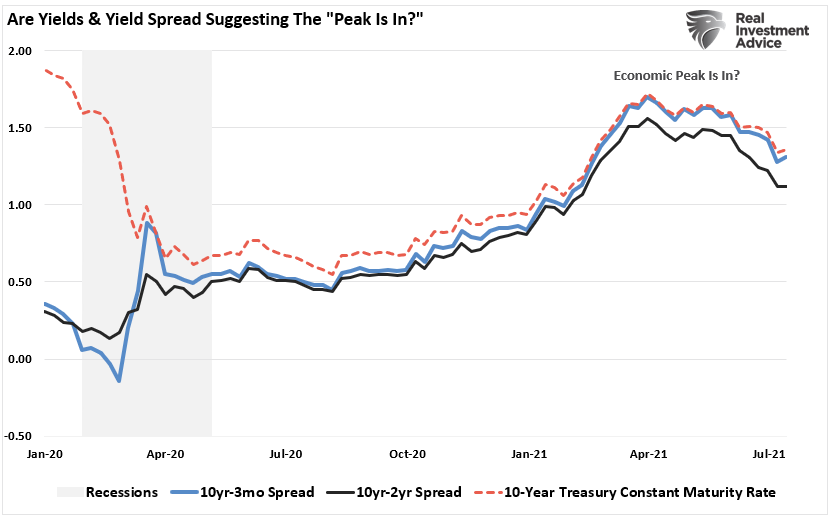

Yields Had It Right After All

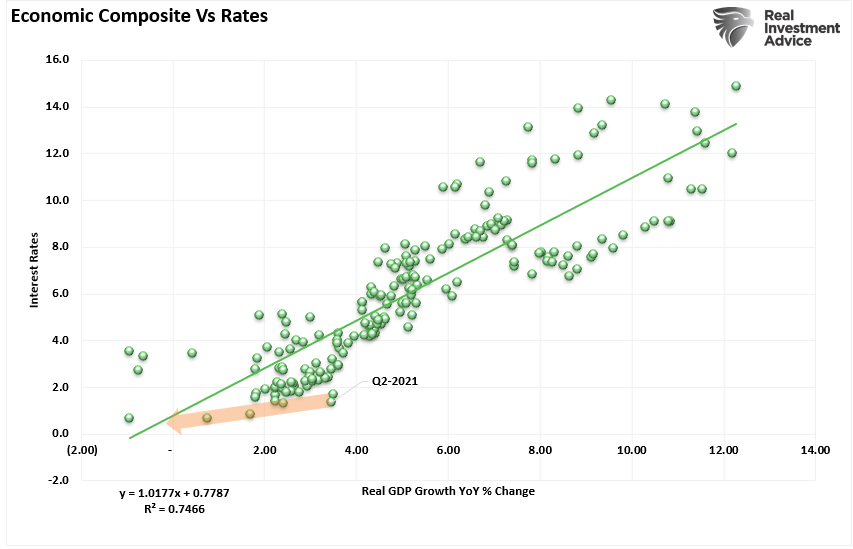

As discussed in April, when estimates were for 13% GDP growth, bond yields signaled a peak of economic growth. To wit:

“As shown, the correlation between rates and the economic composite suggests current expectations of economic expansion are overly optimistic. At current rates, economic growth will likely very quickly return to sub-2% growth by 2022.”

Since then, yields have continued to drop, along with the yield curve flattening. Historically, yields are a strong predictor of economic growth and inflation. However, as stated previously, disinflation is more likely than accelerating inflation.

“With the base effects now exhausted, the cyclical, structural, and monetary considerations suggest inflation will decline by year-end. Thus, the ‘inflationary psychosis’ gripping the bond market already reversed as the realization of slower economic growth occurs.”

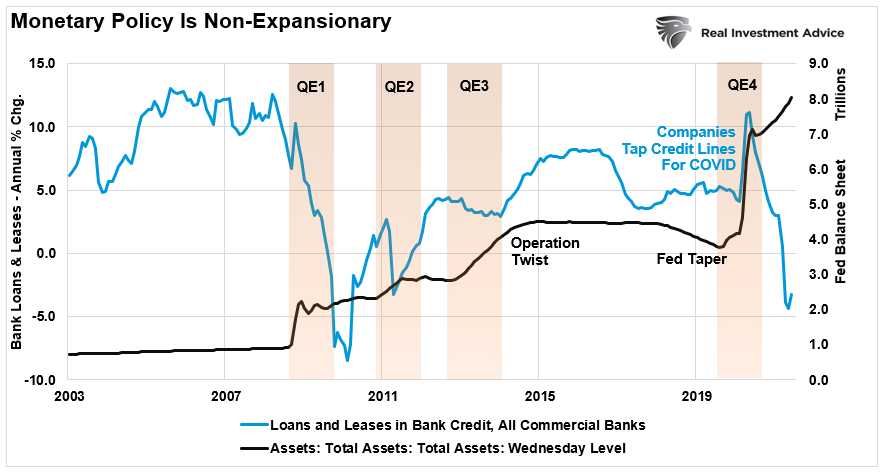

Of course, such is problematic for the Federal Reserve. The current program of $120 billion a month in monetary injections only maintains economic growth. But, unfortunately, those monetary interventions are not translating into “economic activity” either directly or indirectly.

“Each time the Fed has engaged in QE programs, the banks ‘hoard’ those reserves as the ‘risk/reward’ of loaning money into the economy is not justified. For example, in early 2020, as the economy was ‘shut down’ due to the COVID pandemic, companies tapped credit lines at their banks to ensure sufficient capitalization. After that initial surge in lending activity, banks reversed back into a more ‘protectionary’ mode.”

QE programs have NOT been effective at creating organic economic growth. However, they were effective at boosting asset prices and providing an illusory wealth effect.

The Fed faces a challenge in trying to “taper” asset purchases. While there is more robust economic growth, a bubbling housing market, and falling unemployment, can they remove the economic “life support?” Some alternative measures suggest such may not be the case.

Alternative Measures Of Economic Growth

While mainstream economists suggest the economy is booming based on the more mainstream economic data, other data suggests such may not be the case.

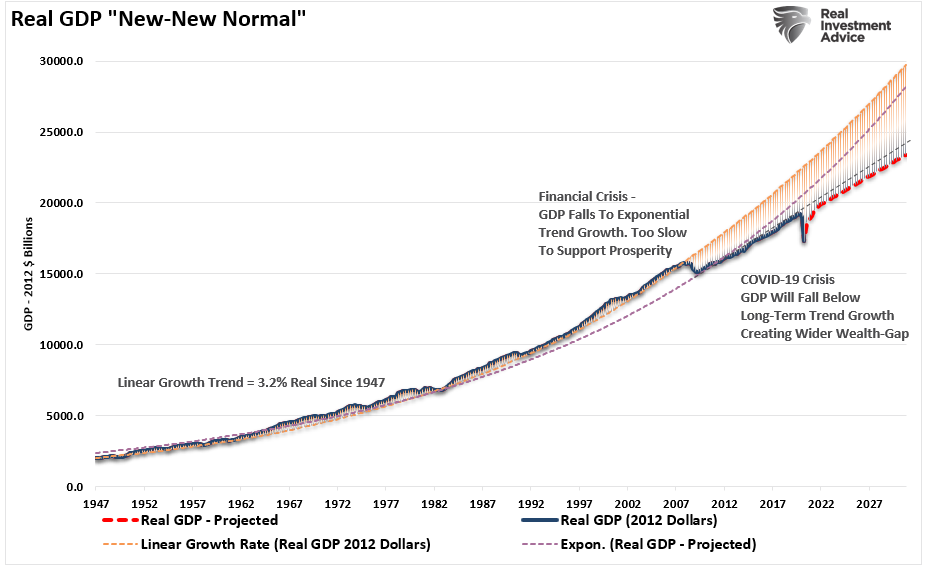

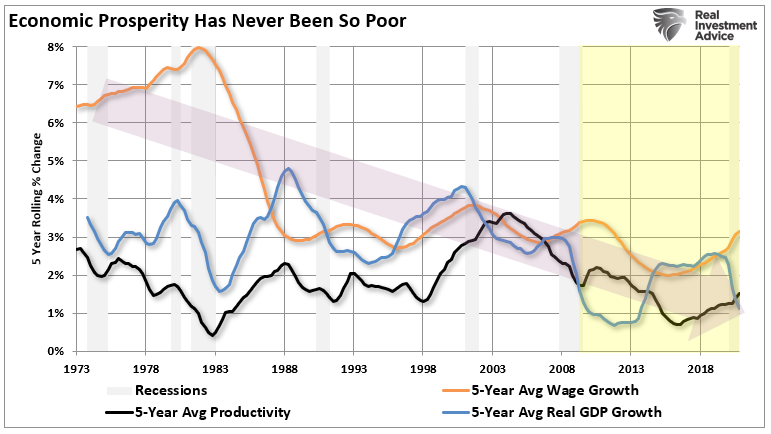

It is important to note that America’s economic performance peaked in the late 1990s. Thus, the erosion in crucial economic indicators such as the rate of economic growth, productivity growth, job growth, and investment began well before the Great Recession.

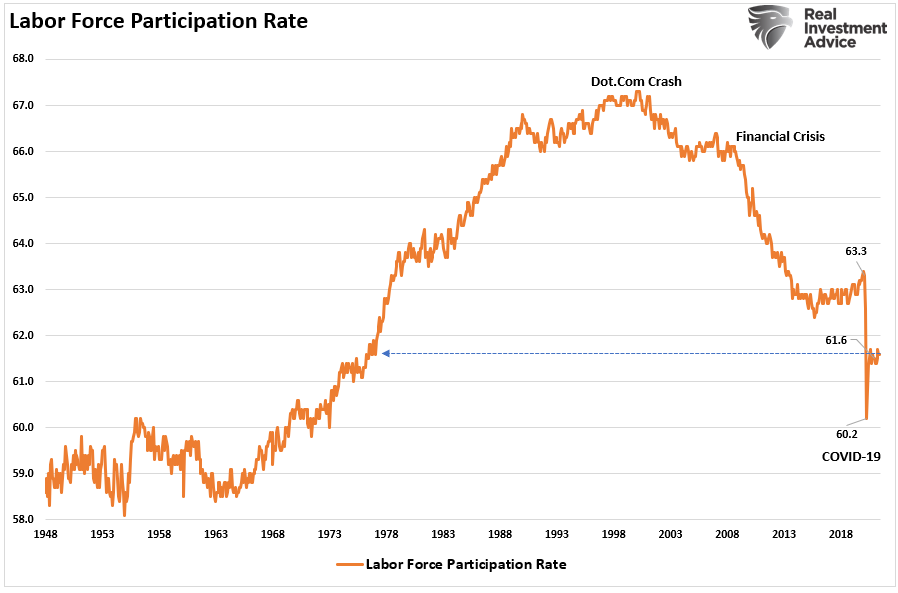

A look at labor force participation, the proportion of Americans in the productive workforce peaked in 1997.

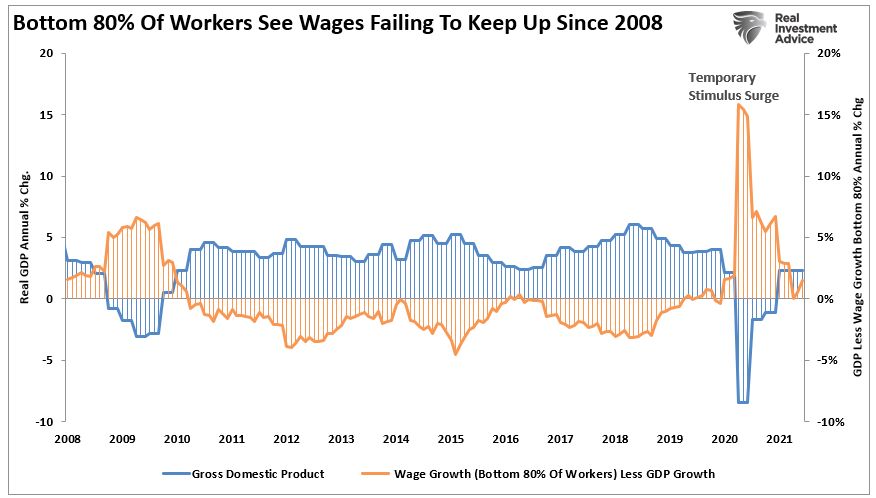

With fewer working-age men and women in the workforce, per-capita income continues to decline. Not surprisingly, median real household income remains muted well below the actual cost of living, with incomes stagnating across the bottom 80% of income earners.

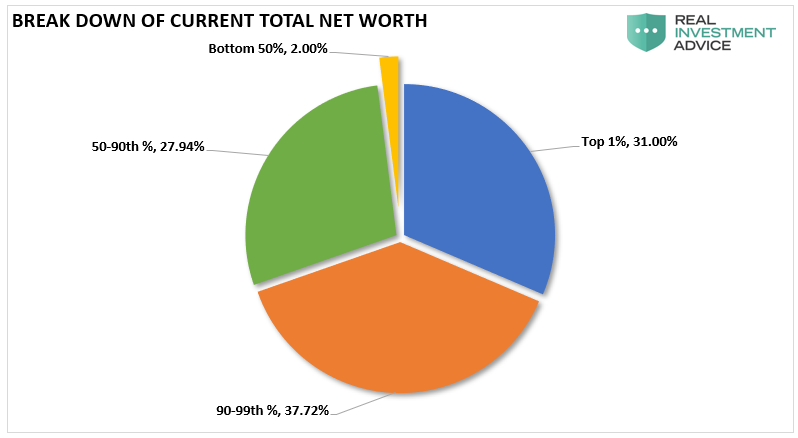

Moreover, stagnating income and limited job prospects have disproportionately affected lower-income and lower-skilled Americans, leading to household inequality.

Lastly, the U.S. lacks an economic strategy, especially at the federal and Governmental levels. The implicit strategy remains trusting the Federal Reserve to solve our problems through monetary policy. However, the rise in wealth inequality has fostered demands to transform the U.S. into a “socialistic” economy.

Neither strategy has ever solved the problems of those with the least who were promised the most.

Conclusion

As noted, the Federal Reserve is trapped. The Federal Reserve needs more substantial economic growth to justify raising interest rates. After all, the reason the Fed tightens monetary policy is to SLOW economic growth to mitigate the potential of surging inflationary pressures. The problem currently is that the Fed is discussing raising interest rates in an environment of weakening economic growth and disinflationary headwinds.

Currently, employment and wage growth remain weak, 1-in-3 Americans are on Government subsidies, and the majority of American’s are living paycheck-to-paycheck. Such is why Central Banks, globally, are aggressively monetizing debt to keep growth from stalling out. However, many analysts and economists have currently increased the odds of the Fed hiking rates by next year. The belief is that economic growth can continue to accelerate despite the tighter monetary policy.

Most of the analysis overlooks the level of economic growth at the beginning of interest rate hikes. The Federal Reserve uses monetary policy tools to slow economic growth and ease inflationary pressures by tightening monetary supply. For the last decade, the Federal Reserve has flooded the financial system to boost asset prices in hopes of spurring economic growth and inflation.

As stated, outside of inflated asset prices, there is little evidence of real economic growth as witnessed by an average annual GDP growth rate of just 1.1%.

While the mainstream media may indeed tout the “greatest economic growth rate in decades,” the pervasive weakness below the headlines will continue to erode projections.

The problem for investors is the inflation of assets prices far beyond what the actual economy can generate in terms of future revenue and earnings growth.

The re-alignment between overly bullish expectations and a “Grossly Defective Product” will likely be more painful than most expect.

Related: The Markets Next “Minsky Moment”