S&P 500 duly rose on the little weaker than expected non-farm payrolls as the taper theme (start of discussions moving to serious contemplation) got dialed back. The Fed‘s forward guidance manouevers can continue, and inflation trades breathed a sigh of relief. Encouragingly for the S&P 500, reflation trades weren‘t affected as evidenced by value stocks rising again regardles of the long-dated Treasuries action.

Of course, volatility welcomed the retreat in yields as much as technology did – but the option traders aren‘t buying into the upswing nearly as much. Practically speaking, Friday‘s moves in the dollar, some commodities and precious metals, reversed a great chunk of the preceding day‘s bigger swings. The guessing game on the Fed‘s taper goes on, and the upcoming CPI readings won‘t add to the markets‘ peace. Most likely, fuelling the sense of taper urgency as the inflation figures won‘t be coming on the low side. Add in the job market slowly catching fire, and you‘ll understand why I have been calling for months for elevated inflation readings.

It‘s the market reaction what matters – what is at stake, is how much the Fed is still expected to fight inflation, whether it plays ostrich in toeing the transitory line much to the satisfaction or dismay of the marketplace. As I wrote on Friday:

(…) Should the transition into a higher inflation environment be appreciated for what it is, the dive in gold, silver and copper wouldn‘t have been that steep. On the other hand, the sharpest moves tend to be the countertrend ones – yes, I‘m still of the opinion that the current reflationary period with reopening rush (more juice left in value over growth trades) is conducive to higher stock market and commodity prices. Including precious metals, naturally.

Moreover, the taper talk (...is…) exposing a key vulnerability in the Treasury market. The Fed is well aware that its ample support is a condition sine qua non, and that rising yields (rising real rates) aren‘t in the largest borrower and real economy‘s interests. Financial repression has to come into the picture, and that‘s one of the reasons why precious metals have been on a tear lately. We‘re also a long way from inflation breaking the back of stock market bulls.

So stocks have taken the risk-on cue, amply reversing Thursday‘s losses – but the same can‘t be said about gold, silver or copper. Precious metals pared Thursday‘s setback to a good degree only, and these words apply to miners as well. Not that conducive conditions hadn‘t been in place to facilitate more gains, but the optimism over Fed moves being dialed back to a more distant future, is more guarded. Understandably so when Janet Yellen would welcome higher inflation and higher rates as per her G7 meeting proclamation. The bulls aren‘t out of the woods – all eyes on nominal yields, inflation expectations and the dollar now.

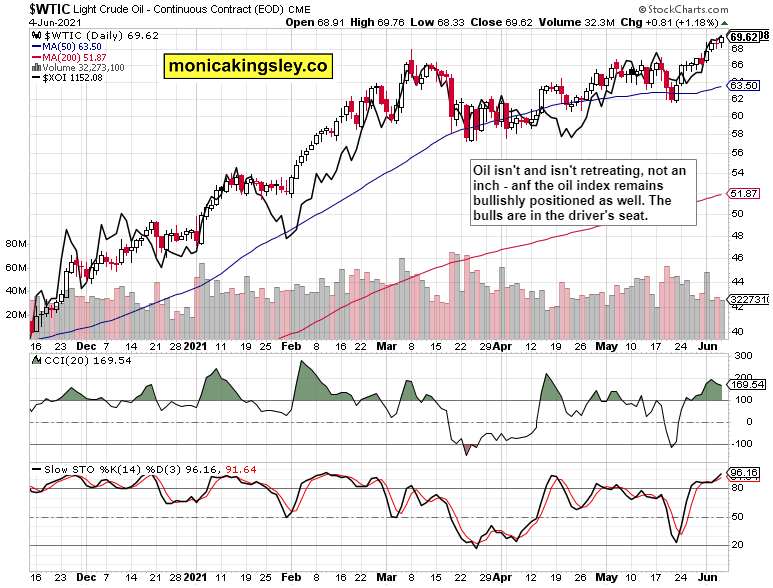

Oil is refusing to budge, and the oil index doesn‘t favor too much downside. Should commodities stall again though, oil would be no exception – in spite of its next upleg getting underway after the long sideways consolidation (with a bullish slant, however).

Cryptos can‘t get their mojo, but aren‘t falling through the floor either. The consolidation goes on, and bulls better step in and overcome Thursday‘s highs for the recovery to continue. That‘s not unimaginable for Ethereum or Cardano, though – it‘s only that Bitcoin is acting really weak relatively speaking.

Let‘s move right into the charts (all courtesy of www.stockcharts.com).

S&P 500 and Nasdaq Outlook

Both S&P 500 and Nasdaq 100 grew sharply, and if you look under the hood, the signals are positive. If only higher volume confirmed them.

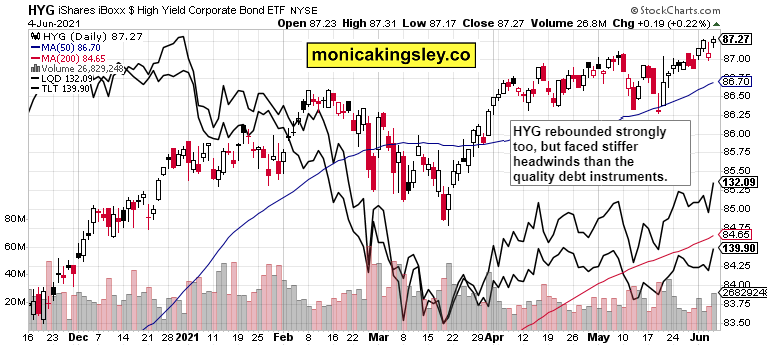

Credit Markets

HIgh yield corporate bonds met an intraday setback, which is part of the short-term watchouts.

Technology and Value

Technology including $NYFANG dialed back Thursday‘s overreaction – just as was likely, and the value stocks confirming in the upswing stretching over to high beta plays in tech as well, are a positive sign for Monday.

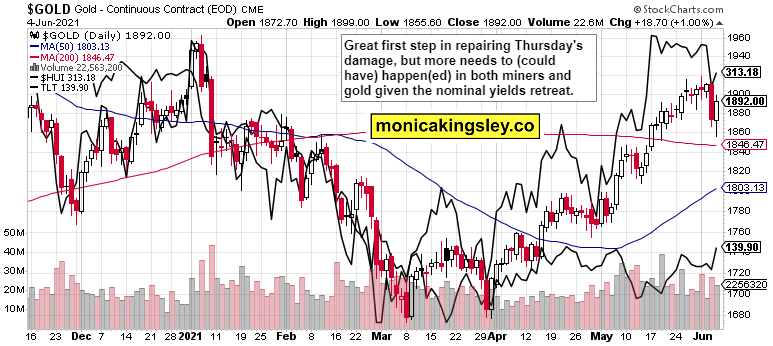

Gold, Silver and Miners

It‘s nice that gold recovered from yet another dive but, its white candle could have closed nearer to the daily highs – it‘s concerning that it didn‘t, and the same applies to miners. The return of strength has been suboptimal when nominal rates solely are assessed. Of course, that ties in to the retreat in inflation expectations being the other side of the coin, coupled with rising rates expectation underpinning the dollar.

Silver recovered stronger than copper, but the red metal‘s ratio enriched with 10-year Treasury yield view, could have driven stronger gold gains. However, silver‘s outperformance isn‘t worrying here.

Crude Oil

Crude oil is continuing its low volatility rise, volume isn‘t drying up, and the oil index supports the upleg to proceed.

Summary

S&P 500 bears got on the defensive again, and credit markets give the bulls benefit of the doubt. How will another attempt at all time highs unfold, is to be closely observed for signs of strength / weakness.

Gold and silver remarkably rebounded, but could have recouped even more of Thursday‘s losses. It remains a (short-term) red flag they didn‘t. The bulls haven‘t proved themselves entirely, which can be explained by yields, inflation and dollar.dynamics.

Crude oil bullish chart message hasn‘t weakened one iota on Friday, and black gold‘s upleg remains underway – while a meaningful correction isn‘t favored, taking a breather would be healthy.

Bitcoin and Ethereum meek recovery, bottom searching after Elon‘s broken heart emoji tweet goes on, and the Miami show didn‘t help much. The longer prices stay this low without steadily attempting a march higher, the more vulnerable they are.

Thank you for having read today‘s free analysis, which is available in full at my homesite. There, you can subscribe to the free Monica‘s Insider Club, which features real-time trade calls and intraday updates for all the four publications: Stock Trading Signals, Gold Trading Signals, Oil Trading Signals and Bitcoin Trading Signals.

Related: When Markets Get Scared and Reverse

The views and opinions expressed in this article are those of the contributor, and do not represent the views of IRIS Media Works and Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.