Trending

Written by: Jordan Jackson

Numerous data suggests the U.S. economy will enter a recession in the next 12 months; 46% of professional forecasters in the Philadelphia Fed Survey project a recession, the Conference Board recession probability model predicts a 96% likelihood of recession, and the U.S. Treasury yield curve is deeply inverted which has been a decent predictor of prior recessions. With these indicators all flashing red and the Global Financial Crisis still fresh in investors’ minds, market participants are concerned how the banking industry might fair in the next economic downturn?

Every year the Federal Reserve conducts a rigorous stress test to assess how large banks are likely to perform under a hypothetical recession. The severely adverse scenario implies the unemployment rate peaks at 10% by the third quarter of 2023, real GDP declines by more than 3.5% from 4Q21 to 1Q23, and steep declines in asset prices across stocks, bonds, and real estate. This years’ stress test shows that large banks have sufficient capital to absorb losses and can continue lending to households and businesses under this stressed scenario1.

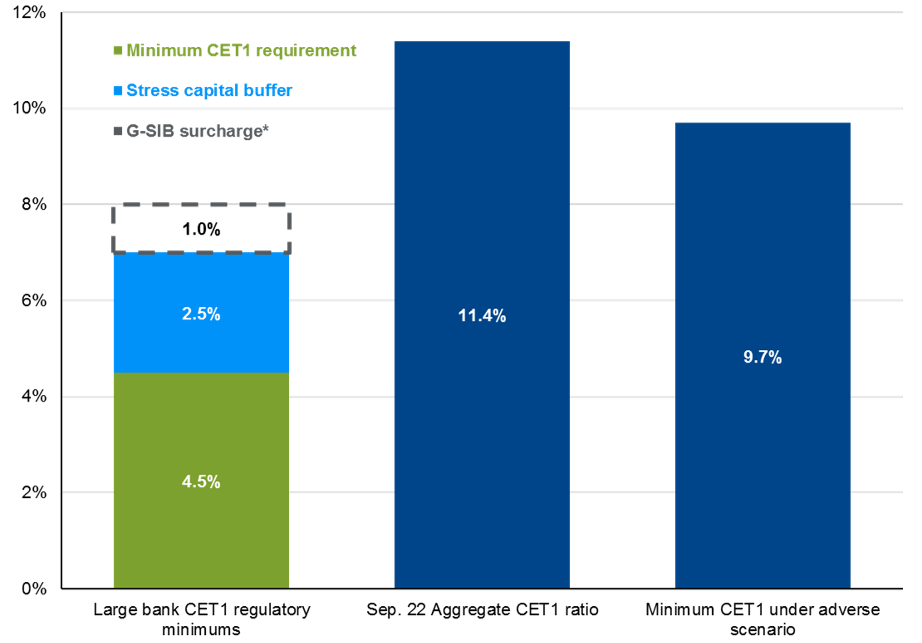

An important metric in this stress test is common equity tier 1 capital ratio (CET1), a measure of a bank’s core equity capital compared with its total risk-weighted assets. While each bank is subject to individual capital requirements, the baseline requirements consist of the following components:

- The minimum CET1 ratio at 4.5%2;

- The stress capital buffer (SCB) requirement of at least 2.5%3; and

- If applicable, a capital surcharge for global systemically important banks (G-SIBs) at 1%.

As shown, even under the severely adverse scenario capital requirements would still be adequate to meet regulatory minimums, and aggregate CET1 ratio is currently at 11.4%4. In addition, banks have been conservative with the third quarter marking the sixth consecutive quarter of a build-up in loan loss reserves, further strengthening the buffer banks have to offset an economic downturn.

Banks appear to be well capitalized to weather a recession

Common equity tier 1 capital ratios

Source: Federal Reserve, J.P. Morgan Asset Management. 33 banks participated in the Federal Reserve's 2022 Stress Test. Large bank capital requirements are as of October 1, 2022. *Eight of the 33 banks are subject to the G-SIB surcharge. Data are as of November 29, 2022.