As many advice businesses reach maturity it is common to consider whether they should “buy to grow”. Should they buy another practice, or more commonly, should just buy a book of business from another practice.

The typical reasons suggested for wanting to grow through acquisition are:

- Get new clients to “cross-sell” to

- Increase business turnover

- Increased cost efficiency

- Diversify business lines

- Enhance market position or scale

Generally the majority of transactions in financial services are valued on some form of a multiple of sustainable earnings. This is most often a “rule of thumb” type approach, where a multiple is applied to the passive income stream that the target business promises (which is fair enough). It seems that an “acceptable” multiple continually gets used by purchasers without any genuine consideration being given to either the cost of integration or the inherent value that the other business can actually bring.

Thinking like an investor who is applying capital for the long term, as opposed to someone judging an acquisition simply on its ability to introduce volume of one sort or another (clients; revenue; production; etc), will result in coming up with a valuation multiple which reflects its actual worth to you, rather than a value which the market has universally agreed to “be fair for all business of that type”.

The sort of questions and considerations which should arise in determining what the value of another business is to you would be:

How well matched are the two businesses really?

How easy are they to bring together, and how well do they complement each other?

There are any number of areas to consider, and you might begin with:

- Is it just an asset purchase, or are you looking to buy a business as a “going concern”? If so, what contingent and latent liabilities are lurking about, and what additional risks are being introduced?

- Similarity of client profiles between the businesses: are the types of clients being brought in ones whom you are likely to be able to develop professional relationships with quickly and easily?

- Geographical spread of business: what logistical issues are potentially being introduced?

- Demographics & statistics: average ages, portfolio size, product penetration or fee agreements….how do the numbers actually look in comparison to your own practice and other potential purchases?

- Advice philosophy & values – how do product & process & philosophy work in each business, and do any differences represent opportunity or threat?

- Business relationships – suppliers, research, IT, transferable centres of influence or marketing arrangements….what opportunities can be unlocked which don’t have a particular valuation included in the asking price?

- Data management and CRM systems: will they fit together easily and quickly, and without significant data loss, or is it a potential nightmare? Or will you have to run multiple systems?

- Workflow and advice processes – are they similar, or is substantial change required somewhere?

- Staffing – duplication of roles & responsibilities; individual skill sets; desired skill sets – how will they fit (if at all)?

- Are there any “turnkey” or proprietary solutions that you are purchasing from the target business which would or could enhance your own existing business? Or produce the opportunity to leverage into other areas or in other ways

The better they are matched, and the easier & better the integration, then higher the potential value should be.

This type of analysis is in reality just a starting point however in understanding how the two businesses may mesh. Having done that one can reasonably begin to assess the cost and the benefits of integrating the businesses. Be aware that the majority of purchasers do seem to optimistically over-estimate the “synergies”, or benefits from the acquisition – and often seriously underestimate (or do not understand) the actual costs in terms of lost productivity impact and additional marketing requirements for a prolonged period.

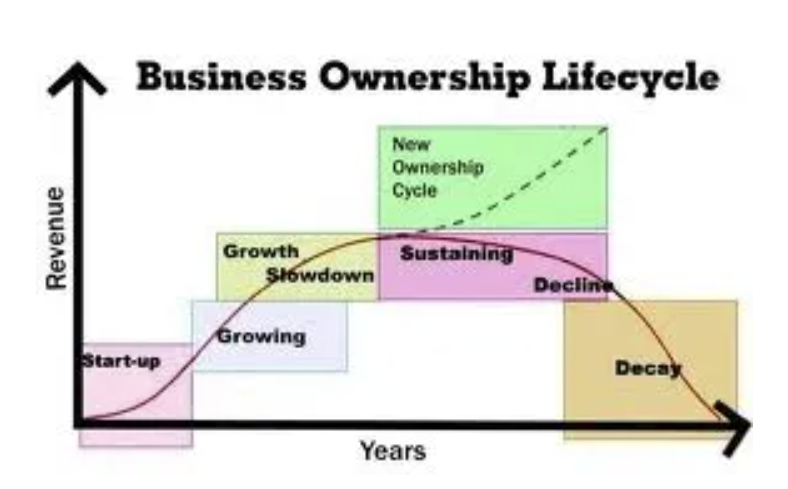

The single most important thing to my mind though is that relatively few prospective purchasers seem to have formed a clear view or understanding of what stage the target business is at in it’s business lifecycle and as a consequence they seriously misjudge expected gains.

There is nothing at all wrong with purchasing a business that is perhaps heading into decline – provided you understand that decline is the inevitable path unless you have a good strategy for how to re-invigorate it. Buying a business in decline is fine, if there is a good turn-around strategy underpinning the purchase.

Even if the target business looks to have moved into some self-sustaining cash-cow mode and has little organic growth within it, there may still be solid rationale to pay a premium price for it. If the business can seamlessly be added to your own business, with highly complementary systems and data management, and opens up the opportunity for your (superior?) advice proposition to unlock latent value….then it may well be worth a superior valuation.

However, simply valuing a book of clients or an advisory business on an “accepted” industry multiple, without any understanding of how or where superior value from the purchase can be derived makes little sense.