Trending

Delivering the right advice consists of getting 2 things right:

- Delivering advice that will work for the client, and

- Delivering it in a manner which will result in the client taking action upon the advice.

Getting both of those right is no simple thing. The first of them is relatively straightforward (although not “easy”) in that this is in essence the distillation of the advisers technical knowledge, competency and understanding of the client and their situation.

So when I say it is straightforward that is only in the sense that competing in an ironman event might be. I’ve never done an ironman event and am never likely to, but it is something way beyond a marathon…way beyond being just an endurance test. A heck of a lot of skills come into play during the event, and a heck of a lot of preparation goes into getting into the event, and then a hundred things have to go right during the event if you want a great result. That’s pretty straightforward, huh? Getting the technical part of financial advice right – or advice that will work for a client – is rather like that it seems to me.

EVEN IF you get all of those bits right though, there is one more tough part to get right, and it is arguably the toughest part of the advisers role:

Delivering the right advice in the right way for it to be acted upon. Because great advice which is not acted upon has no particular value.

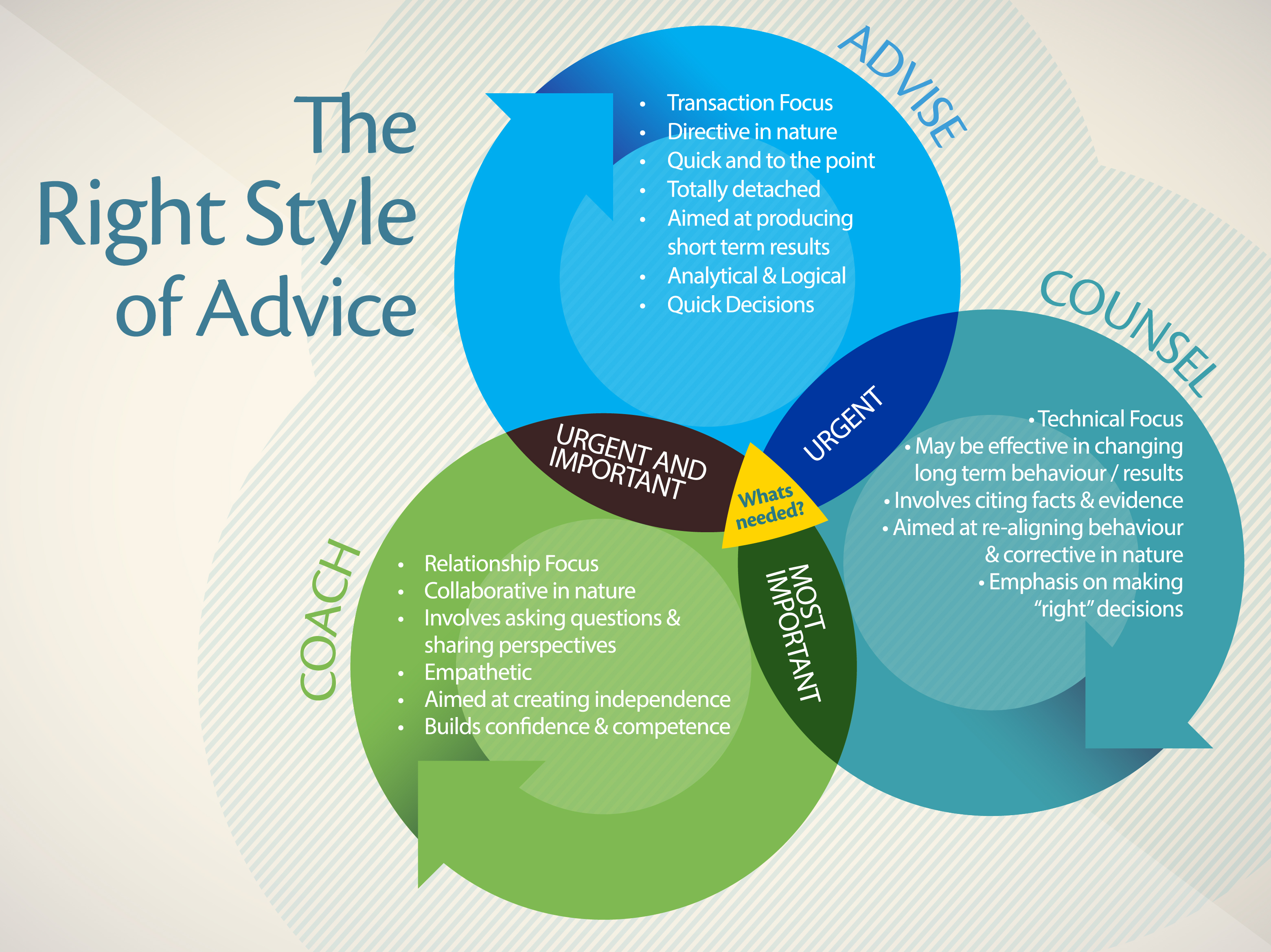

I’ve learned (the hard way!) over the years that generally there are three styles of advice delivery, and each of them can be utterly ineffective when used at the wrong time. Equally, each of them has a time when they are the only way to effectively deliver advice.

There are times when a client is primarily driven by “urgency”. A resolution or solution is required fairly quickly, or there are limitations imposed upon the advice process by the client. That often takes the form of an instruction being delivered, such as “the bank says I need to do…..” and what follows is the client only wants done what is required to keep their new lender happy for example.

There is no grand plan, or desire to deal with long term goals or wider implications. Someone just wants the job of the moment done.

On these occasions the ideal style is to advise. That means tell them the answer, or provide the solution as rapidly as possible. Remain objective and somewhat detached, and lean upon analysis and logic to drive the recommendation. It is the classic “give the customer what he or she wants” position.

There are times however when there is a desire to get it right, rather than just get it done. The decision of the moment for the client IS wrapped up with and amongst other financial decisions that they have made and will make in the future. It is an important decision for them, and as such the style of delivery which works best is to counsel the client. A counsellor still has a strong technical focus and a leaning upon facts and logic in providing the advice, but it is a more strategic role. The key objective is on getting decisions as right as possible in a much wider context, and that will involve managing behaviours and habits as much as finding solutions, but the emphasis does lean towards the technical rather than behavioural.

Then there is the coaching role, where the main emphasis is upon helping the client become self-sufficient ultimately. Mainly this style of delivery is about shaping behaviour and building confidence. The technical aspects of financial advice are important, but absolutely secondary to the need to manage a human more than the financial plan.

These primary roles, or types of advice delivery, are clearly quite different in approach and emphasis. The real challenge though is knowing how and when to blend the styles, and that requirement is far more common that adopting one style absolutely for the duration of an engagement.

Understanding which styles blend well comes down to understanding what type of engagement we are dealing with. The areas of overlap in the diagram show how and where the styles blend well for the type of engagement we are dealing with.

It is worth remembering that “an engagement” in this context is not “the client relationship” – it is the requirement for advice by a client at any given time during the entire business relationship. That means that at times clients will have needs which are essentially urgent, and the best style of advice delivery is a combination of counselling and pure objective advice. The same client a year or two down the track and in different circumstances might well be grappling with a significant issue which does require a relatively quick decision but which is also a critical factor in their long term planning. On such occasions there is typically a requirement to coach the client while also providing specific detailed advice.

What is needed by any particular client at any given time in an advisers relationship with them will fluctuate. There will be times when the client leans upon good technical expertise and rapid recommendations. There will be times when the adviser is providing far more strategic advice coupled with transferring skills and developing competence in the client to self-manage aspects of their affairs.

Great advisers understand what they are dealing with on each occasion that they are interacting with a client, and quickly moving to the style of delivery which is going to achieve the 2 primary objectives: giving advice that will work, and advice which will also be acted upon.

We need to achieve both if we are truly making a positive impact in clients lives and create value.