Trending

Here’s a little secret some of the world’s wealthiest people use to expand their fortunes…

It’s something I personally use to grow The Advisor Coach…

And it’s a way for financial advisors to set more appointments and get more clients.

Would you like to know what it is?

Okay, here it is…

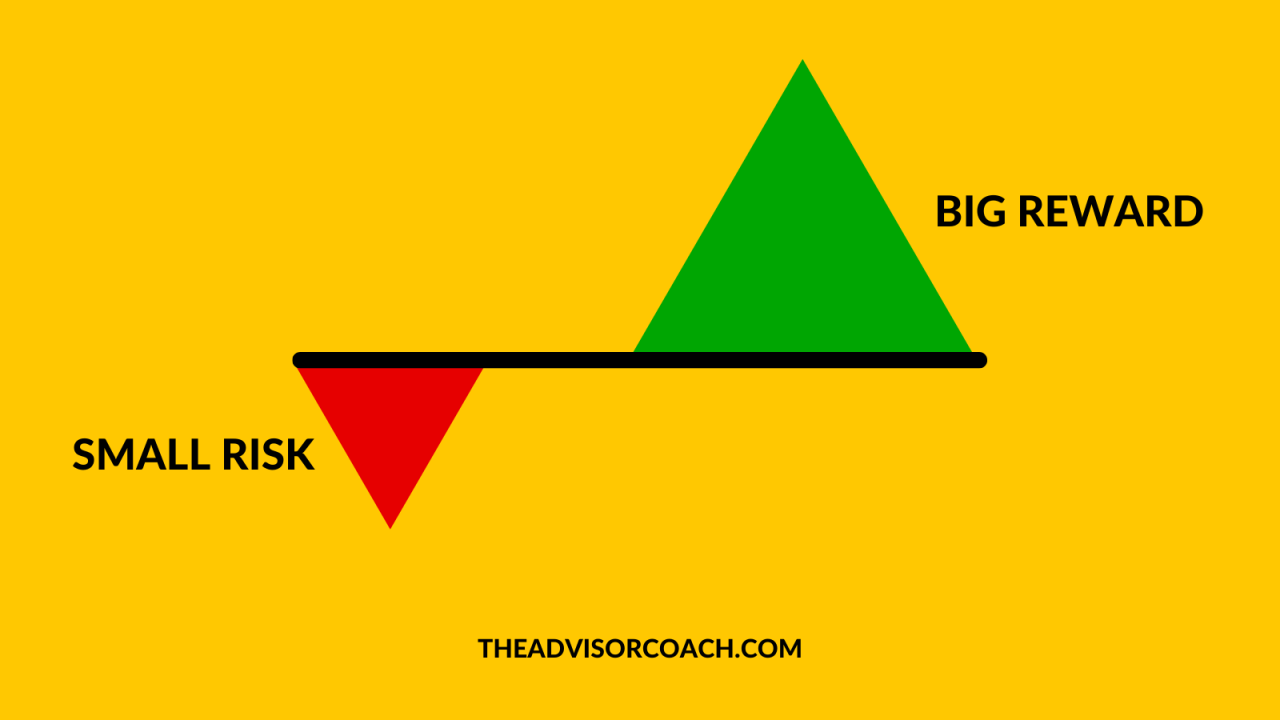

It’s taking advantage of asymmetric risks.

An asymmetric risk is a scenario where the potential for profit or loss is imbalanced. Put another way, the risk is not equal to the potential reward.

Playing Russian roulette is an example of an asymmetric risk you would NEVER want to take. However, there are many asymmetric risk opportunities you should seize when you have the chance…

For instance, imagine you and I are sitting together at my desk and I tell you I’d like to play a coin flipping game that goes like this…

You risk $5 and I flip a coin. If it’s heads, I keep your $5. But if it’s tails, I pay you $50.

How many times would you like to play that game?

I hope as much as you possibly could! Because, over the long term, the potential for profit is so much higher than the potential for loss.

Yet, the sad truth is that many financial advisors are playing games where the odds aren’t in their favor. Here are three examples…

Example 1: Using unscalable marketing strategies.

If you’re a financial advisor and your net income is below $300Kish per year, it’s almost certainly because your marketing doesn’t scale well.

Two examples of unscalable marketing strategies are referrals and cold calls. I appreciate both of these strategies, but they should be viewed as icing on your business cake, not the cake itself. Because the cold hard truth is that if you try to compete with a scalable marketing strategy, you will get crushed.

Two examples of scalable marketing strategies are online advertising and email marketing. In fact, I put together a free 42-minute video titled “How Financial Advisors Can Run Profitable Online Ads”, which you can watch here:

How Financial Advisors Can Run Profitable Online Ads

I created it because I’m so sick of “lead-gen” companies selling financial advisors expensive, unqualified leads when all they’re doing is running ads and passing the traffic down the line. In the above video, I share examples of ads I’m running that get 20X more clicks than average at 1/10th the cost.

Email marketing is also incredible because you can create an autoresponder sequence which contacts your prospective clients on autopilot whether you’re working, sleeping, or on vacation.

I also wrote an article detailing a few things I’ve learned from sending 3.2 million financial advisor emails, which you can read here:

What I’ve Learned From Testing 3.2 Million Financial Advisor Emails

Email is the most powerful appointment-setting marketing strategy I’ve ever seen in my entire life. It’s incredible, and any financial advisors who don’t adopt it as a marketing strategy will be kicking themselves in a few years.

But enough about email. Let’s move on to the next example...

Example 2: Letting lifestyle creep sabotage them.

Lifestyle creep happens when increased income leads to more spending. You make more money, so you buy nicer clothes…

Drive a luxury car…

And live in a bigger house.

While those things are cool, they can wreck your chances of hitting asymmetric jackpots.

The guy who makes $50K per month and spends all of it literally has no room to try new things and cannot remove emotion from the investments in his business. He is a slave to making that $50K per month and can’t try new things to get him to the next level. He can’t afford the temporary drop in income.

On the other hand, the guy who makes $20K per month and only lives on $5K per month can literally do $15K worth of tests and experiments…

Every…

Single…

Month.

For him, it’s pure math. No emotion and no neediness whatsoever.

Here’s the million-dollar question:

Who do you think is going to win in the great game of business? The guy who is hustling every month just to pay his bloated lifestyle expenses… or the guy running his business like a cool, collected blackjack player executing perfect strategy?

Most people aren’t willing to sacrifice today to increase their odds of success in the future. They’re chained to the hedonic treadmill, constantly trying to fill a void that mere “things” will never satiate.

Example 3: Failing to invest in themselves.

This past weekend, I spent some time going through my business receipts and realized that I’ve spent a LOT of money on personal development in the past year. I’m not going to give an exact number because I’m not one to count money in public, but it’s more than most people make in a year. And if “normal” people saw how much it was, they would probably have a heart attack.

But to the dream chasers… the winners… the people ACTUALLY succeeding in life… they’re necessary expenses.

I can buy a $30 book that helps me make an extra thousand dollars in a weekend. I can buy a $3,000 course that shows me how to make an additional $10,000 per month. I can hire a freelancer for $30,000 to unlock an additional six figures in productivity within my business.

Investing in yourself is critical to your success because it allows you to shorten your learning curve. Put simply, you don’t have all the time in the world to figure things out. All else being equal, people who implement faster will be more successful.

I think a good rule of thumb is AT LEAST 5% of your annual income. Here’s what that looks like, based on various annual incomes…

$50,000 income = $2,500.

You can buy one book a week and still have money left over for an online course or two.

$100,000 income = $5,000.

You’ve got books and most courses covered. You can now add something like a conference or seminar.

$250,000 income = $12,500.

Here’s where you can put a rocket ship on your back. This is the level where you can outsource many of the day-to-day personal tasks that take up your time. This includes house cleaning, food prep/delivery, landscaping, car washing, and so on. You can take your saved time and invest it back into yourself and your business.

(Here are some productivity tools I recommend once you’re at this level.)

$500,000 income = $25,000.

You now have several options. You can focus exclusively on high-level courses and/or hire a coach/consultant or two.

$1,000,000 income = $50,000.

Now you’re getting dangerous. You can easily afford something like “40 Years of Zen”, which costs at least $15,000. It will help you access mental states that typically take 40 years of meditation to achieve.

At this level, you are paying for faster results.

You also have the money to message experts in your field and pay their hourly consulting rates to solve your biggest problem.

Past this income level, your personal growth budget will likely morph into a team of people who check in with you on a regular basis. You’re paying for access more than anything else.

My point is that you MUST think this way if you want to get to the next level.

That’s why I can’t help but laugh when I see financial advisors stumble, hesitate, and fret about subscribing to my Inner Circle newsletter.

It’s $99 per month. Aka less than $3.26 per day.

And guess what?

I don’t even keep the money for the first month. Because I donate every penny of the first month’s payment of $99 to a charity called First Book.

So, the potential “downside” is the possibility that you hate the newsletter and cancel your subscription before being billed again.

(Which, to the best of my knowledge, has never happened. EVER.)

The potential upside is that your business will be forever changed for the better.

Seems like an easy choice to me because it’s the perfect example of an asymmetric risk you should take.

Related: Here's What Millionaire Financial Advisors Do Differently