Trending

I-Bonds: At 7%, It’s Hard to Go Wrong

Does a risk-free bond with a seven percent yield interest you? If so, read more about the red-headed stepchild of the bond world that is finally attracting investors. Series I Bonds (I-bonds) are bonds issued directly to the public by the Department of Treasury. Unlike most other bonds, I-bonds pay a coupon that adjusts for inflation. Not surprisingly, with inflation surpassing 8%, we receive quite a few questions on I-bonds. As such, this article provides more information on I-bonds to help you compare them versus TIPS and other types of bonds.

How Can I get a 10% bond?

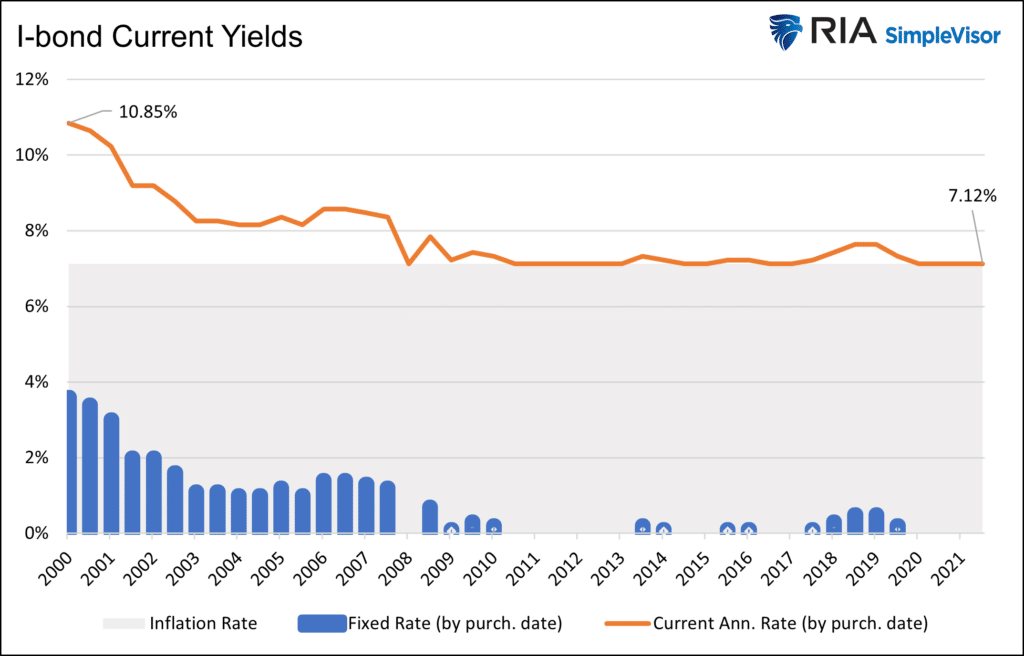

I-bonds currently have a yield ranging from 7.12% to 10.85%, depending on when the bond was bought. The graph below shows the current annualized yield (orange) based on the purchase date on the x-axis.

The coupon of an I-bond equals the sum of its fixed-rate (blue) and the current inflation rate (gray shading).

The fixed-rate, set by the Treasury and shown in blue, is loosely linked to Fed Funds and money market interest rates. As the name states, the fixed-rate remains constant throughout the bond’s life. The current fixed rate is zero, but it has been as high as 3.60%.

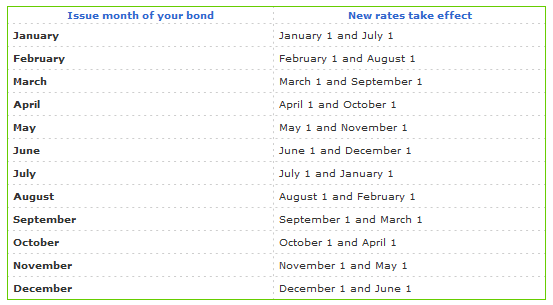

The inflation rate is equal to CPI and resets every six months. Inflation rates reset in May and November, but the coupon of I-bonds changes at varying times depending on the purchase month.

I-bonds compound the coupon payments into their principal values, whereas most bonds pay holders a semi-annual coupon payment. For example, if you purchase $1,000 of an I-bond with a 5% coupon, the bond’s principal value will increase to $1,050 at the end of year one. Assuming the coupon remains 5% in the second year, the holder receives 5% on the new principal value ($1,050), not the original value of $1,000 like most bonds.

To appreciate compounding, consider the benefits of holding an I-bond for ten years that pays 5% every year. In year 11, the principal value will be worth $1,628. The interest payment in year 11 would be $81.45, not $50 (5% of $1,628). Despite the 5% coupon rate, the bond pays an 8.1% yield on the $1,000 original investment. In our example, you can redeem the bond at year 11 for $1,628.

How Do I Buy an I-Bond?

I-bonds can only be purchased directly from the U.S. Treasury or through the IRS by applying a tax refund toward an I-bond purchase. There are limitations to the amount of bonds you can buy in either case.

The maximum amount of an I-bond an individual can purchase is $10,000 per year. You can buy I-bonds in $25 increments directly from the Treasury Department via TreasuryDirect. If you wish to use a tax refund, you must include a completed IRS form 8888 with your tax forms. There is an annual purchase limit of $5,000 per year using tax refunds, and you must take delivery of the bond as a physical “paper” bond. If you buy from TreasuryDirect, you can elect to have bonds in electronic form and avoid the risk of holding a physical bond. One can buy up to $15,000 per year using both purchase methods.

I-bonds have a 30-year maturity but can be redeemed anytime after the first year. There is a penalty of the last three months of interest if you redeem the bond before the fifth year.

Like other Treasury bonds, I-bonds are Federally taxable but not taxable on a state level.

TIPS

Treasury Inflation-Protected Securities (TIPS) also offer investors inflation protection but are much easier to buy and sell than I-bonds. There are no limitations on the amount of TIPS you can purchase or restrictions to sell them. TIPS holders are not subject to early redemption fees. Like I-bonds, you can buy TIPS from the Treasury Department via TreasuryDirect. Unlike I-bonds, almost all stock and bond brokers sell them. Further, some mutual funds and ETFs solely hold TIPS portfolios.

I-Bonds vs. TIPS Returns

From a liquidity perspective, TIPS are the better option. However, from a returns perspective, there are differences worth considering. Like I-bonds, TIPS have a fixed rate and an inflation rate. TIPS bonds pay bondholders the fixed coupon rate every six months based on the principal value. This feature may be advantageous for those needing income versus an I-bond where the coupon accrues. The compounding benefits of I-bonds may be more attractive for those focused on saving.

More critical to the decision between the two is how the bonds capture inflation.

As discussed, I-bonds accrue the coupon (sum of the fixed and inflation rate) into the bond’s principal value. Deflation can offset the fixed rate in any given year, but the principal value will never decline.

The coupon on a TIPS is paid to the holder, but the inflation rate accrues as principal value. There are some compounding benefits, albeit not as much as an I-bond.

More importantly, however, deflation can reduce the principal amount of TIPS to its original principal value.

When the deflation rate is more than the fixed-rate an I-bond will yield 0%. That is the worst-case scenario. The effective yield on TIPS can be negative. While TIPS holders will still receive a coupon, the bond’s principal can erode more than the coupon and decline back to its original principal value.

There are tax differences also worth considering. Interest payments and inflation adjustments on TIPS are taxable each year. I-bond interest can be deferred until it is sold or matures.

Monetary and Fiscal Policy Make I-bonds Attractive

With an understanding of I-bonds, let’s now answer whether it makes sense to buy one today.

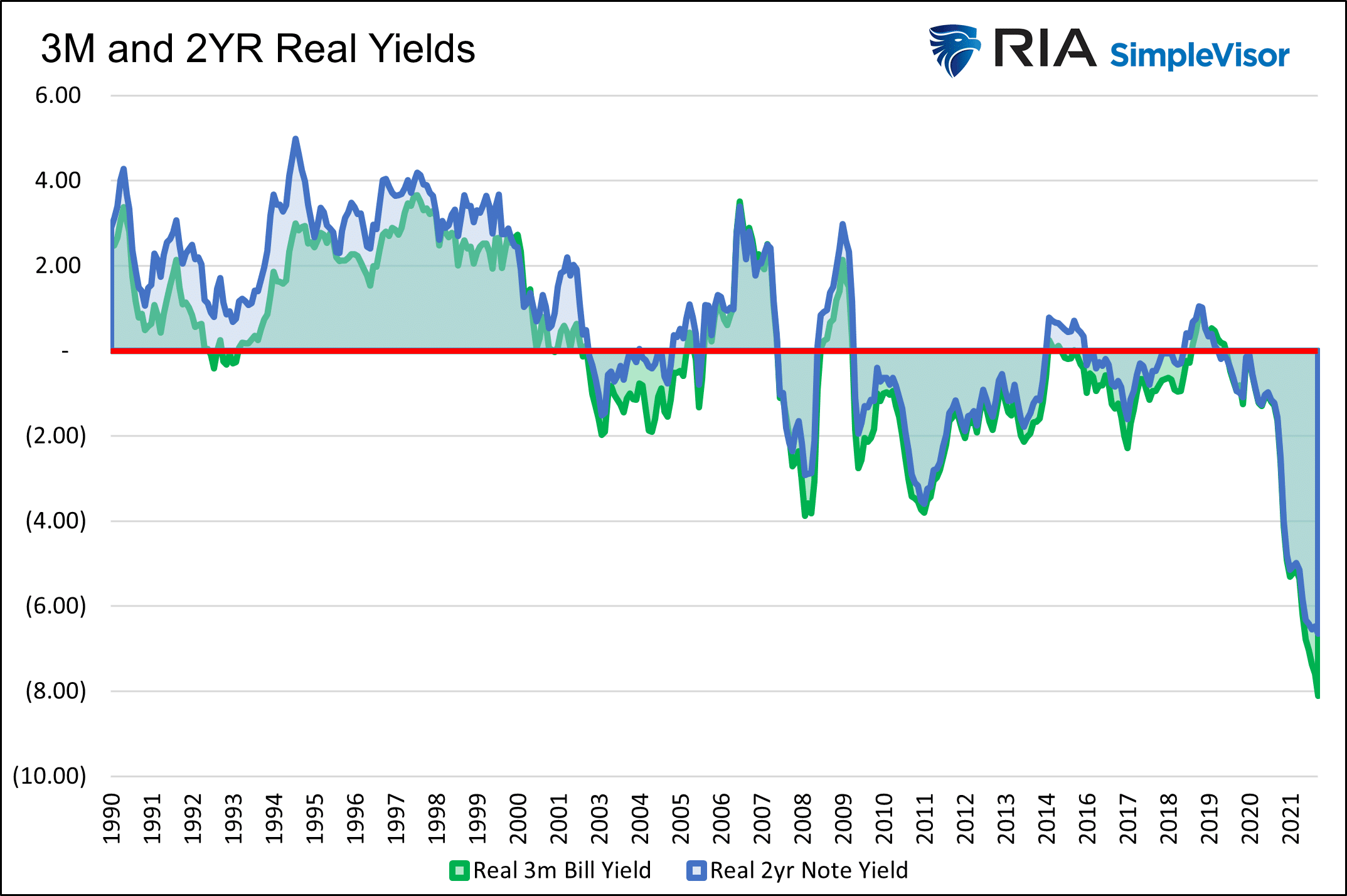

Regardless of inflation in the future, I-bonds should be a much better alternative to money markets or short maturity bonds. The state of indebtedness in the U.S. requires the Fed’s efforts to support it with negative real yields (inflation-adjusted). We do not see that changing.

As we show below, the real yield on three-month and two-year Treasury bills and notes has been negative for most of the last decade. The real yield on an I-bond in the worst-case scenario is zero. A zero real yield may not be appealing, but it sure beats a negative real yield.

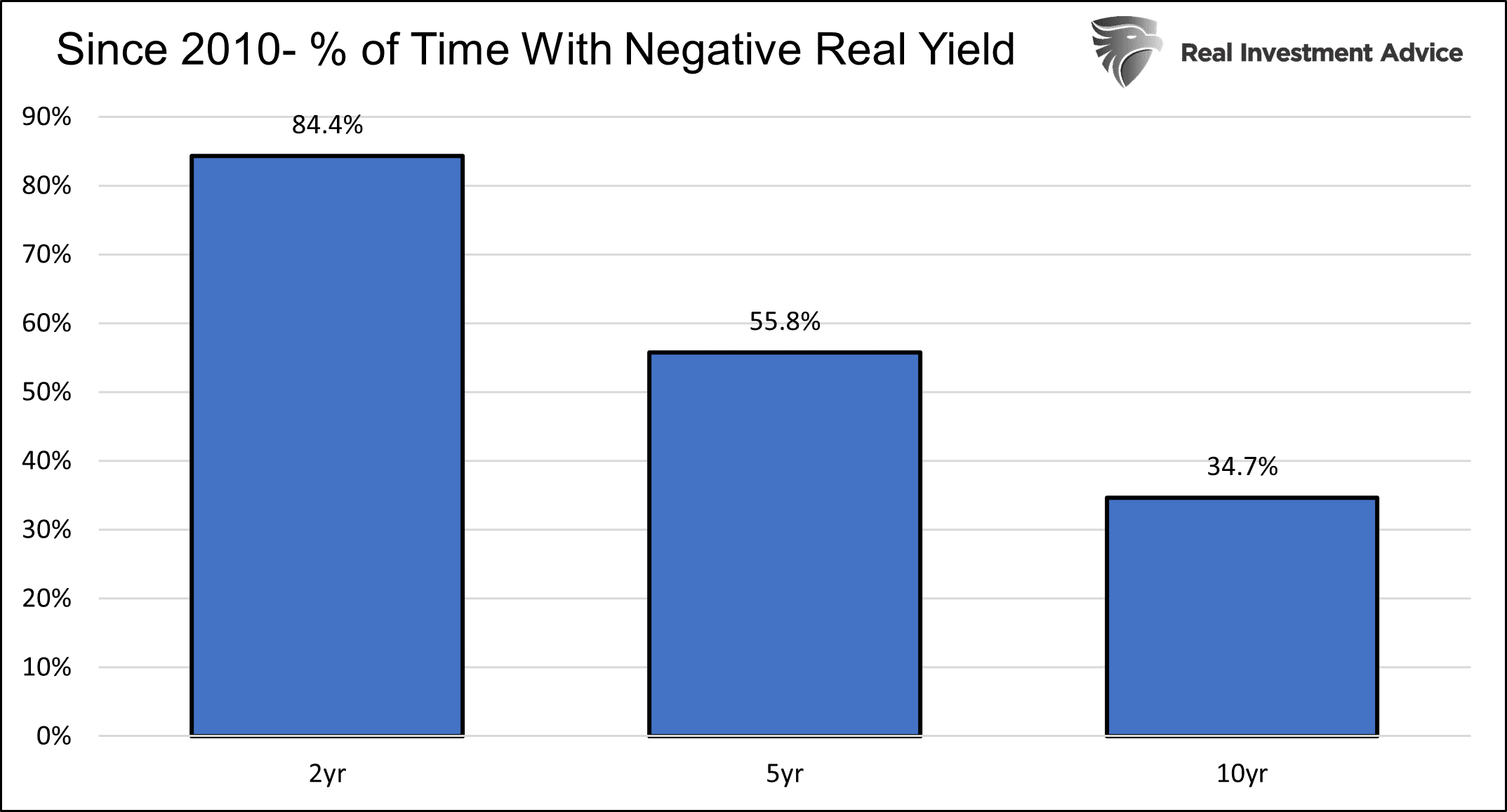

We share the graph below to compare I-bonds versus longer-term Treasury bonds. The graph highlights the percentage of months since 2010 in which the real yield on 2yr, 5yr, and 10yr notes was negative. Again, a zero real yield may be a relatively decent alternative.

Should I Buy an I-bond?

The decision to buy an I-bond today presents a unique opportunity. An investor can capture a high annualized yield of 7.12% for the next six months. After that, the yield will float with CPI. If we assume inflation falls to five percent at the next reset, the I-bond will yield 6.06% in its first 12-month period. That dwarfs the yields on all money market equivalent bonds.

While it seems like a no-brainer there is a catch. You must give up the last three months of interest to redeem an I-bond after the first year and before the sixth year.

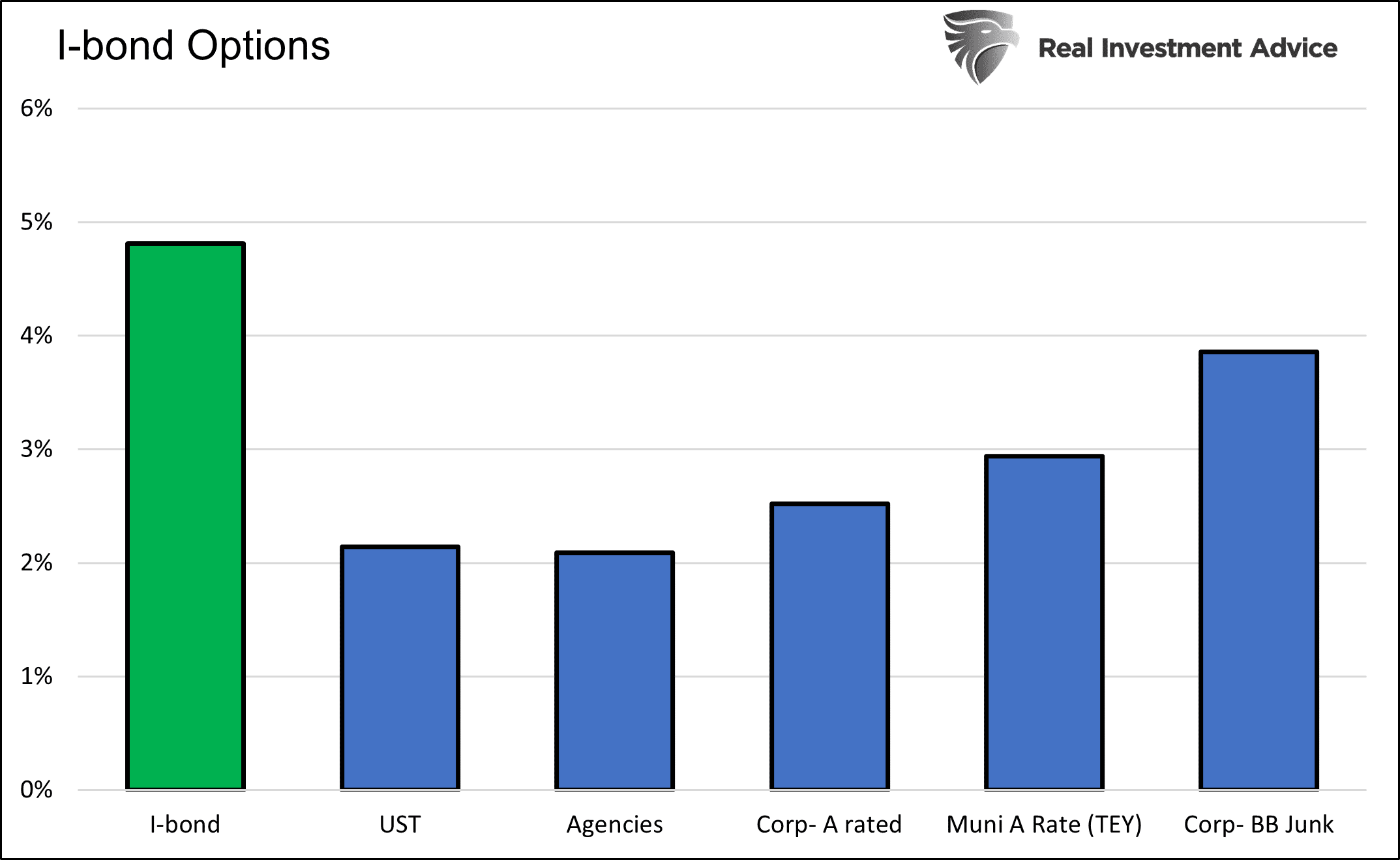

The graph below compares the yield of an I-bond to other one-year bond options. The annual yield on the I-bond assumes 5% CPI in the second six-month period and an early redemption penalty of three months of interest.

The data for the comparable bond yields is from Charles Schwab. The corporate junk-rated option represents the highest yielding BB-rated. The Municipal bond yield is a tax-equivalent yield (TEY).

CPI has to fall below 3% in the following six months to make an investor indifferent between a 1-year junk bond and the I-bond. Keep in mind the I-bond is risk-free while the junk bond is far from it. Even at 0 percent inflation in the second six-month period, a buyer is indifferent between buying a one-year Treasury bill and an I-bond today.

The I-bond is a superior choice in almost all cases. However, the size limitation makes it difficult for many investors to accumulate enough I-bonds to move the needle. For smaller accounts focused on wealth preservation, I-bonds make a lot of sense.

Summary

I-bonds guarantee a zero percent real yield. That may seem paltry, but given the fiscal and monetary policy landscapes, that may prove better than many fixed-income alternatives.

I-bonds are flawed in that they have an early redemption fee, cannot be redeemed in the first year, and can only be bought in small increments. If inflation is a concern, we think a combination of I-bonds and TIPS will hold up better than most other bonds on a real, inflation-adjusted basis.

For more information, visit the TreasuryDirect website.

Related: Inflation and the Fed. A New Dance Partner to Contend With