Trending

I see a lot of people talking about 2023 as the year we see the FinTech markets separate the wheat from the chaff. No wonder when you look at the stats that show it’s the end of the boom party.

As reported by Hugh Son at CNBC:

Many fintech companies — particularly those dealing directly with retail borrowers — will be forced to shut down or sell themselves next year as startups run out of funding, according to investors, founders and investment bankers. Others will accept funding at steep valuation haircuts or onerous terms, which extends the runway but comes with its own risks. Top-tier startups that have three to four years of funding can ride out the storm. Other private companies with a reasonable path to profitability will typically get funding from existing investors. The rest will begin to run out of money in 2023.

This is clear when you look at the stats. After a decade of growth and record fundraising in FinTech, FinTech companies accounted for 21 of the UK’s 44 unicorns, but data from investment manager Finch Capital showed funding reached $6 billion in 2020 and $19 billion in 2021, then took a 25% drop in 2022. The number of new FinTech firms founded is down 85% since 2020. Market consolidation continues, and FinTech M&A spiked in the first half of 2022, with 591 recorded deals. So, it is possible that we are now on the other side of the FinTech sector ‘boom.’

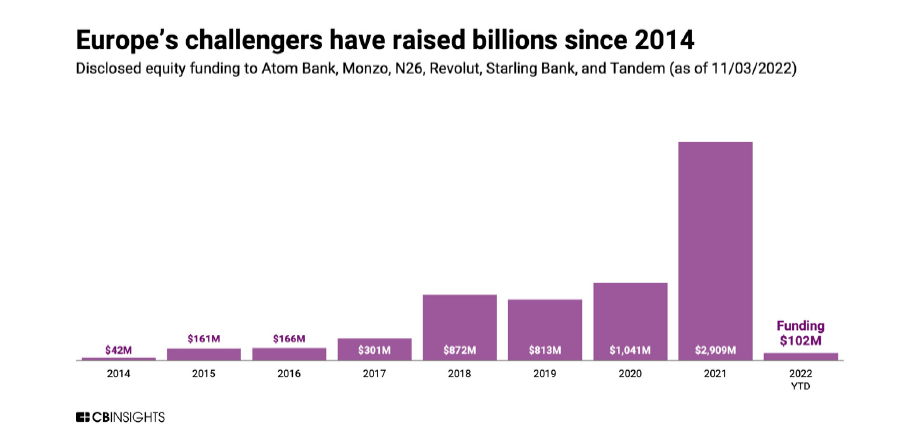

In fact, this is well illustrated by a couple of charts from Tearsheet that shows challenger banks in Europe raised over $6 billion of funding since 2014 but, last year, things took a bad turn with challengers only raising $102 million (as of November 3rd 2022), their lowest since 2014.

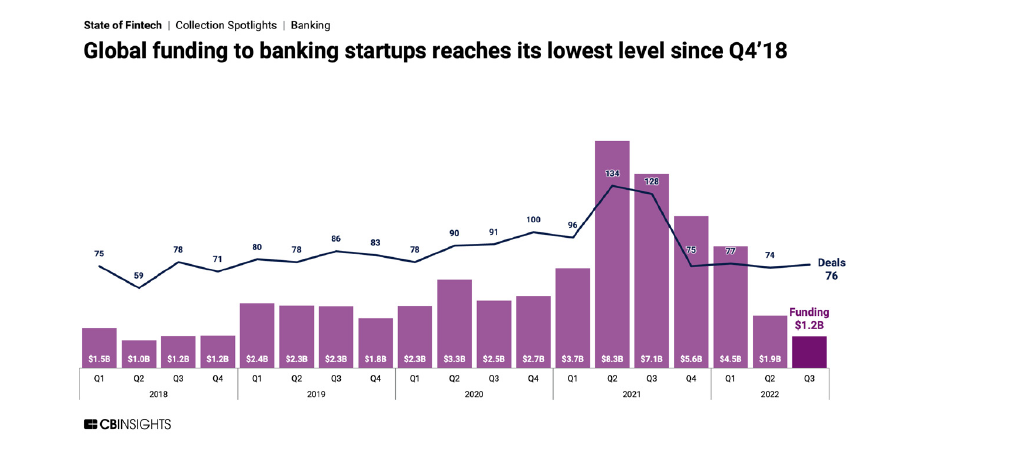

During 2022, all startups saw a hit in funding with global venture funding decreasing by 34% QoQ in Q3’22. And fintechs may have experienced the biggest slap of them all: in Q3 of 2022, fintechs accounted for 17% of all tech funding – down from 25% in Q2 2021.

This means that start-ups, and particularly FinTech startups, need a lot more focus on viability and stability. Most people are predicting that business models will be challenged with investors looking for ROI; embedded finance will be the biggest growth area, along with AI used intelligently; B2B FinTechs will succeed far more than those focused on B2C; smart contracts and blockchain is still a thing; whilst the new area will be the development of super-apps, like Alibaba and Tencent, outside of China.

Interesting.

There are a few specific things that different contacts touched upon, and so I thought I would share some of those. For example, Jorgen Christian-Juul, CEO and founder of Cardlay, sent me a bunch of five FinTech trends for 2023 therefore, as a result of this slowdown.

Increased focus on digitalisation and cost optimisation: international external factors such as the war in Ukraine, and the energy crisis, will lead FinTech’s to focus their attention on cost optimisation and digitalisation as they continue to manage their business during these times.

Partnerships to scale and digitise product positioning with a fast go-to-market plan: the FinTech industry will see an industry-wide push for a speedy go-to-market plan with the competition at a high. As well as this, companies hoping to get ahead will realise there is strength in numbers, and seek partnerships with complimentary financial services companies to offer a robust package. In 2022 we partnered with SAP Concur to offer a payment cloud solution that integrates issuers, processors and technology providers to enable end-to-end virtual card creation and reconciliation.

Virtual cards will be used in all forms of payments: the ease of use for consumers and simplicity to set up for businesses has led to a huge rise in the use of digital wallets. According to IT service management company Marqeta, 75% of consumers are now embracing digital wallets to pay for their purchases, with 60% of people saying that they’d now feel comfortable leaving the house with just their phone and not their wallet. Virtual card payments are set to become the norm in 2023.

Consolidation of the FinTech market: research conducted by FinTech Capital has revealed that FinTech investment had slowed over 2022. According to the report, business formation in the FinTech sector peaked in 2018, and over the last year, has declined by 80%. This could result in consolidation in the industry, which will ultimately strengthen the offering of larger FinTech operations.

Increased focus on banks who are in demand for partnerships to service increasingly demanding portfolios: as the financial sector has evolved, traditional banks no longer have the resources to keep up with modern banking demands. An influx of banks seeking FinTech partnerships is set for the forthcoming years. If traditional banks fail to keep up with the innovation of FinTech’s they are bound to fall behind.

Anuj Nayar, LendingClub’s Financial Health Officer, states that 2023 is the year “to separate the strong performers from the ones that are struggling”. And many are struggling as investment markets dried up in 2022. According to Anuj, this leads to three big trends in the US FinTech markets:

Looking to get a bank charter: the markers of FinTechs who are successfully navigating this wavering economy are those in the digital banking space, including those that are combining their lending capabilities with a bank charter, the lack of which appears to be adversely impacting resiliency.

FinTech M&A: FinTech M&A increased in 2022 with the likes of TD Bank/First Horizon deals. As the cost of funds continues to increase, this trend could accelerate dramatically. There are still well-capitalised buyers out there who will look to accelerate out of a potential downturn through acquisitions and consolidations.

Regulation: the US regulator CFPB recently proposed a new rule under Section 1033 of the Dodd-Frank Act on open banking and consumer data rights, which will empower consumers to “break up” with banks that provide bad service by providing consumers greater access to their financial records”. If it is enacted, it could help end the trend of consumers paying too much for credit and earning too little from their bank accounts. It could also help consumers more easily switch to FinTechs and banks that offer lower rates on loans and pay higher interest and rewards on checking and savings accounts.

Unsurprisingly, as a CEO and Co-Founder of compliance technology and data analytics firm SteelEye, Matt Smith, agrees and believes the trends are all around tightening of markets. By way of example, in the United States, the SEC filed 760 enforcement actions in 2022, up 9% from 2021. This amounts to an eye-watering $6.4 billion – an all-time record – far surpassing 2021’s $3.9 billion in fines. His 2023 predictions include:

Voice Compliance: regulators will eventually embed voice in surveillance and archiving requirements. To get ahead, many US firms are proactively self-regulating and investing in voice supervision and transcription to improve their surveillance.

Crypto Regulation: the recent FTX collapse highlighted, once again, how volatile the space is. It is a fragile market and represents a considerable systemic risk, where the fall of one significantly impacts the whole market. In 2023 there will be a “regulatory reckoning”, to build a world where regulation is sufficiently sophisticated to protect retail investors and make crypto a more stable investment for financial institutions.

My friends in Central & Eastern Europe (CEE) – specifically Austria, Estonia, Greece, Hungary, and Romania – came up with these ten key trends:

#1 Embedded Finance: many professionals are talking about it as the next financial frontier and also why financial players build these types of products with no code/low code.

#2 FinTech trends for SMEs: embedded financial services will lead to more and more FinTech solutions for small and medium companies. For example, Bulgarian Payhawk became a unicorn by focusing upon this space from the start.

#3 Alternative payment infrastructure: say “bye-bye, baby” to credit cards or bank transfers with the rise of alternative or personalized payment systems, as Romanian PAGO offers. These represent convenience, speed, and security compared to financial traditional methods. Account-to-account (A2A) transactions could represent 15% of transactions by 2030, for example.

#4 Functional business models: investors will be looking for more robust business models in 2023, and will “scrutinize the ratio of the cost of user acquisition to customer lifetime value, especially the assumptions behind the value part and how fast that value can be achieved.”

#5 Central Bank Digital Currencies (CBDC): will be a big focus “as governments realise that they should not miss the blockchain party.”

#6 Know Your Customer (KYC) guidelines: will see major growth next year. Some regulations that will emerge in 2023 will likely involve biometry, and crypto, to name a few.

#7 Micro-FinTech: 2023 will be the year of micro-investments and, “in the world of insurance, pay-per-use insurances (only pay for the car insurance when you are driving the car), as well as micro-insurance (in some cases embedded insurance) which aim to cover risks in a limited time could be an interesting way to disrupt the traditional market.”

#8 ESG is a key topic in finance too: “2023 seems like a year when the pressure to think and act sustainably will begin to materialise in actual products and services.”

#9 Personalised tools: “although generalist finance applications will always take part of the market, I expect custom-designed solutions that cater to specific audiences’ needs to be much more effective moving forward.” This means the development of voice recognition technology and natural language processing (NLP) so users can access services through voice commands for seamless processes. “Siri? Alexa? Pay my internet bill and donate to The Recursive” coming next.

#10 AI Technology as a cost-effective alternative

Last, but not least, “algorithmic AI decision-making is an efficient alternative to the current high costs of aggregating, analysing, and using data. Moreover, chatbots are also quickly becoming an invaluable asset for customer support departments.”

Not to overlook other parts of the world, here are the top 5 FinTech trends & predictions for Africa:

The Unbanked: given that a large portion of African people are still unbanked, there is a large market to tap into, and many FinTechs and banks are trying to solve this problem and tap into this market. FinTechs in Africa will continue to provide solutions to the continent to create seamless, borderless transactions. Furthermore, many banks will continue to partner with new FinTechs to solve this problem, as well as many others.

Highest funding ever: according to data from The Big Deal, African startups raised over $4 billion in the third quarter of 2022 alone, the fastest the continent has seen in the past three years since they surpassed $1 billion in funding. The funding is also impressive because it comes in a period when over 100 startups in Africa have raised their first $1 million+ round this year. FinTech is proving to be the main driver of investment on the continent, and experts predict 2023 to be an even better year.

Mobile Network Operators (MNOs) will become more active: MNOs are key to watch in the space. The banking sphere is competitive, and should the MNOs be granted a mobile money license; competition will become even tighter. There has been a vast amount of research indicating that West Africa will be focusing on growth within mobile and online banking instead of traditional banking institutes as this is of lower cost to the average consumer. With the steady growth of smartphone users, Africa will experience growth in more accessible financial solutions.

Crypto adoption will rise further: the crypto scene has been incredibly turbulent in recent times. However, with the rise of FinTechs and the growth of companies such as Luno, more mainstream usage and adoption of cryptocurrencies is expected. We predict a huge growth in crypto adoption in Africa in 2023, and leading cryptocurrency exchanges are making efforts to support this trend.

Emerging technologies: as technology improves exponentially, an array of new innovative solutions will arise. We expect to see new, exciting changes in the FinTech sphere through IoT technology, Artificial intelligence, Big Data, and numerous other types of emerging technology and trends.

Meantime if you’re looking at where to focus, especially career-wise, FinTech Futures points to three key areas:

Cloud and cybersecurity

The growing threat of security breaches means FinTech companies are increasingly contingent on protecting digital data and creating the software required to protect financial institutions. Despite this growth in the cybersecurity sector, 43% of organisations globally are struggling to find top talent, meaning an even greater reliance on automation and managed security tools.

AI and machine learning

FinTech is increasingly relying on AI and machine learning to provide innovative solutions. One area in particular where AI has proved invaluable is regtech within the financial industry. AI technology can help with compliance costs, credit risk assessment and fraud detection. AI-powered personalisation is also another area that looks set to surge in 2023 and beyond as financial institutions turn to AI to help customers over automated chatbots or hard-to-reach customer helplines.

Blockchain

Experts predict that 2023 will see blockchain technology reach its technological tipping point and become one of the fastest growing sectors over the next decade to the tune of £5 trillion globally. While cryptocurrency has dominated the sector up to this point, the growing need for blockchain technology to power Web3 will bolster this new era of decentralised finance even further.

All in all, 2022 may have been the year of challenge but 2023 does look like a year of opportunity … as long as you are the wheat and not the chaff.

Related: Tech and Cybersec in 2023: A World That Is Virtually Different