Trending

Written by: Christopher Gannatti & Aneeka Gupta

Key Takeaways

- In August 2025, gold prices have surged past $3,300 while miners maintain median production costs near $1,600, creating historically wide margins that savvy investors can no longer ignore.

- Despite massive profitability, gold supply remains inelastic due to long project lead times and environmental constraints, reinforcing the case for disciplined miner exposure over pure bullion plays.

- With the WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN) up 76% year-to-date, outperforming both gold and traditional miners, investors now have a capital-efficient way to potentially capture gold’s margin upside with equity-like alpha and downside resilience.

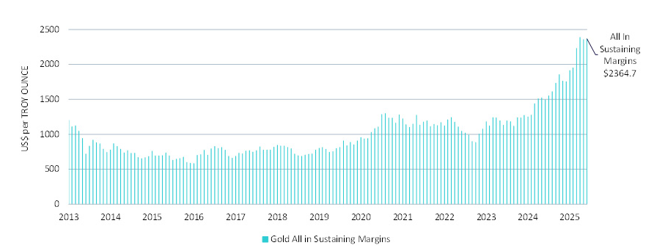

Looking at gold in August 2025, forget spot prices for a moment. We believe what matters most in gold mining isn't the number on the screen, it's the spread between what you're paid and what it costs to keep the machines running. In gold today, that spread is breathtaking. At over $3,300 per ounce and climbing, gold prices have surged to all-time highs.1 But here's the kicker: the median all-in sustaining cost (AISC) across gold miners2 barely scrapes past $1,600.3 That's roughly $1,700 of production margin4 per ounce—the kind of figure that should turn heads in any sector. It's not just a bull market in gold—it's a new reality in gold mining profitability.

Figure 1: The Golden Spread: Mining Margins Surge to Record Highs

Sources: Bloomberg, WisdomTree, as of 6/30/25. Please note: All-In Sustaining Margins represent the difference between gold price and the weighted average all-in sustaining costs (AISC) of the constituents of the NYSE Gold Miners index.

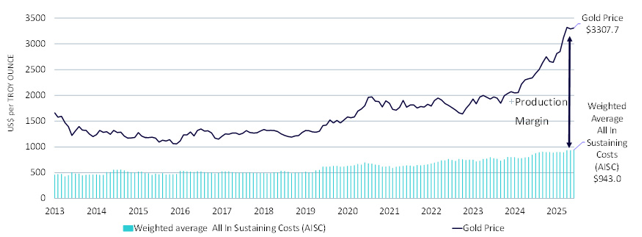

The Iron Law of Margins—and Why It's More Important than Price

Figure 2 makes it explicit: what powers decision-making inside mining companies isn't spot price in isolation—it's the durability and scale of margin.

Figure 2: Cost Contained, Price Unchained: Gold's Production Margin Hits All-Time High

Sources: Bloomberg, WisdomTree as of 6/30/25.

The 2011–2013 cycle burned that lesson into corporate memory. Back then, gold ran to $1,900, but miners chased growth with irrational exuberance—funding marginal projects at the top of the cost curve, and torching investor capital when the cycle turned. Today? Discipline reigns. New projects must clear a 15%–20% internal rate of return at a conservative long-term price deck. Boards are skeptical of spot prices.5 They assume gravity wins eventually.

Why Costs Are Rising—and Why That's Not a Bad Thing

There's nuance in the rising AISC trend. Yes, input inflation and environmental, social and governance (ESG) capital expenditures play a role—solar-battery hybrid power plants don't come cheap, nor does skilled labor in remote jurisdictions. But here's the subtlety: some of the rising cost is actually a byproduct of choice. When margins expand, miners lower their cut-off grades and process more low-grade ore—effectively "printing" more gold.6 This endogenous cost inflation is a feature, not a bug. It's how miners stretch throughput and maximize net present value (NPV), using today's margins to unlock marginal ounces they'd never touch in leaner times.

The Silent Constraint: Why Supply Won't Catch Up Anytime Soon

You'd think these record margins would trigger a flood of new supply. But the supply curve in gold mining is glacially inelastic. Projects take 7–10 years from discovery to first pour. And the pipeline is tapped out—exploration budgets were slashed post-2013, and high-grade deposits are increasingly rare. Layer in tougher permitting regimes, higher royalties and ESG constraints, and you get a simple truth: there is no fast track to new gold supply, no matter how juicy the economics look today.7 This is a structural bottleneck, not a cyclical hiccup.

Figure 3: Once Burned, Twice Cautious: How Gold Miners Rebuilt Their Capex Playbook

Sources: Bloomberg, WisdomTree, as of 6/30/25.

The Setup: Durable Margins, Disciplined Management and a Repricing of Risk

What's unfolding is the kind of margin regime shift that quietly rewrites investor expectations. Many gold miners are now gushing free cash flow with balance sheet leverage under 0.3 times EBITDA8—offering oil-major-style dividend frameworks, but with lower capex intensity and less political heat. That kind of profile deserves a re-rate. Investors don't need a higher gold price to get paid. They just need margins to persist. And here's the asymmetric part of the story: even if gold drops $400, margins remain historically fat.9 That's a setup few sectors can match—and one that feels deeply underappreciated right now.

What about the Case for Gold in Summer 2025?

In summer 2025, the macro case for gold remains as compelling as ever—not because it hasn't moved, but because its move reflects a deeper re-rating of global financial conditions. Crossing $3,300 doesn't mean gold has "run too far"—it means investors are recalibrating what's worth trusting. Real rates remain subdued, and while the U.S. debt burden is drawing more scrutiny, it's less about hitting a breaking point and more about signaling a shift in how markets and policy makers frame long-term risk. Central banks, especially in emerging markets, have been quietly but persistently reshaping their reserve strategies—accumulating gold as a non-sovereign asset that sidesteps the geopolitics of Treasuries.10 Add in simmering global tensions and rising skepticism toward fiat durability, and gold's ascent starts to look less like a spike and more like the early stages of a structural repricing. The price has moved—but the world around it may have moved even more.

Building the Investment Strategy

What is the optimal way to express that exposure? Is it physical, futures-based, miner equities, royalty and streaming models, or something more novel—like tokenized gold or gold-integrated multi-asset strategies? In 2025, gold is back in the portfolio construction conversation. But the debate is shifting from "why gold" to "which gold—and how."

So, let's consider some of the more popular choices:

-

Do they take direct exposure to the metal itself, through vehicles like SPDR Gold Shares (GLD),11 and position for stability and monetary debasement hedges?

-

Or do they reach for equity-like upside via the shares of gold miners in the VanEck Gold Miners ETF (GDX),12 which historically offer leveraged sensitivity to movements in the gold price—but come with operational risk and higher volatility?

Or, there is a third option that has entered the arena—capital-efficient exposures that combine gold and gold miners into a single vehicle, such as the WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN).13 These aim to deliver both the stability of the metal and the growth potential of the miners, while preserving portfolio capital to be deployed elsewhere.

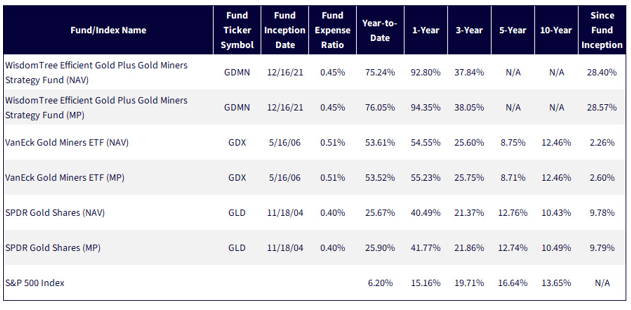

Figure 4: Standardized Performance

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 7/30/25, but showing returns for the period ended 6/30/25. NAV denotes total return performance at net asset value. MP denotes market price performance. The performance data quoted represents past performance and is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: GDMN, GDX, GLD.

-

2025 has been a breakout year for gold miners—but not all miners are equal. GDMN has surged 76% year-to-date, handily outperforming both traditional miners (GDX +55%) and bullion itself (GLD +26%). This isn't just beta—it's margin-aware, disciplined alpha.

-

Outperformance is persistent, not episodic. Over the one-year and three-year horizons, GDMN has outstripped its peers by 20–35 percentage points. Importantly, it's done so while the S&P 500 has lagged dramatically in 2025, underscoring GDMN's role as a differentiated return source—not merely a defensive hedge.

-

Longer-run results show structural leadership. Even over the longest common period, GDMN leads with a 27.9% total return, versus 19.3% for GDX and low double digits for GLD and the S&P 500. This suggests an evolving regime where quality-focused miners, strong margin capture and capital discipline are beginning to get re-rated—perhaps durably.

Figure 5: Miners Outshine Gold—and Nearly Everything Else

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 7/30/25, but showing returns for the period ended 7/28/25. NAV denotes total return performance at net asset value. MP denotes market price performance. Since GDMN Inception starts with December 16, 2021. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: GDMN, GDX, GLD.

Gold sets the tone, but miners amplify the story—on both sides. When GLD posts a positive year, GDX historically surges higher, averaging 24.8% returns versus GLD's 16.9%. But the reverse is just as true: in GLD-negative years, GDX has averaged a punishing −12.9%, making it a high-volatility expression of gold sentiment.

- 2025 YTD is the pattern on steroids. With GLD up 26.3%, GDX has gained 55.4%—but GDMN, the quality-focused miner Fund, has exploded higher by 76.0%. This isn't just leverage to the metal—it's margin expansion and capital discipline working in tandem.

- Direction matters more than magnitude. The calendar-year table shows that the binary—whether gold is up or down—is a better predictor of miner performance than how much gold moves. GDX tends to trade on trend conviction, not price precision.

Figure 6a: Cycles within the Cycle: How Gold's Direction Has Shaped Miner Returns

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 7/30/25, but showing returns for the period ended 7/28/25 for the 2025 YTD period. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: GDMN, GDX, GLD.

Figure 6b: Gold Has Set the Direction—Miners Have Set the Pace

Sources: Morningstar, FactSet and WisdomTree, specifically data is from the PATH Fund Comparison Tool, accessed as of 7/30/25, but showing returns for the period ended 12/31/24, the most recent full year. NAV denotes total return performance at net asset value. MP denotes market price performance. Past performance is not indicative of future results. Investment return and principal value of an investment will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For the most recent month-end and standardized performance, click the relevant ticker: GDMN, GDX, GLD.

Conclusion: The Margin Regime Has Changed—So Should the Allocation

Gold is no longer just a metal; it's a margin machine. And gold miners are no longer just a leveraged play—they are increasingly capital-disciplined operators that have learned from past cycles. The structural spread between gold prices and AISC has created a margin profile few sectors can replicate, with free cash flow surging and balance sheets healthier than ever. This isn't about chasing price—it's about capturing durable economic rent in a capital-light, cash-rich framework that's finally being recognized by the market.

Against that backdrop, investors are being presented with a timely and underappreciated opportunity: to rethink how gold exposure fits into the broader portfolio. Traditional bullion positions may hedge macro instability, but they don't harness the upside of expanding margins. Miners, selectively deployed, can. And strategies that integrate both exposures while maintaining capital efficiency—blending defensive ballast with cyclical torque—are now proving their worth in real-time performance. In this margin-driven regime, the allocation conversation shifts from "Do I own gold?" to "Am I capturing the full stack of what gold can deliver?"

Figure 7: Additional Information

Sources: WisdomTree, VanEck and SPDR. Assets under management as of 7/29/25.

Related: Fed Watch: See You in September?

1 Source: "Gold Spot Price Climbs to Record $3,303/oz amid Inflation and Geopolitical Concerns," Bloomberg, 7/29/25.

2 Gold miners in this article refers to the NYSE Arca Gold Miners Index universe.

3 Source: "Gold Focus 2025: Supply, Demand and Investment Trends," Metals Focus Ltd., May 2025.

4 Refers to the difference in gold's spot price and the all-in sustaining cost.

5 Sources: "Responsible Gold Mining Principles: Investor Guidance," World Gold Council, 2023; S&P Global Market Intelligence, "Gold Project Economics: IRR Thresholds and Development Risk," S&P Global, September 2024.

6 Source: T. Torries & D. Humphreys, "Strategic Mine Planning and Margin Optimization in the Gold Sector," Society for Mining, Metallurgy & Exploration, 2023.

7 Source: R. Schodde, "The Long Road to Gold: Discovery to First Pour Timelines and Supply Constraints," MinEx Consulting, September 2023. Presented at the Denver Gold Forum.

8 Refers to earnings before interest, taxes, depreciation and amortization.

9 Source: "Gold Miner Margins: Cost Discipline and Resilience in Volatile Markets," World Gold Council, November 2024.

10 Source: "Gold Demand Trends Q4 2024: Central Bank Gold Buying Remains Resilient," World Gold Council, December 2024.

11 The investment objective of SPDR® Gold Trust (the "Trust") is for SPDR® Gold Shares ("GLD") to reflect the performance of the price of gold bullion, less the Trust's expenses. It is the largest fund ranked by assets under management that provides exposure to movements in the price of physical gold.

12 VanEck Gold Miners ETF (GDX®) seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the NYSE Arca Gold Miners Index (GDMNTR), which is intended to track the overall performance of companies involved in the gold mining industry. It is the largest fund ranked by assets under management that provides exposure to movements in the share prices of a group of gold mining companies.

13 The WisdomTree Efficient Gold Plus Gold Miners Strategy Fund seeks total return by investing in gold miners and gold futures contracts. The exposure is designed such that for each $100, $90 is exposed to equities of gold miners, $90 is exposed to gold futures contracts and $10 is in U.S. Treasury collateral.

Important Risks Related to this Article

All funds are managed differently and do not react the same to economic or market events. The investment objectives, strategies, policies or restrictions of other funds may differ and more information can be found in their respective prospectuses. Therefore, we generally do not believe it is possible to make direct fund to fund comparisons in an effort to highlight the benefits of a fund versus another similarly managed fund.

Material must be proceeded or accompanied by a prospectus. Click the respective ticker to view the fund prospectus: GDMN, GLD, GDX.

GDMN: There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“gold miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of gold miners, the Fund may be susceptible to financial, economic, political or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic or regulatory conditions affecting that country or region, or emerging markets generally. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

GDX: An investment in the fund may be subject to risks which include, but are not limited to, risks related to investments in gold and silver mining companies, special risk considerations of investing in Australian and Canadian issuers, foreign securities, emerging market issuers, foreign currency, depositary receipts, small- and medium-capitalization companies, equity securities, market, operational, index tracking, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, fund shares trading, premium/discount risk and liquidity of fund shares, non-diversified and index-related concentration risks, all of which may adversely affect the fund. Emerging market issuers and foreign securities may be subject to securities markets, political and economic, investment and repatriation restrictions, different rules and regulations, less publicly available financial information, foreign currency and exchange rates, operational and settlement, and corporate and securities laws risks. Small- and medium-capitalization companies may be subject to elevated risks.

GLD: Investing involves risk, and you could lose money on an investment in GLD.

ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns.

Commodities and commodity-index linked securities may be affected by changes in overall market movements, changes in interest rates and other factors such as weather, disease, embargoes, or political and regulatory developments, as well as the trading activity of speculators and arbitrageurs in the underlying commodities.

Frequent trading of ETFs could significantly increase commissions and other costs such that they may offset any savings from low fees or costs.

Diversification does not ensure a profit or guarantee against loss.

GLD has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents GLD has filed with the SEC for more complete information about GLD and this offering. Please see the GLD prospectus for a detailed discussion of the risks of investing in GLD shares. You may get these documents for free by visiting EDGAR on the SEC website at sec.gov or by visiting spdrgoldshares.com. Alternatively, GLD or any authorized participant will arrange to send you the prospectus if you request it by calling 866.320.4053.

The Marketing Agent for GLD, State Street Global Advisors Funds Distributors, LLC, is not affiliated with Foreside Fund Services, LLC, or WisdomTree, Inc.

Past performance is not indicative of future results.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S.

This WisdomTree article is provided as part of a paid sponsorship.