Trending

Written by: Jeremy Schwartz

Key Takeaways

-

Most investors are significantly underweight gold, holding just 0–3% compared to a market-implied 12% allocation, despite rising risks from inflation, dollar debasement, and geopolitical uncertainty.

-

Gold has preserved purchasing power over centuries and, since the end of the gold standard, has outperformed bonds in real terms, supporting its long-term role as a portfolio diversifier.

-

WisdomTree’s Efficient Gold Plus Equity Strategy Fund (GDE) and WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN) provide capital-efficient tools to add gold exposure without reducing equity positions.

For most investors, zero gold exposure is not neutral—it's an active ~10% underweight relative to global market portfolios. And that gap is growing harder to justify as new portfolio tools become available that can enhance portfolio efficiency, diversification and optimization.

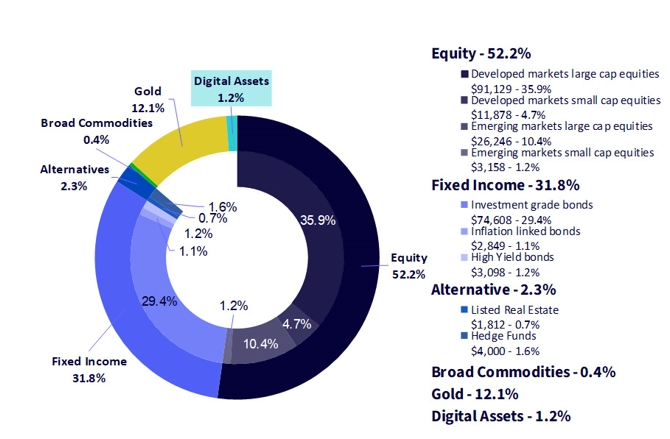

The Market Portfolio Tells an Uncomfortable Truth

A market-cap-weighted view of global investable assets implies roughly:

-

52% equities

-

32% fixed income

-

16% alternatives, including:

-

~12% gold

-

~1.2% digital assets

-

3% in real estate and other alternatives

-

The Liquid Market Portfolio

Source: Bloomberg, WisdomTree, 12/31/25. Market caps are shown in USD billion. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investment may go down in value.

Passive investing has been gaining share within the asset classes, particularly equities. But the framework for looking at the investment opportunity set can be generalized to broader portfolio allocations. And the data is clear: a traditional 60/40 portfolio is structurally misaligned with the global opportunity set. It is overweight financial assets and underweight real assets, particularly gold.

Why this matters:

-

Most investors have 0–3% in gold and very little in diversified commodity allocations. I was recently looking at the total assets in diversified commodity strategies in the U.S. and there was a total of just $17 billion invested across the entire ETF industry that is over $13 trillion in size.

-

I sympathize with this under-allocation – for a decade following 2008, commodities went largely nowhere. But commodities showed some of their diversifying potential for hedging inflation and geopolitical risk following the Russian invasion of Ukraine.

-

Commodities are critical for powering much of the AI revolution and energy needs and rare earth metals are key focal points for the geopolitical developments around the globe. I think this low allocation to broad based commodity funds is a major mistake. Our pie chart above suggesting a neutral allocation at ½ of 1% is just based on the open interest of the futures market – and there is no easy way to suggest what should be neutral, but our historical work suggests as much as 10-15% allocations to commodities would better optimize portfolios and hedge key risks.

-

If investors hold 0-3% in gold, this is an active bet against inflation hedging, monetary debasement, and diversification.

-

International exposure is also typically too low in global allocations, again understandably because of the U.S. exceptionalism and tech dominance for the last 15-years. 2025 was the first breakout year for international in a long time, but gold did even better. Investors do not have to make bets on the euro, yen, or Chinese yuan in emerging markets to get protection from the falling purchasing power of the U.S. dollar. They can add gold in a capital efficient way on top of U.S. stocks to accomplish similar outcomes.

The Real Constraint Isn't Conviction—It's Capital Efficiency

The common objection:

"I like gold, but I don't want to sell stocks or bonds that have more fundamental income streams to fund it."

That objection is rational. Selling productive assets to add a non-yielding one often feels like a step backward.

But WisdomTree pioneered an ETF product range that overcomes this challenge. You don't need to reallocate to gold from stocks or bonds if you can overlay it very capital efficiently.

That's the design philosophy behind our capital-efficient gold strategies:

-

Adds gold exposure via the futures market

-

Preserve core equity and fixed income

-

Improve portfolio resilience without forcing trade-offs

Gold's Long-Term Role: Keep up with Inflation, Not Growth Engine

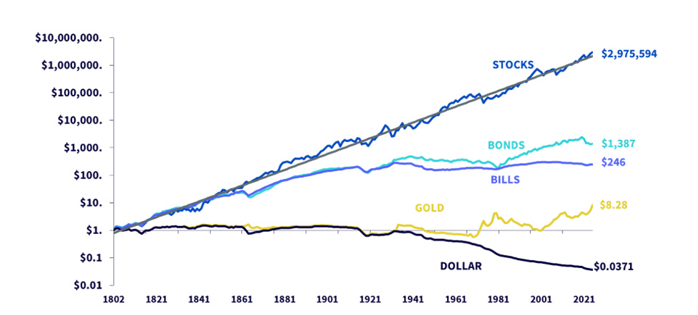

Jeremy Siegel's Stocks for the Long Run provides critical historical context.

Since 1802: Gold Preserved Purchasing Power

-

Gold: ~0–1% real return

-

Stocks: ~7% real

-

Bonds: ~3% real

January 1802–December 2025

Source: Siegel, Jeremy, Stocks for the Long Run (2022) with updates to 2025. Past performance is not indicative of future results. You cannot invest directly in an index.

Gold was never meant to beat equities over centuries. Its job was to keep up with inflation and protect purchasing power—which it did.

The purchasing power value of the U.S. dollar declined 93% over 200-years. Gold overcame that inflationary bias and returned positively after inflation.

But Siegel's 200-year study masks another interesting story over the last 50-years.

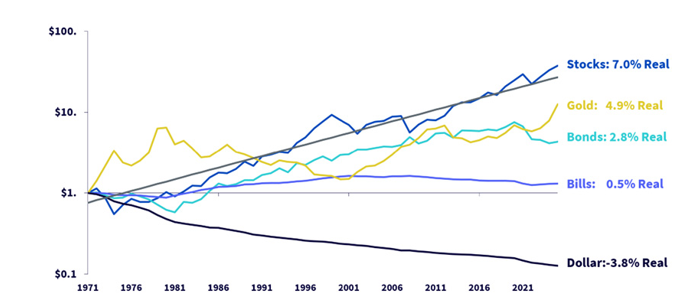

Since 1971: A Regime Shift Changed the Math

Once the gold standard ended, gold was liberated from artificially low pricing.

From 1971–2025 (real returns):

-

Stocks: 7.0%

-

Gold: 4.9%

-

Bonds: 2.8%

-

T-Bills: 0.5%

-

Dollar: -3.8

Gold didn't just hedge inflation—it outperformed bonds in real terms during the fiat-currency era.

January 1971–December 2025

Source: Siegel, Jeremy, Stocks for the Long Run (2022) with updates to 2025. Past performance is not indicative of future results. You cannot invest directly in an index.

The Forward Case for Gold: Why This Regime Persists

There is some natural fear today about adding to gold after chasing an enormous performance run. But there are some structural tailwinds for continued gold allocations.

1. Global Debt Dynamics

-

Sovereign debt-to-GDP ratios remain historically high

-

Financial repression (inflation) while keeping rates low is the path of least resistance. The way countries have managed debt levels across time is to allow inflation.

-

Gold benefits when real rates are capped

2. Dollar Debasement Risk

-

Persistent fiscal deficits provide some concern for the bond market and gold overlays can provide diversification from pure bond allocations.

-

Long-term erosion of fiat purchasing power even without crisis

3. Central Banks Are Voting with Their Balance Sheets

-

Emerging market central banks continue to accumulate gold. There are many reasons, but the geopolitical stress in which Russia was caught off from its U.S. dollar reserves provides motivation for holding less U.S. Treasuries and more real assets.

-

This is price-insensitive, structural demand and we see central banks continuing to accumulate, particularly China

Gold doesn't require catastrophe it simply requires policy constraints and geopolitical uncertainties.

How We Think About Implementation: Two use cases. Two tools. One philosophy.

GDE — Strategic Gold, Capital Efficient

-

Designed as a long-term core holding to replace other equity funds

-

Adds gold futures exposure on top of U.S. large-cap equities

-

Seeks diversification and inflation resilience without selling core stock positions.

Use case: Investors who believe gold belongs strategically in portfolios, but don't want to give up equity exposure to get it.

GDMN — Tactical Conviction in Gold & Miners

-

Higher-octane exposure. This was among WisdomTree and the industry's best performing Funds in 2025 as miners rebounded.

-

Leans into gold miners, which historically delivered subpar returns. Miners have a reputation for being poorly managed capital allocators. This run in gold prices came while energy prices remained low. Some of the current geopolitics looks to provide a ceiling for oil prices (particularly around Venezuelan oil that we expect to become better globally supplied in coming years). This gives a positive backdrop for gold miner margins.

-

This Fund is more tactical and best suited for investors with a strong near-term bullish view and want more torque to the trade.

-

Gold miner flows were very modest to non-existent in 2025, despite strong performance.

Use case: When fundamentals, flows, or macro regime shifts favor gold leadership.

Bottom Line

-

Zero gold allocation in a portfolio is not neutral, it's an under-weight bet against gold.

-

The global market portfolio argues for meaningfully higher real-asset exposure.

-

History shows gold's value is regime-dependent, and there are some positive forces supporting gold over the coming years.

-

Capital efficiency matters. You shouldn't have to dismantle your portfolio to fix its biggest blind spot.

Adding gold doesn't have to be about replacing stocks or bonds. It's about making portfolios more complete efficiently.

Related: Positioning Portfolios for the Rise of Defense ETFs

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile. The Funds’ investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains.

The Fund is actively managed and invests in U.S listed gold futures and U.S. equity securities. The Fund’s use of U.S. listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate.

The Fund is actively managed and invests in U.S.-listed gold futures and global equity securities issued by companies that derive at least 50% of their revenue from the gold mining business (“Gold Miners”). The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. By investing in the equity securities of Gold Miners, the Fund may be susceptible to financial, economic, political, or market events that impact the gold mining sub-industry, including commodity prices and the success of exploration projects. The Fund may invest a significant portion of its assets in the securities of companies of a single country or region, including emerging markets, and thus, the Fund is more likely to be impacted by events and political, economic, or regulatory conditions affecting that country or region, or emerging markets generally.

Past performance is not indicative of future results.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S.

This WisdomTree article is provided as part of a paid sponsorship.