Trending

Acknowledging the 50-year anniversary of the launch of exchange-listed options (4/26/1973), we decided to explore how options – a derivative alternative tool - can play an important part in asset management to enhance income, dampen volatility, and provide a strategy for further diversification to address different market environments.

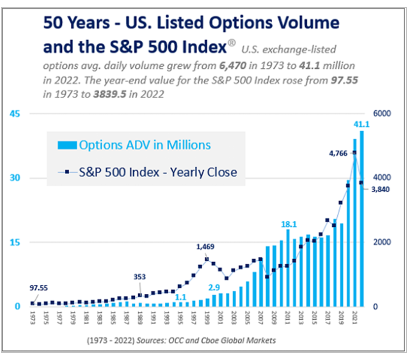

Through these past 50 years, U.S. exchange-listed options daily volume grew from 6,470 in 1973 to 41.1 million in 2022. The average daily volume of calls and puts on U.S. exchanges has grown to 46 million contracts in the first quarter of 2023. With such tremendous growth, the natural question would be what are some of the catalysts for this growth and how are asset managers using options in their portfolio construction?

To explore how asset managers are using options, we reached out to Institute members Kim D. Arthur and James W. Concidine, two of the portfolio managers of the Main BuyWrite ETF, and Darol Ryan, Managing Partner, at Main Management – an independent, San Francisco-based advisory firm established in 2002 that was an early pioneer in managing all-ETF portfolios and utilizing option writing strategies in some of their investment offerings. Their BuyWrite ETF (ticker: BUYW) had a top decile ranking in the Morningstar Derivative Income category and a positive performance return in 2022 which motivated us to ask them questions to understand their perspectives and experiences on using options in investment portfolios.

Hortz: What do you feel is behind the huge increase in the use of options especially over the past few decades?

Arthur: The growth in options usage has a lot to do with investors seeking more diversification in their portfolios. In the minds of a lot of financial advisors and investors, traditional asset classes (stocks and bonds) have become insufficient to fully address the complexities of the market and investors' needs. People began exploring alternative strategies, like options-based strategies, to enhance returns and manage risk more effectively.

Concidine: And adding to that, options are a very strong tool in the toolkit, even for long-term investors. Some advisors dismiss the idea of options as overly complex or solely for making high-leverage risky bets. However, by properly employing them to diversify and hedge risk, you can handle a variety of market scenarios.

Hortz: You started your BuyWrite covered call option strategy 18 years ago, a few years after the founding of your firm. What was your motivation and thinking behind offering this strategy?

Arthur: We developed the BuyWrite strategy as an alternative sleeve for our High-Net-Worth clients. Most traditional portfolios have equities and fixed income but our clients were asking for more diversification. So, we created this third category – an alternative category utilizing option writing that sits between the other two asset classes.

Concidine: Our group had strong experience in options. I personally started selling calls in the mid-1970s. Covered call writing becomes more interesting when you can do it on indices and ETFs. We also knew that an option writing strategy works well in an up or down 15% market or in a sideways market. There have been many times in stock market history where the stock market has gone nowhere for an extended period. The strategy was developed to also be an effective diversifier for a traditional portfolio that also addressed different market environments and conditions.

Hortz: Can you explain more specifically what are the different components of the strategy or portfolio?

Arthur: The Main BuyWrite is a hedged equity strategy that actively writes call options on a thoughtfully chosen set of 8-12 sector and industry ETFs driven by fundamental analysis. This approach creates a three-pronged return stream. The first potential source of returns comes from the ETF allocation, based on the 20 years of fundamental sector analysis expertise at Main Management. The second potential source is the options premiums generated by selling covered call options against the underlying ETFs, which may vary based on expiration and strike price (in-, at-, or out-of-the-money). Lastly, the dividend income from the underlying equities historically adds to the other two components. Our strategy's combined effect enables the ETF to provide a 50bps monthly yield (or 6% annually), making it an attractive option for income-seeking investors.

Hortz: What is your investment process in selecting and managing the underlying ETF positions?

Arthur: Our investment process for selecting and managing the underlying ETF positions involves a fundamental-with-a-catalyst approach. We first start bottom-up by focusing on sector and industry fundamentals – valuations versus history and the rest of the market, revenue and earnings growth rates, etc. Then, once we find a sector/industry that appears attractive, we determine if there is a catalyst at the macro level by analyzing market trends, economic indicators, and global events. The goal is that these potential catalysts may help drive reversion-to-the-mean on the valuations.

Hortz: How does your overall investment strategy compare and contrast to other managers that may be developing similar strategies utilizing options?

Concidine: As a hedged equity strategy, our first step in the process is to find the most attractive sector ETF. Then we find the right options to sell, the appropriate strike and maturity. This “dual-active” approach, on both the equities and the options overlay, is especially rare in the hedged equity universe – so many other managers are active only on the equity side or the options side – or even completely passive/systematic in both! In my mind, this approach is underused likely because the analysis processes for equities and options are considerably different and it is rare for managers to have adequate experience on both sides. This approach allows us to seize opportunities and manage risk more effectively, which can be quite exciting in dynamic market conditions.

Arthur: An advantage of our strategy is the different levers that the Investment Committee can pull depending on the market and sector outlook. In a down-market, the underlying ETF allocation can shift to a more conservative tilt, and the calls may be written in-the-money as protection. In an uncertain market, the ETF allocation may shift to opportunistic, and the calls may be written with a barbell approach to limit market exposure. In a strong up-market, the ETF allocation may be more aggressive, and the calls can be written more tactically.

I also want to highlight the tax awareness of the strategy – particularly important when distributing income. Many other managers may boast a strong yield on their products, but if you look at the after-tax returns – the true return many investors are getting – those are quite weak as the manager ends up so focused on the high income that they forget about the other parts of the strategy. We started the firm with taxable money 20 years ago, so tax awareness has always been a core pillar of the firm’s investment process.

Hortz: What should investors know about option writing that they may not be aware of?

Arthur: Investors should recognize that option writing offers flexibility and can be tailored to various market conditions, providing consistent income and risk management. As options markets continue to expand in liquidity and cover new ETFs, it allows us to be even more targeted with our allocation - essentially giving us a sharper scalpel in our toolkit.

Hortz: You mentioned previously that option writing strategies have historically done well in certain investment environments like a sideways market. Do you feel we are in or entering a particularly conducive market environment for this strategy?

Concidine: While it is always difficult to predict the exact market environment, it does seem that we could be entering a period where option writing strategies could thrive. With increased market uncertainty and potential for volatility, a sideways or “choppy” market could become more common. In such scenarios, option writing strategies can provide investors with consistent income and risk management opportunities, making them particularly attractive as a portfolio diversifier during these times.

Hortz: What advice or recommendations can you offer advisors on the asset allocation benefits of an option writing strategy for a client’s portfolio?

Ryan: Incorporating an option writing strategy into a client's portfolio can serve as a powerful diversification tool, given its low correlation with traditional asset classes like stocks and bonds. This means that it can potentially provide a different source of returns and risk management, even during times when other investments may underperform.

When considering asset allocation, advisors should look at how an option writing strategy fits within a client's overall risk tolerance and investment objectives. We generally target an allocation of 10-15% to an option writing strategy within a diversified portfolio, funded from a blend of equity and fixed income, enhancing its overall risk-return profile. The key is to find strategies that strike the right balance between income generation and capital growth, while effectively managing risk and optimizing tax efficiency. By doing so, advisors can help clients navigate various market conditions and build more resilient, all-weather portfolios.