Trending

Written by: Gabriela Santos

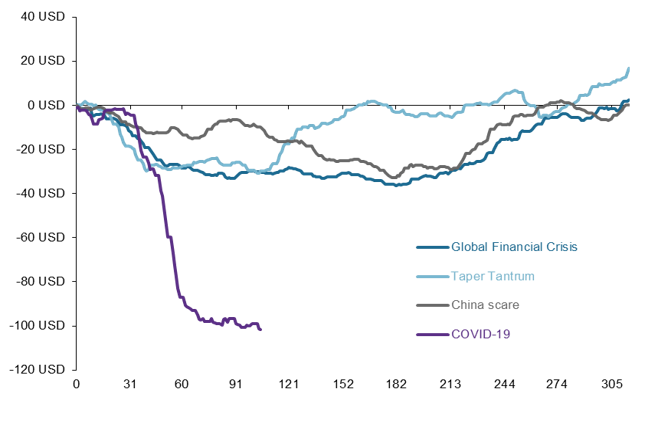

During the first three weeks of March, investors stampeded out of riskier markets and rushed to safe assets. In the process, 100 billion USD flowed out of emerging market (EM) stocks and bonds –more than three times the outflows seen during each of the previous three risk-off periods. Over the past month, outflows have stabilized; however, foreign investors have yet to return to the asset class. Now that the dust has settled somewhat, investors are wondering: what opportunities were created by the COVID-19 earthquake?

For EM countries and companies, the large volume of foreign outflows does present some challenges and reason for caution. However, it also creates opportunities for investors who can sift through the rubble carefully, have a longer time horizon and can take advantage of a better entry point in terms of valuations.

The challenge: EM debt

The large outflows have caused a weakening in EM currencies versus the U.S. dollar, making it more expensive for EM governments and companies to service their U.S. dollar-denominated debt. Thankfully, the percentage of EM U.S. dollar-denominated debt as a share of total debt outstanding has decreased significantly over the past couple of decades, given previous experiences with moments like these. As such, outside of select frontier EM markets, investors should not expect significant sovereign defaults. However, investors are now demanding a higher premium for investing in EM debt, which raises the costs for EM countries and companies to finance themselves. In addition to a challenging environment for budgets, this suggests that downgrades can be expected in the EM debt space. While investors in developed markets are starved for yield, they should tread carefully with EM debt, focusing on higher rated credits and very thoughtful security selection.

The opportunity: EM Asia equities

The pre-existing structural trend of the emergence of EM Asia has stayed intact and even strengthened during this episode. Over the next decade, the Brookings Institute estimates that 1.5 billion people in EM Asia will enter the middle class (1 billion alone in China and India), providing a significant tailwind to revenue growth in consumer-oriented sectors in EM Asian equities. Even in the shorter-term, several countries in North Asia have provided good examples of how to reopen their economies in the face of COVID-19 in a risk adjusted way. Lastly, another pre-existing structural trend that has only been strengthened is technology, which is well represented in EM Asian equities, with a 21% weight. Given the past couple of months of risk aversion, the entry point into these themes has improved, with EM Asia’s price-to-book ratio moving down 12% compared to December 31st.

Outflows from emerging markets create risks – and opportunities

Net non-resident purchases of EM stocks and bonds, cumulative total (USD bn) and days

Source: IIF, J.P. Morgan Asset Management. Data are as of May 5, 2020.