Trending

It has been said that the stock market climbs a “wall of worry”. The rationale behind that sentiment is that while risk is ever-present, a rising market is bent upon overcoming them. When we look at the Cboe Volatility Index (VIX), it is quite clear that traders are not overcoming risks, they may instead simply be ignoring them. Thus, Mr. Market looks like Spiderman in scaling the current worry wall.

Bearing in mind our standard disclaimer, that “VIX is not a fear gauge though it plays one on TV”, it is helpful to remember that sentiment is not a direct component of the VIX calculation. The Cboe describes it thus:

The VIX Index measures 30-day expected volatility of the S&P 500 Index. The calculation takes as input the market prices of SPX options and SPXW options as well as U.S. Treasury yield curve rates.

That said, we would be naïve to assert that sentiment plays no role in expectations for volatility over the coming 30 days. VIX notably has an inverse correlation with the underlying S&P 500 Index (SPX), and since market participants tend to perceive volatility in negative terms, we have come to associate higher levels of VIX with fear. Mathematically identical moves are viewed vastly differently, depending upon direction. Think of normal investor behavior: a -1% decline is cause for concern, while a +1% rally is often taken in stride. This is where our concept of “socially acceptable volatility” comes into play. Up is good, bad is scary.

This is why we have typically contended that VIX is better thought of as a proxy for the demand for hedging protection from institutional investors. This is reflected in the correlation between VIX and SPX skew. If there is a perceived need for insurance (usually meaning put protection), its cost will go up. I have explained this as the price of umbrellas during a drought. If there are few clouds on a sunny horizon, then there is little demand for rain gear; if a sudden downpour arrives, some will be incentivized to pay a premium for the protection.

Yet at some level, volatility assumptions should reflect the likelihood of “known unknowns” that could adversely affect stocks. To stretch the prior analogy, the news and economic calendar is a bit like long-range radar. Over the coming 30 days – the period covered by VIX – there is no shortage of potential disturbances on the horizon. Those include the expiration of the tariff moratoria, and the start of earnings season. It is understandable why VIX would have fallen after hostilities involving Iran have ceased, but we are back to asserting a relative lack of concern about impending events.

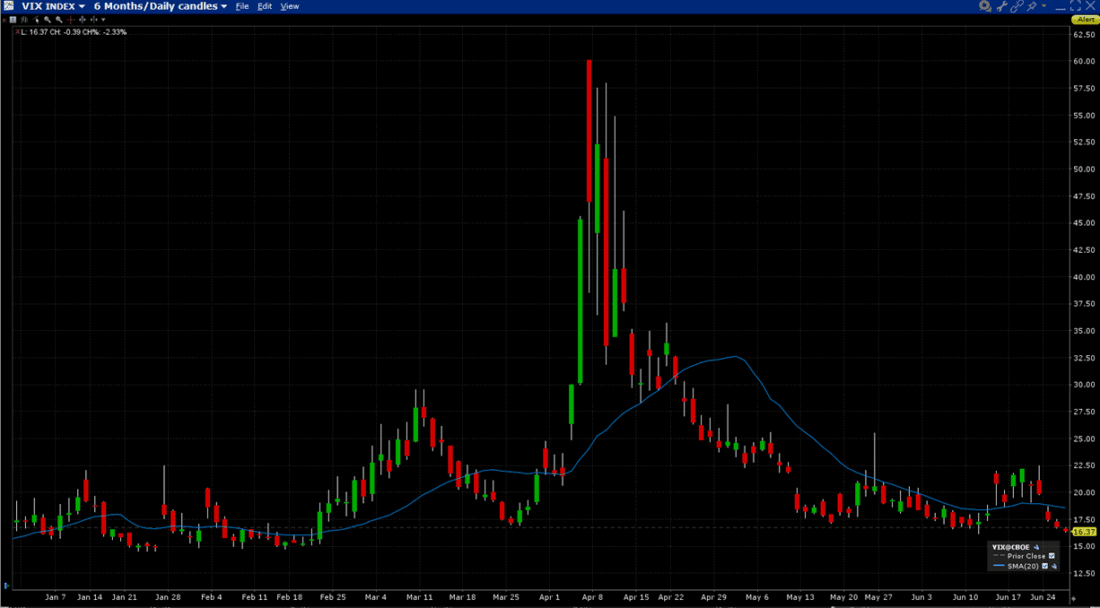

VIX 6-Months Daily Candles with 20-Day Moving Average

Source: Interactive Brokers

Once again, momentum is the key. The positive vibes around the quest for new highs is outweighing more prosaic concerns. Interestingly, I was prepared to write how Micron Technologies’ (MU) solid results and guidance after yesterday’s close were a catalyst for another round of tech enthusiasm overall, and semiconductors specifically, were a valid reason for those sectors’ continued leadership today. But MU gave back its early gains to trade lower, so that isn’t the reason for the rally. It is more about a rally for its own sake. Does anyone really doubt that SPX will fail to touch a record high after constant reporting about how close we are to it?

Also baked into the rally is the implicit hope that tariffs will get pushed back once again. If there was a concern about higher tariffs, stocks would hardly be so sanguine. One reason for hope was a comment by Council of Economic Advisers Chair Stephen Miran, that tariff deadlines could get pushed back with countries that are negotiating in good faith. Since we don’t know who exactly is negotiating with whom and how the talks are going, this could turn into a case where the whole pile of deadlines gets moved once again. The market has been right to use this idea as a catalyst before. VIX is telling us that is once again the base case for ascending that wall of worry.