Trending

Navigating Medicare is a cause of frustration for many retirees. I recently felt that frustration when my dad was in and out of the hospital. Medicare is the primary health insurance for 60 million Americans and has 3 main Parts: A, B and D. Most individuals attain Medicare at age 65 or by having a qualifying disability. For many retirees, health care costs are one of the larger concerns in retirement. To further serve my clients through the complexities of Medicare, I decided to get health and life insurance licensed. Client First Capital is licensed to sell Medicare Advantage plans through United Health Care (the provider endorsed by AARP).

In this article we are going to review a few key points that can be confusing about the Original Medicare (Parts A and B). The next article will compare a Medicare Supplement plan to a Medicare Advantage plan and set out some of the planning considerations around health insurance and Tricare. Keep in mind this is not an exhaustive analysis since there are multiple different Medicare plans and benefit levels. We are only focusing on Parts A and B, and nuances that can be hard to digest based on my experience. The next article will also dig deeper into other parts of Medicare like Part D; since the average 70+ year old relies on 4.2-4.5 prescriptions drugs. Understanding the difference in Plan D and a Medicare Advantage plan is also important. Consider this article as part 1 of 2.

Medicare Part A

Medicare Part A (“Part A”) covers the costs associated with hospitalization. In general, Part A covers inpatient care, skilled care, nursing home care (NOT long-term care), hospice and some home health care. Funding for Part A primarily comes from payroll taxes and most individuals do not have an additional premium. It is important to note that for Part A the benefit period starts on day 1 of being admitted into a facility and it ends once a covered patient has not had treatment for 60 consecutive days. The coverage under Part A becomes confusing if one is readmitted multiple times within a calendar year.

Part A charges a deductible of $1,408 (2020) for each benefit period. Although the cost can vary by type of facility, the concept of tiered periods remains the same. Hospital days 2-60 cost = $0; days 61-90 cost $352/day; and days 91-150 cost $704/day. The benefit for days 91-150 comes from your lifetime reserve days, which can only be used once during your lifetime, although they can be used in different benefit periods.

Below is an example to illustrate how the costs work regarding hospital stays:

Jill is admitted to the hospital in February, after a hip replacement surgery. She is released after 3 days. Her Part A cost for the hospital stay would be the deductible of $1,408.

After 2 weeks, Jill is having problems with her hip as a result of her surgery and has to go back to the hospital. She stays a total of 2 days after being released. Since she is still within her first benefit window of 60 consecutive days her Part A cost for both hospital stays are her deductible of $1,408 (i.e. Jill does not have any additional costs for the second hospital stay).

However, if for example, Jill was very sick after her initial discharge and her second hospital stay exceeded 60 days, then she would have to pay $352 a day for each day beyond 60th day. Meaning a 65- day hospital visit would cost: $1,408(the deductible) + (5 days X $352) = $4,576.

Now, let’s consider if Jill used up all of her lifetime reserve days and still needed hospital care for 35 more days. The table below outlines each portion of the expense:

| Type | Cost |

|---|---|

| Medicare Part A deductible | $1,408 |

| Co-pay for days 1-60 | $0 |

| Co-pay for days 61-90 @$352 per day | $10,560 |

| Co-pay for days 91-150 @$704 per day | $42,240 |

| Full cost for days 151-185 @$1,200 per day | $42,000 |

| Total | $96,208 |

Keep in mind these are just hospital costs and do not include doctors, labs and other potential charges. The overall medical bill will be much greater. From a planning perspective this expense can create a lot of stress on a family. Also, you may have other family members who may get sick and rely solely on Medicare for their health insurance needs. It’s important to remember that Medicare is an individual plan with no individual or family maximum out of pocket. There are supplement plans that limit exposure. But there remains a potential that your assets or strategies for multi-generational planning may be impacted by a significant health care event.

Medicare Part B

Part B pays for the care you receive (i.e. doctors, labs and tests). For most services there is a $198 deductible and then a 20% co-pay. And like any insurance plan out there it can be difficult to understand what is covered and what is not. This website: https://www.medicare.gov/coverage allows you to check online if a certain procedure or lab test is covered. The next best option is to ask the doctor and get it in writing. Two places where most people have a misunderstanding with Part B is called “Medicare Assignment” and IRMAA.

Let’s tackle Medicare Assignment first. Essentially not all doctors accept Medicare payment as payment in full. You may still be on the hook for the difference between what Medicare will pay and the actual bill. This is called excess charges and it can vary greatly from doctor to doctor due to supplies and test used. Let’s look to our first example to illustrate this point.

Before getting her hip surgery, Jill had a series of doctor appointments. Her doctor accepts Medicare Assignment. In this instance, Jill would need to pay her deductible plus a 20% co-pay.

If Jill’s doctor did not accept Medicare Assignment, then Medicare would pay a reduced amount to the doctor. This reduced payment from Medicare means that Jill would need to pay out of pocket for any shortfall between Medicare reimbursement and total cost.

Most doctors accept Medicare Assignment; however, this is not true with all doctors. In some cases where the doctor does not accept assignment, you would need to file the Medicare claim yourself. It is important to know if a doctor does or does not accept Medicare Assignment upfront when scheduling appointments with new doctors.

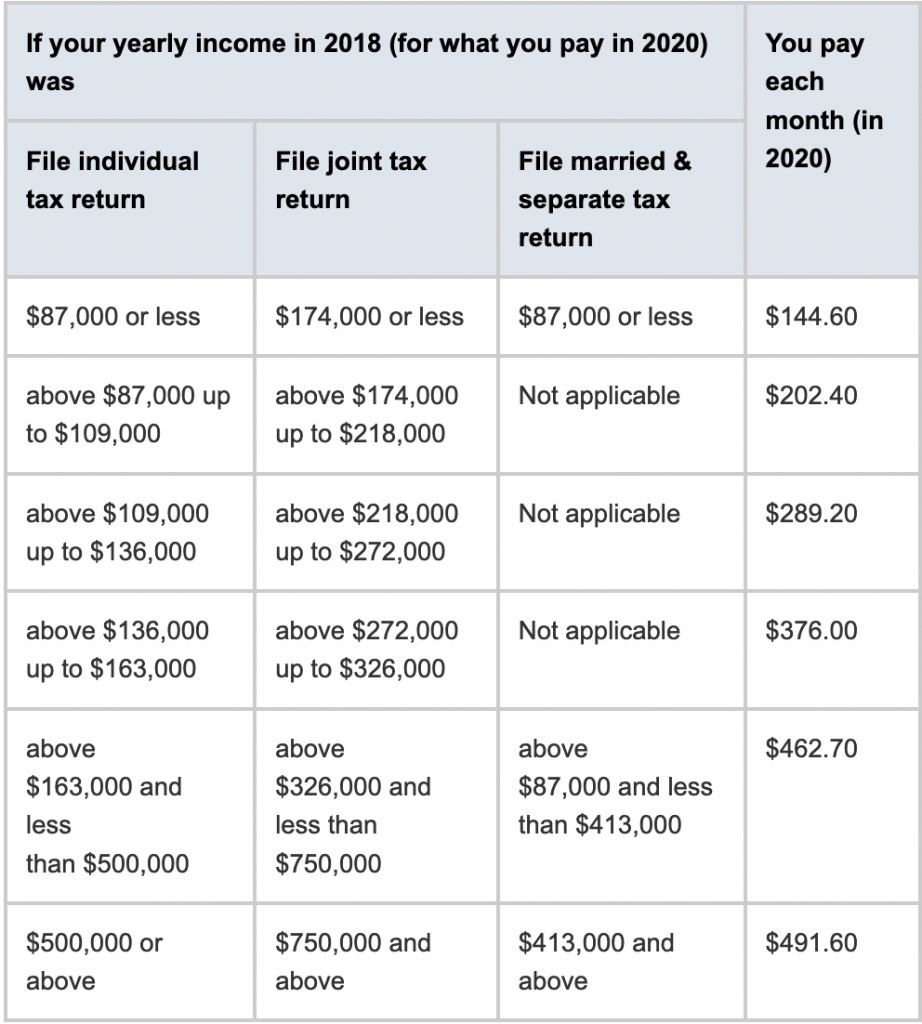

The second misunderstood part is IRMAA which stands for Income Related Monthly Adjustment Amount. Medicare uses your modified adjusted gross income from two years ago to calculate what your premium will be for Medicare Part B. The reason for the 2 years back is that it takes time for your tax return to go from the IRS to Social Security. Below is a chart for 2020.

Source: https://www.medicare.gov/your-medicare-costs/part-b-costs

The reason it is often misunderstood is because these numbers do not line up with IRS tax tables. It is important to make sure you consider this table while doing any tax planning. Often times when we take extra gains in a given year or Roth conversions, we are trying to reduce future gains in income and reduce the likelihood for a premium increase. And just like with taxes, there is also what I call ‘the widows trap’ here as well. For example, if your MAGI as a married couple is 200k, the part B cost is $289.20 per person. If you are a surviving spouse and have the approximately the same amount of income then your premium for the same insurance jumps up to $462.70.

What we have covered so far is called the Original Medicare plan. Everything else is an additional add on. The next article will cover these add-ons including Part D (prescription plans), Medicare Advantage Plans and how Tricare and Medicare work together.

For those that are Medicare eligible, please note that annual enrollment starts October 15th. We can walk you through your plan and other plans that are out there to give you the peace of mind of having the plan that is right for you.

Feel free to connect with us by emailing us or filling out our contact form. If you would like to subscribe to the newsletter for weekly updates from the team at Client First Capital.