Trending

High-net-worth (HNW) clients are increasingly looking beyond domestic markets. Whether it's property in Portugal, equities listed on the ASX, or a private equity stake in a Singapore-based fund, cross-border investing has moved from the fringes of wealth management to the mainstream.

For financial advisors, this creates both opportunity and complexity. Geographic diversification can strengthen a portfolio — but it also introduces currency risk, tax complications, and operational friction that require careful management.

This article is for financial advisors and wealth managers navigating the practicalities of helping clients invest across borders.

Why Cross-Border Investment Is Accelerating

Several structural trends are driving HNW capital across borders:

- Domestic market concentration risk: US equities account for approximately 63% of global market capitalisation, according to MSCI. Clients with US-only portfolios carry significant single-market exposure.

- Real estate diversification: The Knight Frank Wealth Report found that 29% of ultra-high-net-worth individuals plan to buy property abroad in the next two years, driven by lifestyle, residency programmes, and yield-seeking behaviour.

- Private market access: Cross-border private equity and venture capital funds offer return profiles unavailable in any single domestic market.

- Residency and citizenship planning: Investment migration programmes in countries like Portugal, Greece, and the UAE tie financial investment to personal mobility.

The Currency Challenge Advisors Must Address

Cross-border investment returns are denominated in foreign currencies — and that introduces a variable many advisors underweight in their planning.

How Currency Risk Erodes Returns

Consider a US-based client who invested in an Australian equity fund in early 2024. The fund returned 12% in AUD terms. However, the AUD depreciated 6% against the USD over the same period, reducing the realised return to roughly 5.3% in USD terms.

This isn't a hypothetical edge case. Currency movements routinely add or subtract 3-8% from cross-border investment returns annually. For a $5 million allocation to international assets, that's a $150,000–$400,000 swing that has nothing to do with the underlying investment's performance.

Multi-Currency Accounts as a Strategic Tool

Rather than converting currencies at the point of each transaction which would incur spreads, fees, and unfavourable timing, advisors are increasingly using multi-currency accounts to hold, manage, and deploy capital in multiple currencies simultaneously.

OFX provides a detailed overview of how multi-currency accounts work and why they've become essential infrastructure for cross-border financial management.

Key advantages for HNW clients:

- Strategic timing of conversions: Hold foreign currency and convert when rates are favourable, rather than accepting the spot rate at the moment of need

- Reduced transaction costs: Consolidating currency conversions into fewer, larger transactions typically reduces spread costs by 40-60% compared to multiple small conversions

- Simplified reporting: A single account with multiple currency balances is easier to track and report than multiple foreign bank accounts

- Operational efficiency: Pay foreign expenses, receive foreign income, and manage investments without constant currency conversion

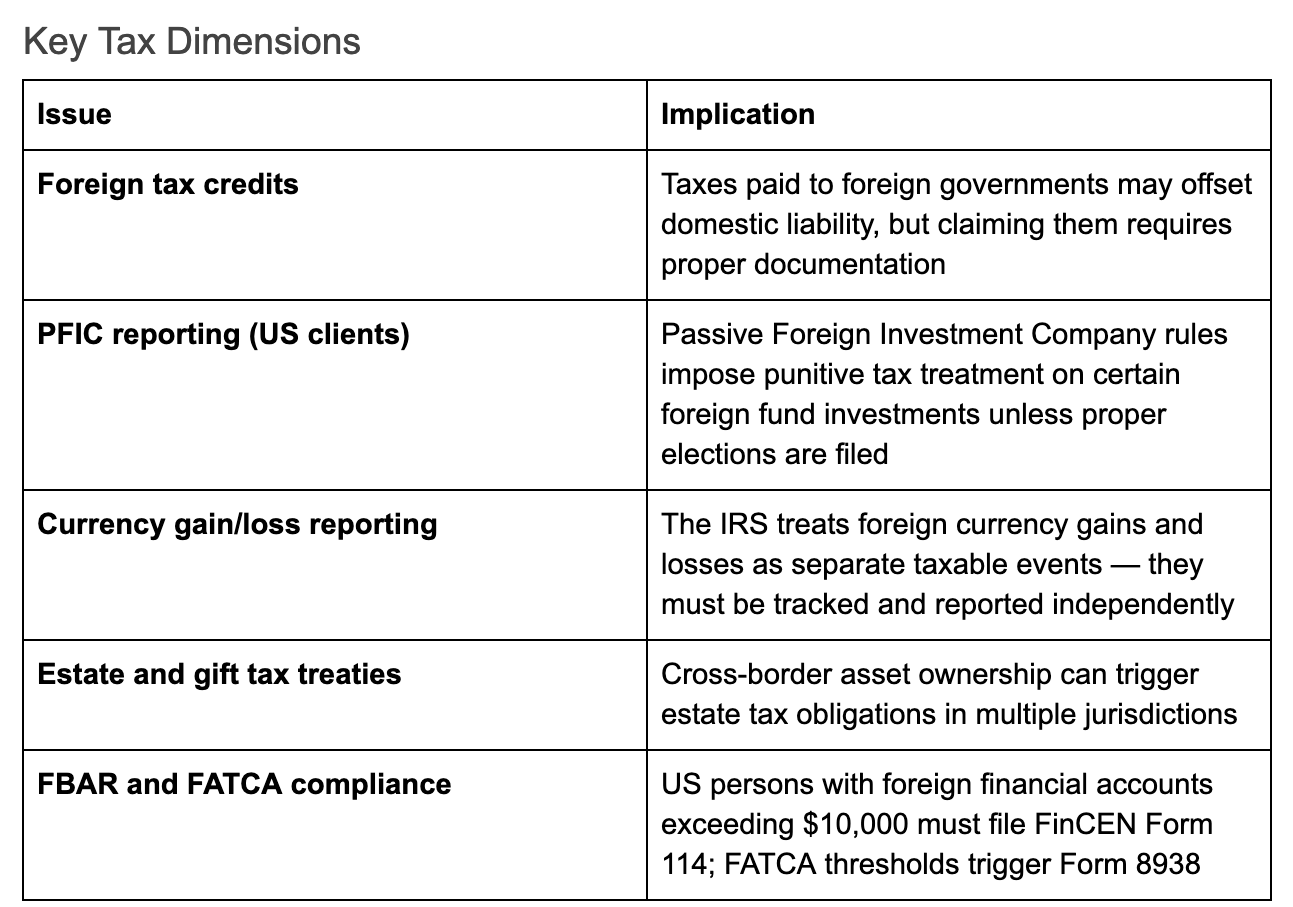

Tax Considerations Advisors Cannot Overlook

Cross-border investing creates tax reporting obligations that domestic investments don't. Advisors who fail to account for these put their clients at risk.

Advisors should coordinate with tax professionals who specialise in cross-border reporting. The cost of expert tax advice is minimal compared to the penalties for non-compliance — FBAR violations alone can reach $12,906 per account per year for non-wilful violations, according to the IRS.

Building a Cross-Border Investment Framework

Step 1: Assess the Client's International Exposure

Before adding cross-border positions, map the client's existing international exposure. Many clients already hold foreign assets indirectly through domestic funds, ETFs, or multinational equity holdings.

Step 2: Define the Currency Strategy

Decide whether to:

- Hedge fully: Eliminate currency risk entirely using forward contracts or hedged share classes

- Hedge partially: Protect against extreme moves while maintaining some currency diversification

- Leave unhedged: Accept currency exposure as an additional diversification layer

The right approach depends on the client's risk tolerance, time horizon, and the specific currencies involved. For stable G10 currency pairs (USD/EUR, USD/GBP), unhedged exposure is often acceptable. For emerging market currencies with higher volatility, hedging becomes more important.

Step 3: Optimise the Operational Infrastructure

The operational mechanics of cross-border investing — how money moves, where it's held, how conversions happen — materially affect net returns. Best practices include:

- Use multi-currency accounts to centralise foreign currency holdings

- Batch currency conversions to reduce transaction costs

- Establish relationships with FX specialists who offer better rates than retail banks — institutional spreads can save HNW clients tens of thousands annually on large transfers

- Automate reporting where possible to ensure tax compliance without manual effort

Step 4: Monitor and Rebalance

Cross-border allocations require more active monitoring than domestic positions. Currency movements, geopolitical events, and regulatory changes in foreign markets can shift the risk profile of international holdings faster than domestic equivalents.

Set quarterly review cycles for cross-border positions, with triggers for out-of-cycle reviews if major currency moves (>5% in 30 days) or geopolitical events occur.

The Advisor's Competitive Advantage

Clients with $5 million or more in investable assets increasingly expect their advisor to manage cross-border complexity, not just domestic portfolio construction. Advisors who build competency in currency management, international tax coordination, and global operational infrastructure will differentiate themselves in a market where international diversification is no longer optional — it's expected.

The advisors who thrive will be the ones who treat cross-border investing not as a specialty add-on, but as a core capability of modern wealth management.