Trending

Written by: David Lebovitz

2023 has proven to be much better for equity markets than expected. Coming into the year, many were forecasting a challenging macroeconomic environment and increasing headwinds to corporate profits. In the event, however, the economy has continued to grow at an above-trend pace and corporate earnings are on track for a +10% gain. That said, we have begun to see a divergence between different measures of earnings, leading many to ask which measure of earnings they should focus on.

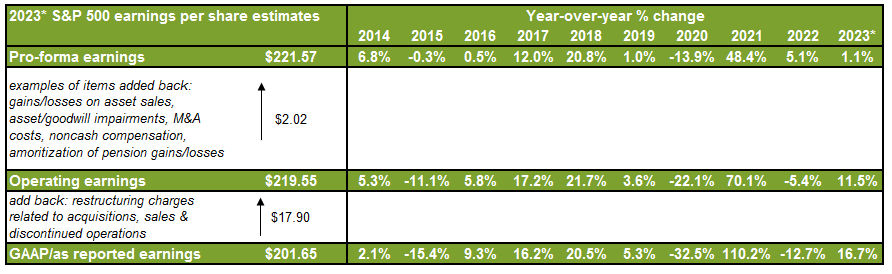

In general, there are three main measures of corporate profits - numbers based on the national account data, operating earnings and pro forma earnings. While the market prices off of pro forma earnings, these numbers are adjusted by the analyst community, which can make it more difficult to compare current earnings to prior periods. We understand the thinking behind some of the pro forma adjustments, but prefer to measure corporate profits using operating earnings, as not all of the adjustments being made seem appropriate. The table below highlights some of the key differences between these various measures of profitability.

The national accounts data looks at earnings for the economy as a whole, and therefore any divergence can be ascribed to differences in the underlying companies. When it comes to operating vs. pro forma earnings however, there have been some interesting trends at the sector level. Looking at expected earnings growth over the next twelve months, technology, communication services and financials show some of the largest gaps. For the financial sector, the pro forma number is higher, while the operating number is more robust for tech and communication services. For financials, the difference seems to stem from adjustments that are made based on losses on available for sale securities. In tech and communications, the issue seems to stem from recent M&A transactions, losses that have been written-off, as well as adjustments made to the top line.

One of the recurring issues with pro forma earnings is that analysts will adjust for assets where values have been marked down, both due to the sale of assets or goodwill impairments; while we recognize that these are technically “non-recurring” items, these asset values cannot be “written up” at some point down the road.

The question for investors, however, is which measure of earnings has the highest correlation with stock market returns. Based on data since 2001, pro forma earnings have the highest correlation; that said, the data is extremely skewed by the fact that operating earnings turned negative in 4Q08. If this data is excluded, operating earnings exhibit the highest correlation. This dynamic, coupled with the fact that there is a far longer time series available, suggests operating earnings are the best measure for long-term investors to use when attempting to gauge corporate profitability.

Difference in earnings measures lead to differences in growth rates

Source: Compustat, FactSet, Standard & Poor's, J.P. Morgan Asset Management. 2023 EPS are estimates. The 2023 pro-forma estimates are from FactSet Market Aggregate consensus estimates. The operating earnings and reported earnings estimates are from Standard & Poor's and are based on 4.0% of companies having reported 3Q23 earnings. Data are as of October 16, 2023.