Trending

Written by: Jordan Jackson

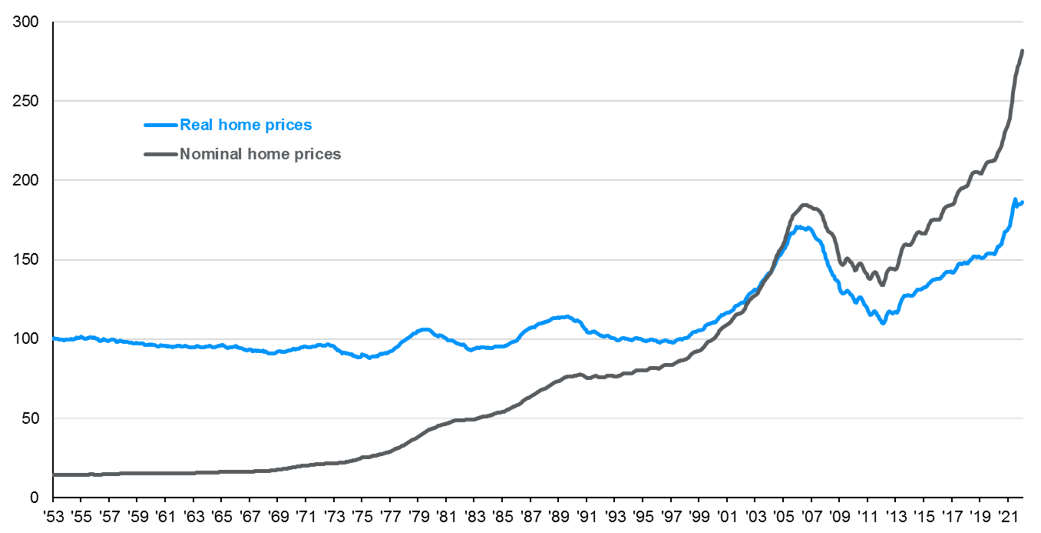

U.S. home prices have experienced incredible appreciation over the last decade, with particular strength in the years since the COVID-19 pandemic outbreak. In fact, as shown below, the recent surge in home prices have pushed the inflation-adjusted figure into record territory, yet the home buying experience remains competitive. As a result, investors may be wondering: what’s going on with the housing market? Furthermore, the prospect of even higher mortgage rates may have investors curious about the prospects for housing in the U.S.

To address the first part of this topic, it is possible to identify several contributing factors behind the dramatic home price inflation.

- Mortgage rates have been near historic lows thanks to the pandemic related policy response. In fact, the average 30-year fixed rate mortgage touched 2.65% in early 2021. Lower mortgage rates means that home prices can be higher while payments stay flat.

- The pandemic changed housing preferences. The combination of telecommuting becoming more viable and mobility restrictions have pushed people into larger, higher quality homes.

- Fiscal transfers and strong equity market performance have resulted in strong consumer balance sheets. Consumers have accumulated over $2.1 trillion in excess savings over the course of the pandemic, allowing for more spending.

- Housing inventory remains historically low. Home building activity is depressed, and existing homeowners may be wary of putting homes on market, perhaps believing that prices will continue to appreciate. As a result, data suggests there are only 843,000 existing single-family homes available for sale, relative to a long-run average supply of 2.1 million units.

Now, with mortgage rates on the rise, how should investors think about the future of the U.S. housing market?

- Higher mortgage rates should put downward pressure on home prices and perhaps encourage an increase in supply as current homeowners attempt to sell before mortgage rates become restrictive. However, the lack of new construction will likely dampen the impact of higher rates as demand remains robust.

- Shifting demographics could result in affordability challenges. As baby boomers retire and downsize, it is possible that their children will be unable to afford the houses their parents live in, pushing prices lower.

- Demand for housing stock should encourage construction activity. Data out this week showed housing starts and permits rose 0.3% and 0.4% m/m respectively, driven in large part by a pick-up in multi-family. While the single-family data showed some signs of cooling, the levels of activity remain strong relative to post-GFC trends.

Altogether, while surging mortgage rates and soaring property values are making homes less affordable, housing affordability remains elevated suggesting that residential investment is unlikely to collapse this year.

From a markets standpoint, it’s unsurprising that the move higher in mortgage rates, material costs and wages have pressured U.S. homebuilder profitability and market performance. Homebuilder stocks are down 25% this year, underperforming the S&P 500 by 19%. That said, given the constructive fundamental outlook and the sectors’ attractive valuation, now may be an attractive buying opportunity.

U.S. housing prices

January 1953 indexed to 100

Related: Has the Sell-off Created an Opportunity in Growth Stocks?

Source: Robert Shiller, Yale University, BLS, Standard & Poor's, J.P. Morgan Asset Management.