Trending

Written by: Sandra Rhouma

As expected, the European Central Bank (ECB) raised its three key interest rates by 25 basis points (bps) on June 11, responding to the energy shock from the Iran war. Inflation was revised higher for 2026 and 2027, and it is expected to fall to target in 2028. Although we expect one more hike, the timing is uncertain as the ECB is keeping all options open—including the possibility of not raising rates again.

Should the ECB pause in July and a resolution to the conflict is reached, we think it would be harder to justify further rate hikes. In any case, two hikes seem consistent with the ECB’s price-stability mandate and would be easy to reverse swiftly once inflation normalizes.

The Euro Area Economy Has Weakened

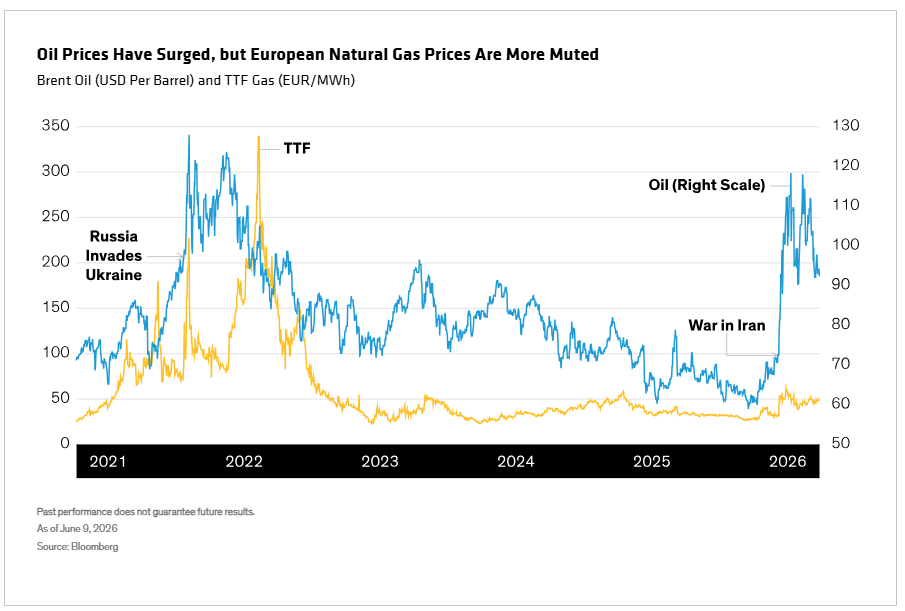

While there’s a chance of further hikes beyond our forecast, we think more policy tightening could be risky given the current macro environment. Today’s euro-area economy is weaker than in February 2022—when Russia’s invasion of Ukraine triggered the last energy shock—and wage growth and job vacancies have been trending down (Display). Euro-area inflation was undershooting the target before the Iran war started, in contrast to the 5.6% inflation rate that prevailed before the Ukraine invasion.

While European natural gas prices have risen substantially, they’re still materially cheaper than during the Ukraine crisis period (Display), and medium-term inflation expectations have remained anchored so far. That’s an important gauge of both the ECB’s credibility and the absence of severe second-round inflationary effects at this stage.

In addition, considering euro-area governments’ stretched finances, fiscal support will likely be limited both in size and duration, and therefore unlikely to stoke inflation. All these factors put the current inflationary environment in context (Display), arguing for a smaller hiking cycle, in our view.

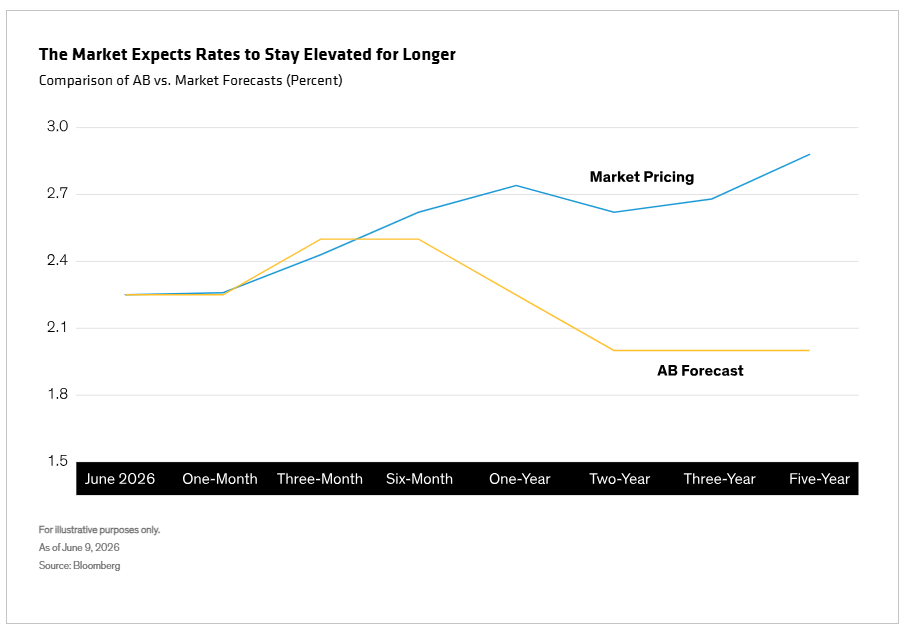

Consequently, we think euro policy rates will need to be cut back to neutral in 2027, or lower if the euro-area economy continues to underperform while inflation normalizes.

By contrast, the market is pricing a rising interest-rate trajectory, with euro rates a full 60 bps higher in five years’ time (Display). But we don’t believe the region’s economy can withstand even moderately restrictive rates for an extended period, and we don’t think this inflationary shock requires them.

The ECB’s rate hikes could prove counterproductive, considering the fragility of the euro-area economy and the expected limited pass-through effects from higher energy prices. But unless the Iran war takes a turn for the worse, if the market’s expectations for rate hikes play out, it could be even more counterproductive.

Related: AI Boom Is Reshaping Markets and Reviving Value Investing