Trending

Written by: Gregg S. Fisher | Quent Capital

For most of my 33-year career as an investor and analyst, the world has operated under a relatively stable set of assumptions:

-

That goods, capital, and trade would continue flowing relatively freely across borders

-

That multilateral instutions and alliances would constrain raw power

-

That the United States would remain the central force in the global economic order

-

That transatlantic alliances and geopolitical relationships were stable and dependable

-

That rising and widely shared prosperity would keep the system more or less stable

This “rules-based” world was one in which we broadly understood the rules of the system, trusted the institutions underneath it, and believed the major powers had a shared interest in keeping the global order relatively stable.

The outcomes of this system were overwhelmingly good: massive growth in emerging countries, particularly China and India; economic stability (until the global financial crisis) in developed ones; and no major wars. I did not think the rules-based order would show clear signs of disintegrating in the wake of so much success.

The assumptions investors relied on for decades are now being challenged and reimagined in real time.

I call this change the Great Reimagination: a time when the political, economic, and technological assumptions we took for granted are being rewritten in real time.

In this three-part series, I’ll share how I am thinking about this changing world, and how those views inform my investment thinking and where I look for opportunity. We are shifting from a rules-based global order to a more power-based world, and that has direct implications for how we invest. In this new environment, it is more important to prepare for many possible futures than to bet on any single geopolitical outcome. Applying these observations to portfolio management, several themes emerge: real assets, security and infrastructure, and strategic geographical diversification.

In Part 1, I’ll explore the shift from a rules-based world to a more power-based one and the implications for geopolitics, alliances, and global markets. In Part 2, I turn to the capital markets and look at concentration, investor behavior, and the end of “magical thinking” after fifteen years of extraordinary market performance. In Part 3, I’ll turn to fractured globalization, the changing role of the dollar, and why real assets, infrastructure, and geographic diversification may matter more in the years ahead.

When Power Matters More Than Rules

Geopolitically, the world is no longer organized around a single, unrivaled center of gravity. The United States is still the largest and most important economy, but we now have a counterweight in China that we didn’t before. The European Union is a major economic bloc, but it does not act like a single geopolitical power the way a sovereign nation does. It is also in a period of decline that does not have an obvious endpoint.

At the same time, traditional alliances no longer feel as certain as they once did. Think about how different the transatlantic relationship looks when one NATO member openly talks about invading another’s territory, even half-jokingly, or when Europe hesitates to back U.S. actions in the Middle East. These are not small changes. They are signs that the old rules of the post-World War II order are under pressure.

The ancient Greeks gave us language for moments when power starts to matter more than rules. In Plato’s Republic, Thrasymachus defines justice as “nothing but the advantage of the stronger.” Thucydides, the Greek historian who chronicled the war between Athens and Sparta, put a similar idea more bluntly: “The strong do what they will, and the weak suffer what they must.” In a recent meeting with President Trump, Xi Jinping invoked the “Thucydides Trap,” a warning about the tension between a rising power and an established one.

For a while, we convinced ourselves the global system was different, and to some extent that expectation was realistic. Institutions like the UN and WTO, and alliances like NATO, appeared able to constrain raw power. That was the promise of a “rules-based order.” The Soviet Union did not follow the rules, but that union was dissolved 35 years ago and violations of the rules-based order were rare for a long time.

Increasingly, however, the global system seems to be moving away from a rules-based order and toward a power-based one. You can see this shift in the examples playing out around the world:

-

In trade, where the United States put broad tariffs on trading partners in ways that stretched legal authority and shocked long-standing allies.

-

In the Middle East, where Iran has used swarms of cheap drones to threaten multi-billion-dollar weapons systems and vital shipping lanes, showing how quickly technology can change the balance of power.

-

In Ukraine, where Russia’s war has turned into a grinding stalemate rather than the clear-cut victory or defeat many expected at the outset.

-

And finally, in countries charting a more independent course: India, Saudi Arabia, Brazil, and others are testing how far they can go without fully siding with any one bloc. Brazil has always gone its own way, but after the fall of the Soviet bloc, India cast its lot pretty definitively with the West, and that tie is fraying although not gone.

That brings us to alliances. A phrase I heard recently from my friend and collaborator Rawi Abdelal really stuck with me: “dead body friends.” Even if you’ve never heard the phrase, instinctively we all know what that means. The person you can call at two in the morning who shows up first and asks questions later. There’s a great scene in the film “The Town” where Ben Affleck says to his friend: “I need your help. I can’t tell you what it is. You can never ask me about it later. And we’re gonna hurt some people.” His friend pauses and says, “Whose car are we gonna take?”

That’s a dead‑body friend. Someone who will help you even if the help involves disposing of a dead body.

Alliances work the same way. In a more power-based world, the question becomes: Whom can you really count on? And who can count on you? For decades, the United States could count on a small circle of countries to act as dead-body friends. Today, there are fewer of those relationships. Europe is more cautious. Some partners in the Middle East hedge between Washington and Beijing. This erosion of deep, unquestioning trust makes crises messier and more unpredictable.

So what does all of this mean for portfolios?

Investing Across Many Possible Futures

Investing through the Great Reimagination is not about making one giant geopolitical bet. It is about thinking in probabilities and investing thematically.

Geopolitics can’t be treated as vague background noise. When the world’s largest consumer market suddenly slaps 20% tariffs on a key partner (after imposing even higher tariffs but then backing off), or when a regional conflict threatens a chokepoint like the Strait of Hormuz, those events flow directly into earnings, supply chains, energy prices, and ultimately asset values.

Traditional diversification still has a role. Owning stocks, bonds, and maintaining some international exposure remains important. But in a more power-based world, those actions may not be enough. We now have to think about diversification across political regimes and economic systems.

In practice, I don’t know when the next major geopolitical shock will happen, or where. My team and I focus on building portfolios that can live through a range of plausible futures.

One future may involve a long-running cold war between the U.S. and China. Another may bring regional flare-ups that periodically disrupt trade routes and energy markets. A third may bring relative calm, but continued competition in areas like space, computing, and advanced manufacturing. Our job is to stress-test portfolios against those kinds of scenarios, not just against historical averages.

That’s one reason we’ve leaned into themes tied to security, defense, and critical infrastructure. When countries feel less secure, they tend to spend more on defending themselves and hardening their systems. You can see this in rising defense budgets, the rush to secure undersea cables and satellites, and renewed focus on shipbuilding, missile defense, and drone technology.

We are not trying to pick the next hot weapons stock. We want to own high-quality businesses that supply components and services essential for undertakings that will continue for a long time. Among these are companies that build the ships, design the sensors, maintain the networks, supply the raw materials, and keep systems online. They tend to have strong competitive positions, long-term contracts, and cash flows that are less tied to the economic cycle than most.

We also place greater emphasis on real assets and strategically important infrastructure. In a more power-based world, control over energy, minerals, communication networks, and space infrastructure becomes even more valuable. That leads us to invest in energy producers and pipeline operators in relatively stable jurisdictions, in companies that own or service critical communications and data infrastructure, and in firms involved in areas such as space launch, satellite constellations, and geospatial data.

A simple example: when a single undersea cable outage can disrupt internet traffic for an entire region, the businesses that build redundancy and security into that system become indispensable.

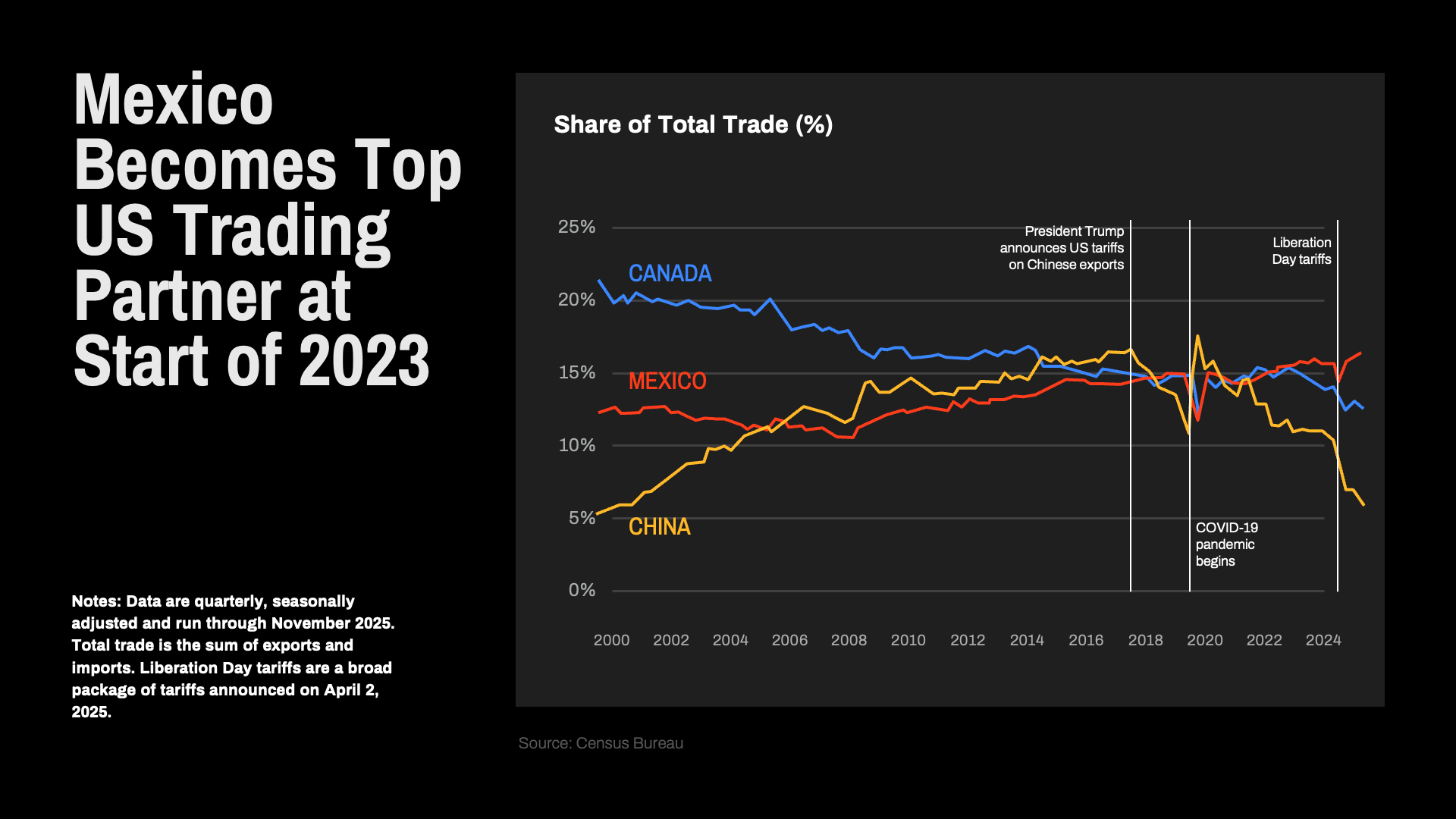

Geography matters too, but not in the simplistic sense of “U.S. good, international risky.” We still see tremendous value in U.S. markets, but we also recognize that other regions are stepping into more central roles and reduce some of the risks associated with U.S.-focused investing. Mexico has become America’s largest trading partner1 and a natural beneficiary of near-shoring. Canada plays an outsize role in energy, aerospace, and now space. Parts of Latin America and Southeast Asia are winning new investment as companies diversify away from single-country dependence in their supply chains.

When we invest internationally, we try to understand each country’s position in this evolving power map. Who are its friends? How durable are those friendships? How stable are its institutions? What leverage does it have? Where does it sit as trade, energy, technology, and security relationships are being redrawn?

That is what investing through the Great Reimagination requires. We have to update our thinking and our portfolios: embracing scenario analysis, understanding very complex supply chains that begin with minerals in the ground and end with finished products, leaning into resilient themes like security and infrastructure, and diversifying across geographies, regimes, and sources of risk.

Ultimately, it means building portfolios with more than one version of the future in mind. Or as I say: Think in probabilities.

In Part II of this series, I’ll turn from geopolitics to markets. For the last decade and a half, U.S. stocks have delivered extraordinary returns, and a small group of mega-cap companies has dominated the story. I think that has encouraged a kind of magical thinking, and I believe that era is coming to an end. I’ll share what that might mean for investors, and how we’re positioning portfolios for a more normal, but potentially more volatile, future.

Related: RIAs Don't Need More Vendors. They Need Better Priorities.

Endnotes

1 Source: World Bank, current USD, nominal (2024).