Trending

“QE” or “Quantitative Easing” has been the bull’s “siren song” of the last decade, but will “Not QE” be the same?

Last week, amid a rash of bank insolvencies, government agencies took action to stem a potential banking crisis. The FDIC, the Treasury, and the Fed issued a Bank Term Lending Program with a $25 billion loan backstop to protect uninsured depositors from the Silicon Valley Bank failure. An orchestrated $30 billion uninsured deposit by eleven major banks into First Republic Bank followed. I suggest those deposits would not occur without Federal Reserve and Treasury assurances.

The details of the Bank Term Funding Program (BTFP) were described in the press release by the Federal Reserve. To wit:

“The additional funding will be made available through the creation of a new Bank Term Funding Program (BTFP), offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution’s need to quickly sell those securities in times of stress.

With approval of the Treasury Secretary, the Department of the Treasury will make available up to $25 billion from the Exchange Stabilization Fund as a backstop for the BTFP. The Federal Reserve does not anticipate that it will be necessary to draw on these backstop funds.”

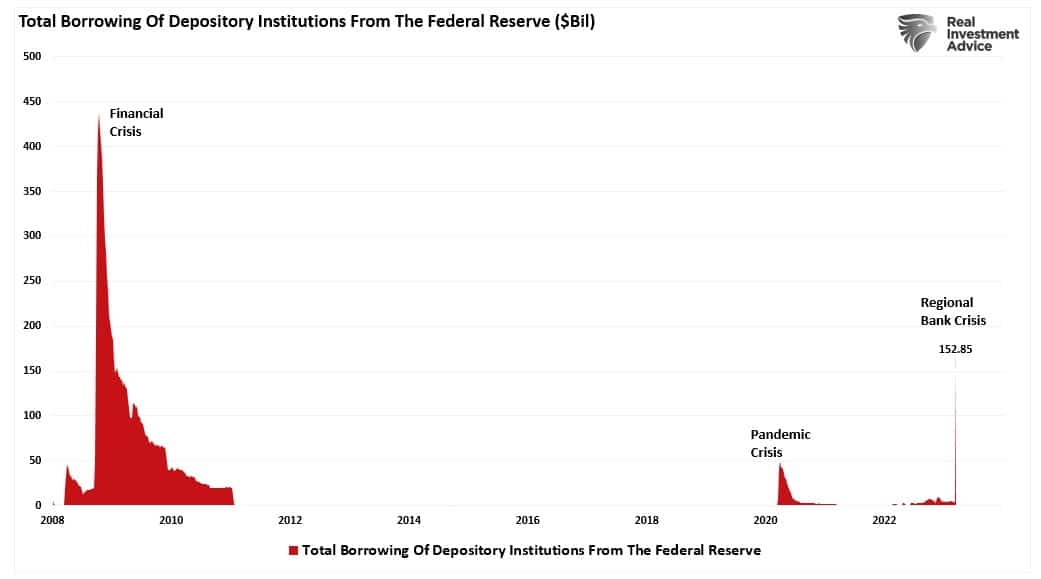

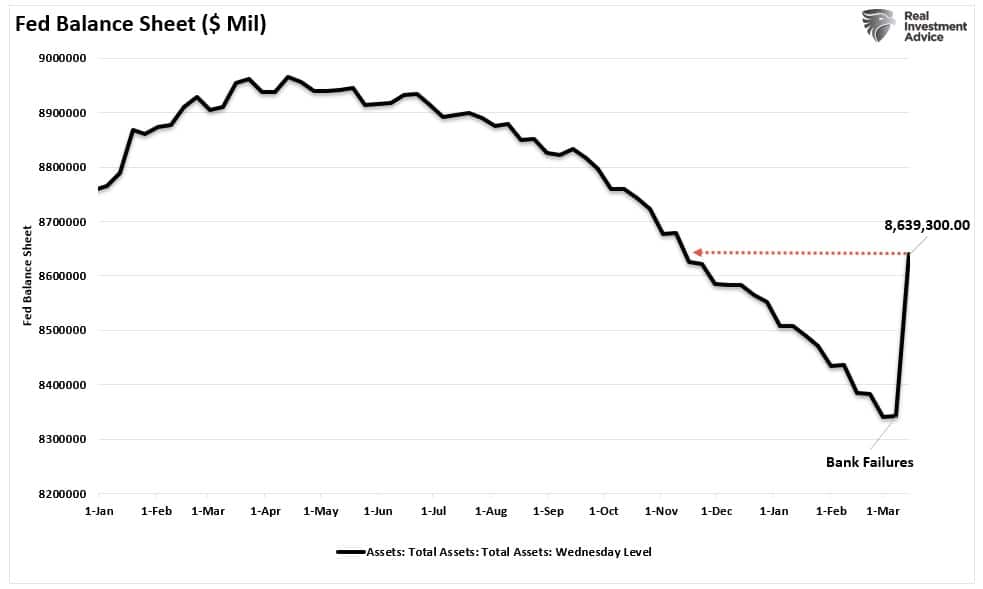

Banks quickly tapped the program, as shown by the $152 billion surge in borrowings from the Federal Reserve. It is the most significant borrowing in one week since the depths of the Financial Crisis.

The importance of this program is that, as noted by Bloomberg, it will inject up to $2 Trillion into the financial system.

“‘The usage of the Fed’s Bank Term Funding Program is likely to be big,’ strategists led by Nikolaos Panigirtzoglou in London wrote in a client note Wednesday. While the largest banks are unlikely to tap the program, the maximum usage envisaged for the facility is close to $2 trillion, which is the par amount of bonds held by US banks outside the five biggest, they said.”

As Bloomberg notes, major banks like JP Morgan likely will not tap the Feds lending program due to the stigma often attached to such usage. Moreover, there are roughly $3 Trillion in reserves in the U.S. banking system, of which the top-5 major banks hold a significant portion. However, as I noted last week in “Bank Runs:”

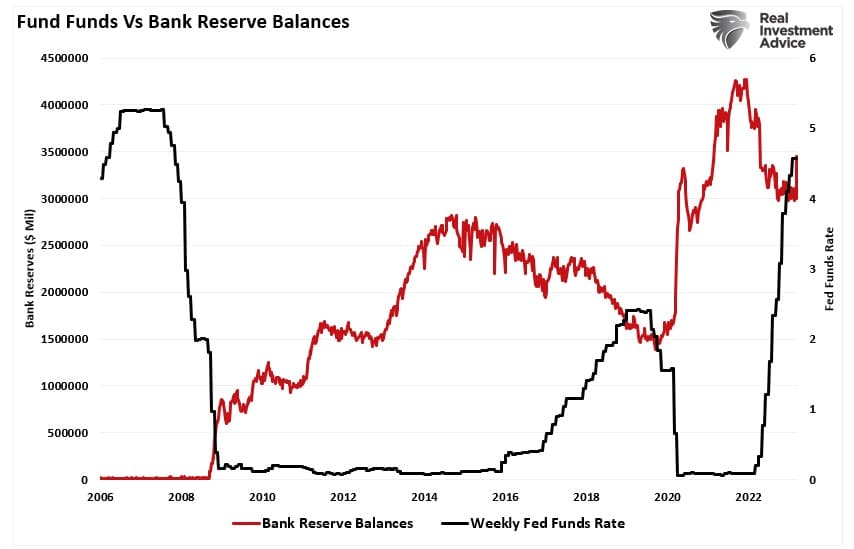

“The Fed caused this problem by aggressively hiking rates which dropped collateral values. Such has left some banks which didn’t hedge their loan/bond portfolios with insufficient collateral to cover the deposits during a ‘bank run.'”

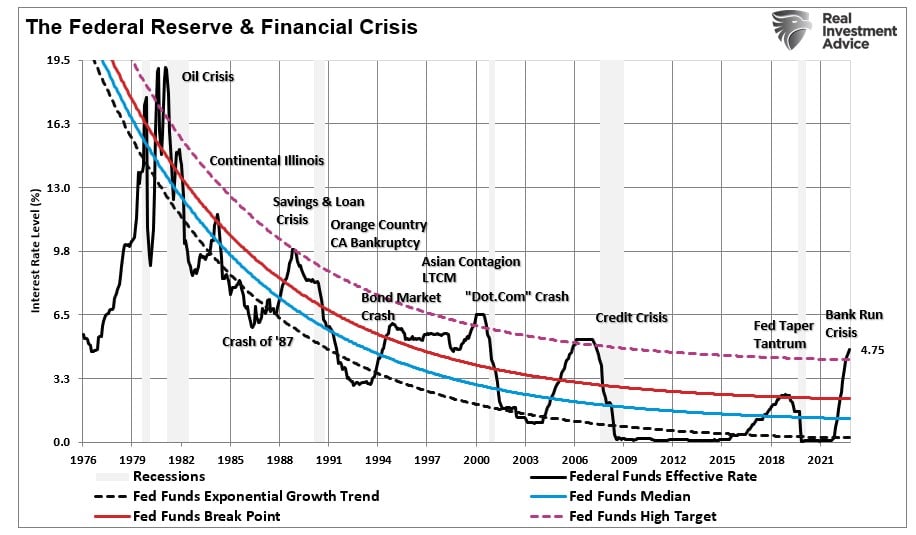

As shown, the rapid increase in rates by the Fed drained bank reserves.

The demand by banks for liquidity has now put the Federal Reserve between a “rock and a hard place.” While the Fed remains adamant in its inflation fight, the BTFP may be the next “QE” program disguised as “Not QE.”

Investor Conditioning

Classical conditioning (also known as Pavlovian or respondent conditioning) refers to a learning procedure in which a potent stimulus (e.g., food) becomes paired with a previously neutral stimulus (e.g., a bell). Pavlov discovered that when he introduced the neutral stimulus, the dogs would begin to salivate in anticipation of the potent stimulus, even though it was not currently present. This learning process results from the psychological “pairing” of the stimuli.

This conditioning is what happened to investors over the last decade.

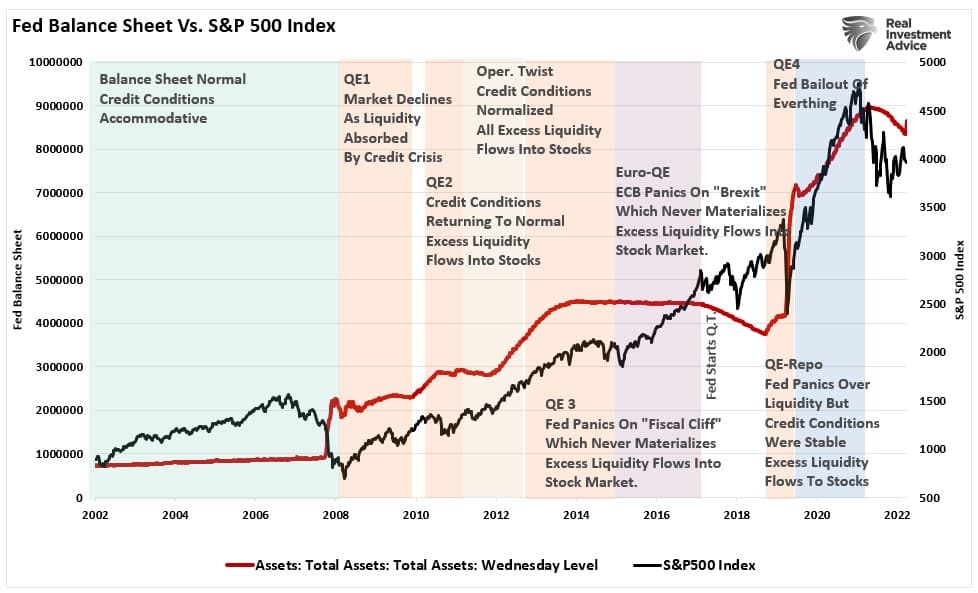

In 2010, then Fed Chairman Ben Bernanke introduced the “neutral stimulus” to the financial markets by adding a “third mandate” to the Fed’s responsibilities – the creation of the “wealth effect.”

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose, and long-term interest rates fell when investors began to anticipate this additional action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion.”

– Ben Bernanke, Washington Post Op-Ed, November, 2010.

Importantly, for conditioning to work, the “neutral stimulus,” when introduced, must get followed by the “potent stimulus” for the “pairing” to complete. For investors, as the Fed introduced each round of “Quantitative Easing,” the “neutral stimulus,” the stock market rose, the “potent stimulus.”

As shown, asset prices rose as the Fed expanded its balance sheet.

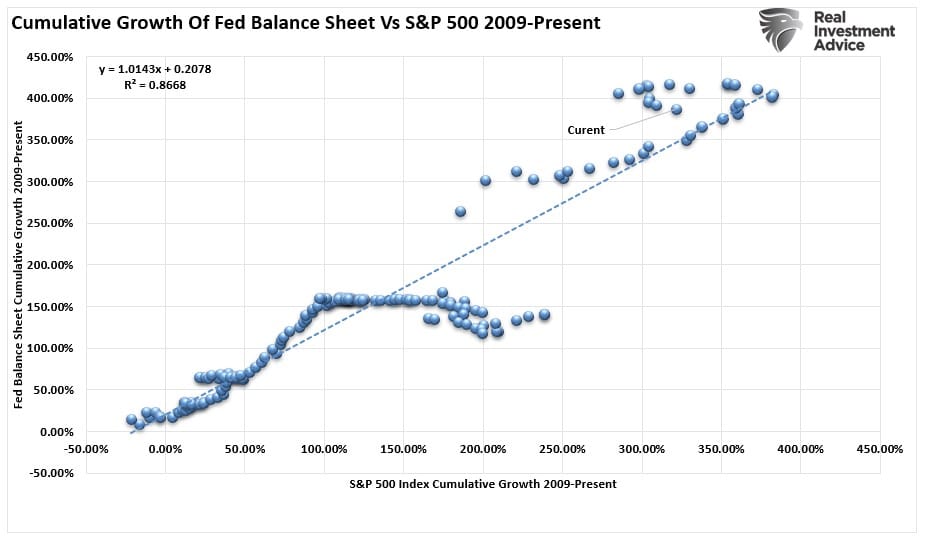

While many suggest that the Fed’s QE programs have no impact on the financial market, the near 87% correlation between balance sheet changes and the market would imply otherwise.

Such is why investors cling to each Fed meeting in anticipation of the “ringing of the bell.”

In Pavlovian terms, the “pairing is complete.”

BTFP Is Not QE

While the BTFP facility is technically “Not QE,” it does reverse the Fed’s efforts to reduce financial liquidity. As shown below, the Fed’s balance sheet surged since last week, reversing more than six months of previous tightening.

This reversal of liquidity is not surprising given the recent rout in the banking sector.

J.P. Morgan noted on Friday that U.S. banks lost nearly $550 billion in deposits last week. Investors, in a panic, were transferring funds to major banks from regional banks, which put further stress on already discounted collateral due to the Fed’s rate hiking campaign.

“The big picture from the H.4.1 release is that the U.S. banking system induced the Fed to expand its balance sheet and inject $440bn of reserves in just one week. That large liquidity injection reverses a third of the previous $1.3tr of reserve tightening since the end of 2021. Given such a backdrop of elevated banking system liquidity or reserve needs, this naturally raises the question of whether the Fed can continue QT, similar to 2018/2019.“

This is NOT QE, as no NEW money was created. The banks’ eligible assets collateralize these loans under the Discount Window facility. The Fed is not purchasing the collateral. Once the loans are repaid, the collateral gets returned to the banks, and the Fed’s balance sheet will shrink again.

However, as noted above, this is the “ringing of the bell” by the Fed. But more notably, as repeatedly discussed, it was only a matter of time before the Fed “broke something.”

“The economy and the markets (due to the current momentum) can DEFY the laws of financial gravity as interest rates rise. However, as interest rates increase, they act as a “brake” on economic activity. Such is because higher rates NEGATIVELY impact a highly levered economy.”

History is pretty clear about the outcome of rate hiking campaigns.

Over the weekend, the Fed opened “dollar swap lines” after the UBS/Credit Suisse takeover. Historically, once the Fed resorts to reopening dollar swap lines, the rest of the programs follow, from rate cuts to the “real” QE and other monetary supports.

The Fed Created This

As noted in this past weekend’s newsletter, the Fed must choose between fighting “inflation” or again bailing out the financial system in the name of “financial stability.”

Of course, this entire situation is entirely due to the Federal Reserve.

In October 2020, I wrote an article arguing that Neel Kashkari was wrong and the Fed was indeed creating a “moral hazard” by injecting massive stimulus into the economy following the pandemic. The literal definition of “moral hazard” is:

“The lack of incentive to guard against risk where one is protected from its consequences, e.g., by insurance.“

Unsurprisingly, zero interest rates, $5 trillion in fiscal policy to households, and $120 billion in monthly “QE” removed all “risk” from owning “risk assets.” The resultant spike in inflation and speculative risk-taking was the result.

However, the “lack of incentive to guard against risk” becomes problematic when monetary, fiscal, and zero-interest-rate policies are reversed.

Yes, this is all the Fed’s doing.

However, since the turn of the century, the Fed has been able to repeatedly support financial markets by dropping interest rates and providing monetary accommodation. Such was because inflation remained at low levels as deflationary pressures presided.

With inflation running at the highest levels since the 80s, the Fed risks creating another inflationary and interest rate spike if they focus on financial stability. However, if they focus on inflation and continue hiking rates, the risk of a further crack in financial stability increases.

I don’t know which path the Fed will choose, but there seems to be little upside to the markets. The “moral hazard” the Fed created in the first place has now come home to roost.

Related: Consensus View of “No Recession.” Could It Be Wrong?