Trending

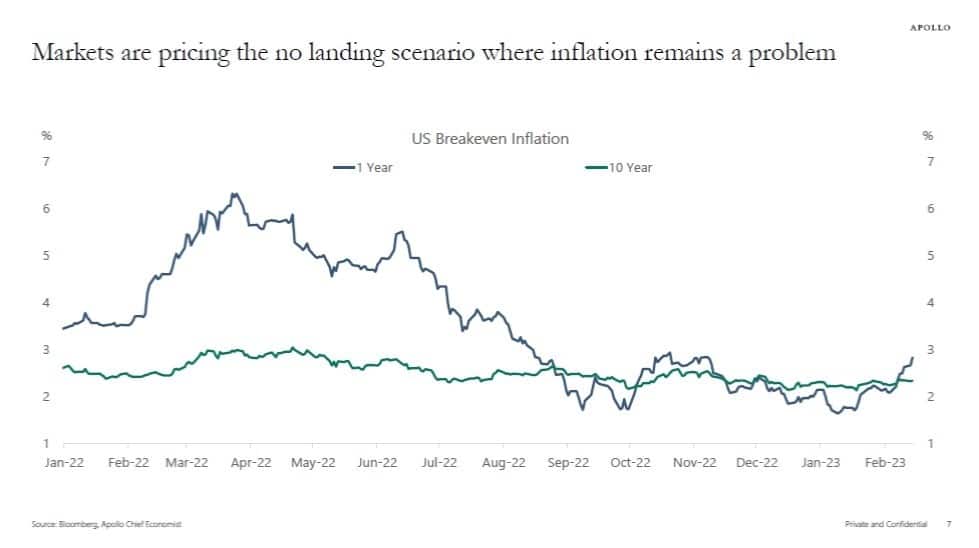

Economically speaking, bullish bets are mounting on a “no landing” scenario, which suggests the economy will avoid a recession entirely. As noted by Yahoo Finance last Friday:

“The newly-coined ‘no landing’ outcome considers a scenario in which inflation doesn’t actually cool while economic growth continues, even as interest rates remain elevated amid the Federal Reserve’s attempts to tamp prices down.

In other words, the market is saying that inflation will be significantly higher in a year’s time than the Fed’s 2% inflation target. Put differently, instead of expecting a recession and lower inflation, short-term inflation expectations are rising and becoming unanchored.“

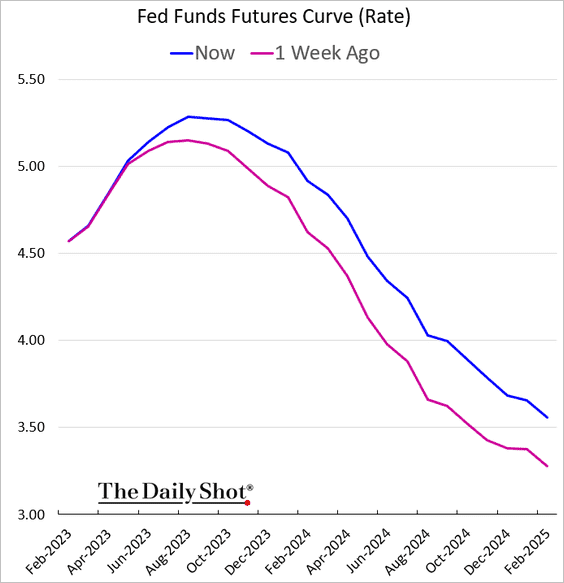

One sign the markets are pricing in the “no landing” scenario is the disconnect between the Fed and the market. The Fed funds futures show the market expects rate cuts to start by mid-year even though the terminal rate has shifted higher.

However, here is the problem with the “no landing” scenario.

What would cause the Fed to cut rates?

- If the market advance continues and the economy avoids recession, there is no need for the Fed to reduce rates.

- More importantly, there is also no reason for the Fed to stop reducing liquidity via its balance sheet.

- Also, a “no-landing” scenario gives Congress no reason to provide fiscal support providing no boost to the money supply.

See the problem with this idea of a “no landing” scenario?

“No landing does not make any sense because it essentially means the economy continues to expand, and it’s part of an ongoing business cycle, and it’s not an event. It’s just ongoing growth. Doesn’t that entail that the Fed will have to raise rates more, and doesn’t that increase the risk of a hard landing?” – Chief Economist Gregory Daco, EY

That last sentence is most notable.

The Fed Isn’t Done Fighting

Fed Funds futures are now pricing in a 21% chance the Fed will hike rates by 0.50% at the March meeting. While the odds are still relatively small, consider that two weeks ago, the odds were near zero. In January, many analysts suggested the February FOMC meeting would be the last rate hike for this cycle.

Given the recent spate of economic data from the strong jobs report in January, a 0.5% increase in inflation and a solid retail sales report continue to give the Fed no reason to pause anytime soon. The current base case is that the Fed moves another 0.75%, with the terminal rate at 5.25%.

That view was supported by Fed Presidents Loretta Mester and Jim Bullard last week.

- FED’S BULLARD: I WOULDN’T RULE OUT SUPPORTING 50-BP MARCH HIKE.

- FED’S BULLARD: THE FED RISKS A REPLAY OF THE 1970S IF IT CAN’T LOWER INFLATION SOON.

- FED’S BULLARD: AT THIS POINT, I SEE THE POLICY RATE IN THE RANGE OF 5.25% TO 5.5% AS APPROPRIATE.

- FED’S MESTER: THE RETURN TO PRICE STABILITY WILL BE PAINFUL.

- “It’s not always going to be, you know, 25 [basis points],” said Cleveland Fed President Loretta Mester

- “As we showed, when the economy calls for it, we can move faster. And we can do bigger increases at any particular meeting.”

As Mr. Daco noted, the type of rhetoric doesn’t suggest a “no landing” scenario, nor does it mean the Fed will be cutting rates soon.

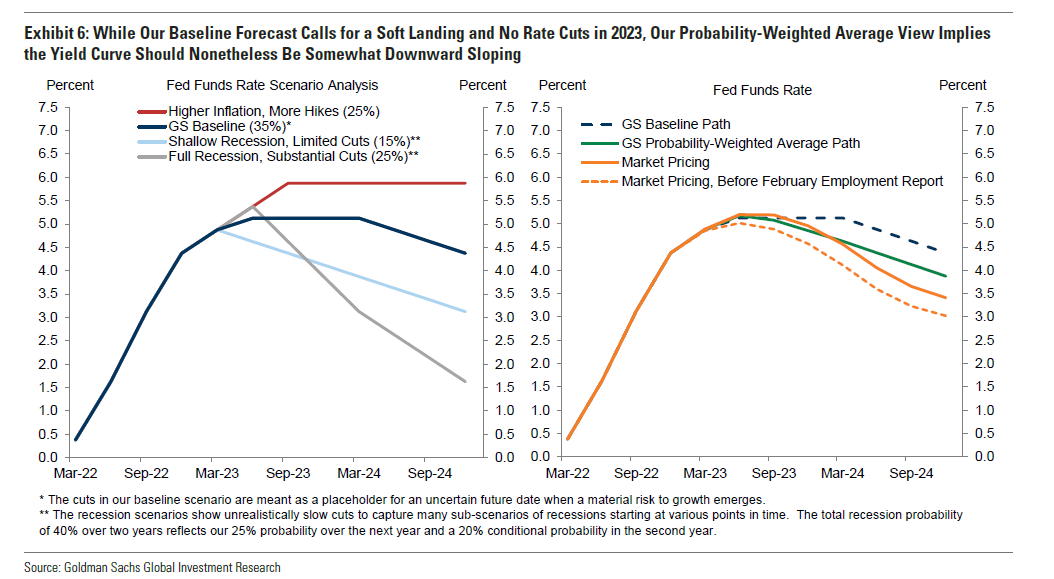

The only reason for rate cuts is a recession or financial event that requires monetary policy to offset rising risks. This is shown in the chart below, where rate reductions occur as a recession sets in.

Of course, the risk of the “no landing” scenario is that it is based on lagging economic data. The problem with that data is that the lag effect of monetary tightening has not been reflected as of yet. Over the next several months, the data will begin to fully reflect the impact of higher interest rates on a debt-laden economy.

More importantly, as Loretta Meister stated last week, to get inflation under control, the “no landing” scenario is not an option. In reality, “the return to price stability will be painful.”

Economic Data Is Weakening

As discussed in this past weekend’s newsletter, mainstream analysis focuses on the monthly economic data points. These myopic observations often overlook the larger picture. As with investing in economic data, the “trend is your friend.”

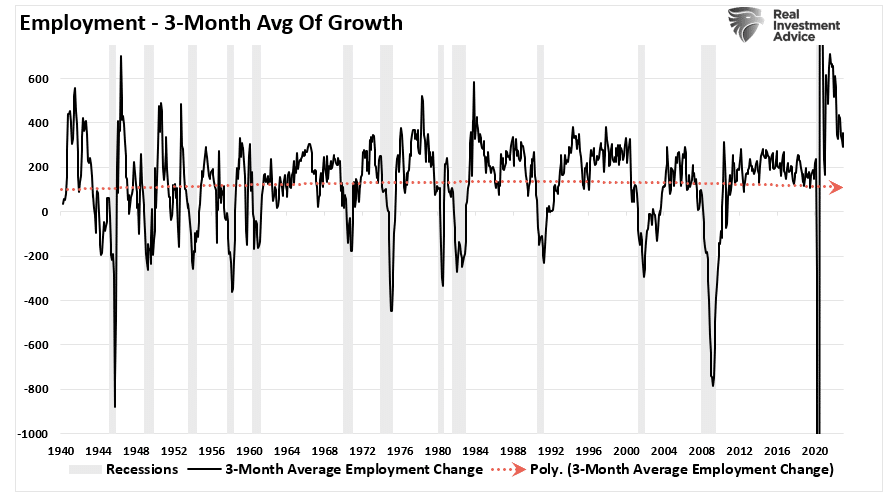

“For example, that strong employment report in January certainly gives the Fed plenty of reasons to continue tightening monetary policy. If its goal is to reduce inflation by slowing economic demand, job growth must reverse. However, if we look at employment growth, it is indeed slowing. As shown, the 3-month average of employment growth has turned lower. While employment is still gaining, the trend suggests that employment growth will likely turn negative over the next several months.”

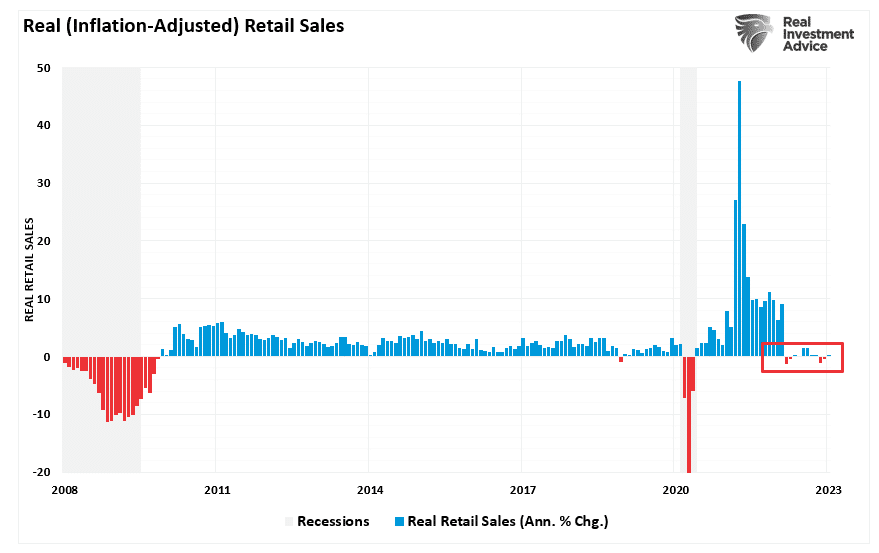

“Retail sales data for January is also showing deterioration. This past week, retail sales showed a 3% monthly increase in January, the most significant jump since March of 2021 when Biden’s stimulus checks hit households. However, this is all on a nominal basis. In other words, even though consumers didn’t have a “stimmy check” to boost spending, they “spent more to buy less” stuff on an inflation-adjusted basis. Over the last 11 months, as the stimulus money ran out, real retail sales have flatlined.”

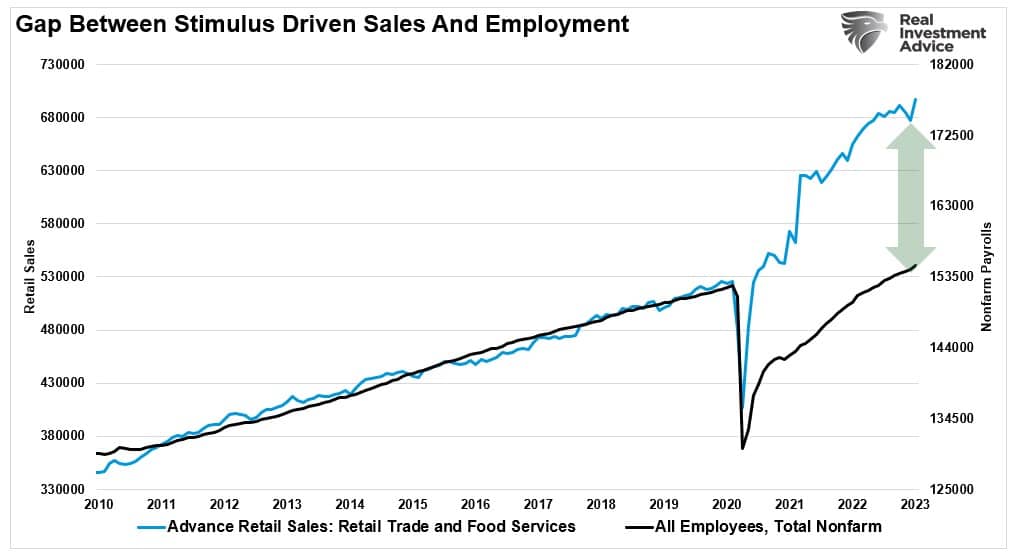

“While most of the jobs recovery was hiring back employees that were let go, the surge in stimulus-fueled retail sales will ultimately revert to employment growth. The reason is that people can ultimately only spend what they earn. As shown, the disconnect between retail sales and employment is unsustainable.”

The eventual reversion of the data to economic normality will ultimately result in something vastly different than a “no landing” scenario.

We think the bulls are misreading the “tea leaves” once again.

The current “no landing” scenario doesn’t make sense and is at odds with the Fed’s goal of combatting inflation pressures. That outcome is likely not bullish for equities over this year.

The bulls are correct that the Fed will eventually cut rates. However, they will be doing so to offset the impact of a recessionary drag. Such does not equate to higher equity prices, as markets must adjust for lower earnings.

Be careful of the narrative you pick.

There is the “no landing” scenario, and then there is reality.

Related: Recession Signal as Consumers Struggle To Pay Bills