Trending

Buying stocks is always hard. Particularly during corrections. Or, near market peaks. Or, when stocks are falling. And when they are rising. Oh, buying stocks is also tricky when valuations are high. And when they are low. You get the point. There is never the right time when it comes to buying stocks.

I recently read Ted Seides’s excellent post, “The Hardest Day To Invest Is Always Today.” As Ted notes, there is always a reason NOT to invest in the financial markets.

“Today is no exception. We face heightened uncertainty from tariffs, economic conditions, valuations, private market liquidity, and crowding in alternatives. Even leading macro strategists have begun to question the durability of U.S. exceptionalism. When stocks, bonds, and alternatives appear unattractive, what’s an investor to do?”

I agree. When buying stocks, we can always rationalize why we shouldn’t. Notably, the reasoning is always sound and logical. Such is particularly true if you consistently follow an “echo chamber of negativity” on the many podcasts, blogs, and mainstream media that use fear to generate views and clicks.

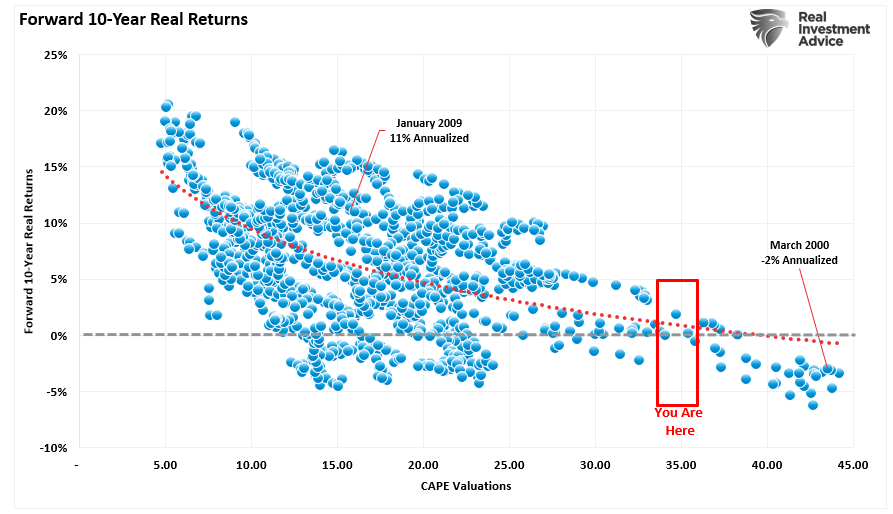

For example, many investors have argued that lofty valuations will impair forward returns. The data supports that claim.

However, valuations have permanently increased over the last 25 years due to massive fiscal and monetary interventions from Global Central Banks and Governments.

“There are many reasons why valuations have shifted higher over the years. The increase is partly due to economic expansion, globalization, and increased profitability. However, since the turn of the century, changes in accounting rules, share buybacks, and greater public adoption of investing (aka ETFs) have also contributed to the shift. Furthermore, as noted above, the massive monetary and fiscal interventions since the “Financial Crisis” created a seemingly “risk-free” environment for equity risk.”

The chart shows the apparent shift in valuations.

- The “median” CAPE ratio is 15.04 times earnings from 1871 to 1980.

- The long-term “median” CAPE is 16.52 times earnings from 1871-Present (all years)

- The “median” CAPE is 23.70 times earnings from 1980 to the present.

However, despite those “high valuations,” The chart shows the average annual inflation-adjusted total returns (dividends included) since 1928. I used the total return data from Aswath Damodaran, a Stern School of Business professor at New York University. The chart shows that from 1928 to 2023, the market returned 8.45% after inflation. However, after the financial crisis of 2008, returns jumped by nearly four percentage points for the various periods. In other words, stocks have had their highest annual return rates during high valuations.

The latest reason “not to buy stocks” is Ray Dalio’s latest warning that the U.S. will face a debt crisis. That is a worrisome headline, but as noted in that article, if investors had listened to Ray Dalio’s first warning in 2010, they would be far worse off today.

Yes, there are always good reasons NOT to buy stocks. But as investors, worrying about what “might happen” has cost them far more money than being invested during periods of what “did” happen.

Does that mean we should not try to mitigate investment risk at all? Of course, not.

Buying Stocks When You Don’t Want To

As stated, there is always a reason NOT to buy stocks. However, in most cases, those are the times when we should navigate our emotional biases. Here are two recent examples of navigating the market.

March 11th – A Topping Process In Progress

“As of early March 2025, several key indicators—the NYSE Advance-Decline (A/D) Line, Relative Strength Index (RSI), and Moving Average Convergence Divergence (MACD)—are signaling caution, suggesting that investors should take a closer look at their risk management strategies. Given these warning signs, investors should proactively manage risk and protect their portfolios.”

In that article, we recommended that investors tighten up stop loss levels, hedge portfolios against a decline, take profits, and rebalance allocations (or buy more defensive stocks). We didn’t say, “sell everything and go to cash.” Most importantly, we concluded that article by stating:

“However, even during bearish trending markets, opportunities will be presented for significant rallies and eventual market lows if such should occur. Therefore, given the proper market set-up, investors should have positions ready to execute accordingly. In this case, we are looking for positions that have either a “value” tilt or have pulled back to support and provide a lower-risk entry opportunity.”

In other words, investors should be willing to buy stocks during the decline, which is typically the point that investors don’t want to.

Of course, the decline did come in April. Concerns over tariffs, a trade war, and rising interest rates were all excellent reasons for investors not to buy stocks. However, we then suggested the opportunity to buy stocks had arrived.

April 6th – The Hope In The Fear

“Whether or not the current market crash is the beginning of a larger corrective cycle, such low readings have, without failure, marked the near-term low of a market correction. While the market has previously continued its corrective process after such low readings, such did not occur without a meaningful reversal rally first.”

As we concluded in that article:

“It won’t take much for the market to find a reason to rally. That could happen as soon as next week. If the market rallies, we suggest reverting to the basic principles to navigate what we suspect will be more volatile this year. However, at some point, just as we saw in 2022, the market will bottom. Like then, you won’t want to believe the market is bottoming; your fear of buying will be overwhelming, but that will be the point you must step in.

Buying near market lows is incredibly difficult. While we likely aren’t there yet, we will be there sooner than you imagine. As such, when you want to “sell everything,” ask yourself if this is the point where you should “buy” instead.“

As is always the case, bearish headlines, concerns beyond our control, and the fear of loss lead us not to buy stocks exactly when we should.

The Best Thing You Can Do For Your Investing

The most significant problem investors face is the barrage of negative headlines, media spins, and “cherry-picked” data points that make very logical cases against buying stocks. However, while there are certainly past instances, like the market crashes of 1929, 1974, 2000, and 2008, these rare events were some of the best buying opportunities of generations. However, it is easy to worry today about the potential for significant losses when looking back at history.

So, what is the best thing you can do for your investing?

Turn it all off.

- The podcasts

- The financial news

- The political news

- Most importantly, your computer.

Yes, turn it off.

Regardless of who they are, no one in the financial media knows what the future will bring. The bears will be bears and will be wrong most of the time. The bulls will be bulls and will be wrong at the worst possible time. They bring nothing valuable to your investing process.

Viewing your portfolio minute by minute makes you treat your investments like a casino. You lose focus on the fundamental underpinnings that drive long-term returns. Most of the time, price declines in fundamentally strong companies are buying opportunities. Still, investors tend to sell them due to headline-driven narratives that are short-term in nature.

Instead, focus on what does work in the long-term investing and wealth-building process.

10 Investing Rules for Navigating Volatile Markets

- Invest Even When It Feels Hard

- There will never be a “perfect” time to buy stocks. Market peaks, corrections, and high or low valuations are all intimidating, but disciplined investing during uncomfortable times often leads to strong long-term returns.

- Manage Risk, Don’t Flee

- Instead of selling everything during market declines, tighten stop-loss levels, hedge portfolios, rebalance allocations, or rotate into defensive sectors. Reducing risk does not mean abandoning the market.

- Be Prepared to Buy on Fear

- Significant declines often coincide with the worst headlines and deepest fears. When the market feels uninvestable, it may present the best opportunities to buy quality stocks at discounted prices.

- Avoid the Noise

- Turn off financial news, podcasts, and social media that amplify fear or euphoria. Constant exposure to market commentary can lead to emotional decisions and distract from long-term goals.

- Respect, But Don’t Obsess Over Valuations

- While valuations matter, they’ve shifted higher due to long-term macroeconomic and structural changes. High valuations alone shouldn’t prevent investing, especially if long-term growth prospects are strong.

- Follow a Disciplined Process

- Have a clear investment strategy that includes specific buying, holding, and selling rules. This can consist of value-based entries, technical signals, or periodic rebalancing.

- Focus on Fundamentals

- Price declines in fundamentally strong companies often present buying opportunities. Avoid selling based on short-term noise if the underlying business remains solid.

- Embrace Market Cycles

- Understand that volatility is normal. Corrections, crashes, and rebounds are part of long-term market behavior. Trying to time every move often results in missed opportunities.

- Don’t Be Swayed by “Expert” Predictions

- No matter how credible, forecasters and macro strategists frequently get it wrong. Avoid making wholesale portfolio decisions based on the latest prediction or warning.

- Stay the Course and Think Long-Term

- As Peter Lynch wisely noted, more money is lost anticipating corrections than in corrections themselves. Commit to your long-term investment plan and adjust with discipline, not panic.

Now, go get to work building your wealth.