Trending

Chart 1: DXY Dollar Index Trends

The structural bear case for the US dollar still lacks meaningful supporting evidence. The dollar’s cyclical downtrend since its 2022 peak is minor compared to historical selloffs. The current trend lacks the momentum of the prior two major declines, supporting the thesis that this is not a breakaway shift in confidence.

Chart 2: DXY Fair Value

DXY valuation models show the dollar has digested the geopolitical and fiscal risks that pushed the index down following the announcement of new tariffs in 2025. The discount that developed has closed, and the spot DXY now trades at or slightly above its assumed fair value.

Chart 3: Rate Hike Risks

Current monetary policy in the US, Eurozone, and UK remains below the levels suggested by the Taylor-rule1.

When major reserve currencies suffer from a lack of monetary policy credibility, relative advantages can determine capital flows. The dollar wins this competition. The spot DXY has erased its previous discount and now trades near model fair value.

Higher economic growth in the US offers better economic insulation against inflation and gives the Federal Reserve more room to maneuver than the UK or EU central banks. Although the rapidly growing US debt is a major risk if investors fear a debt spiral or financial repression.

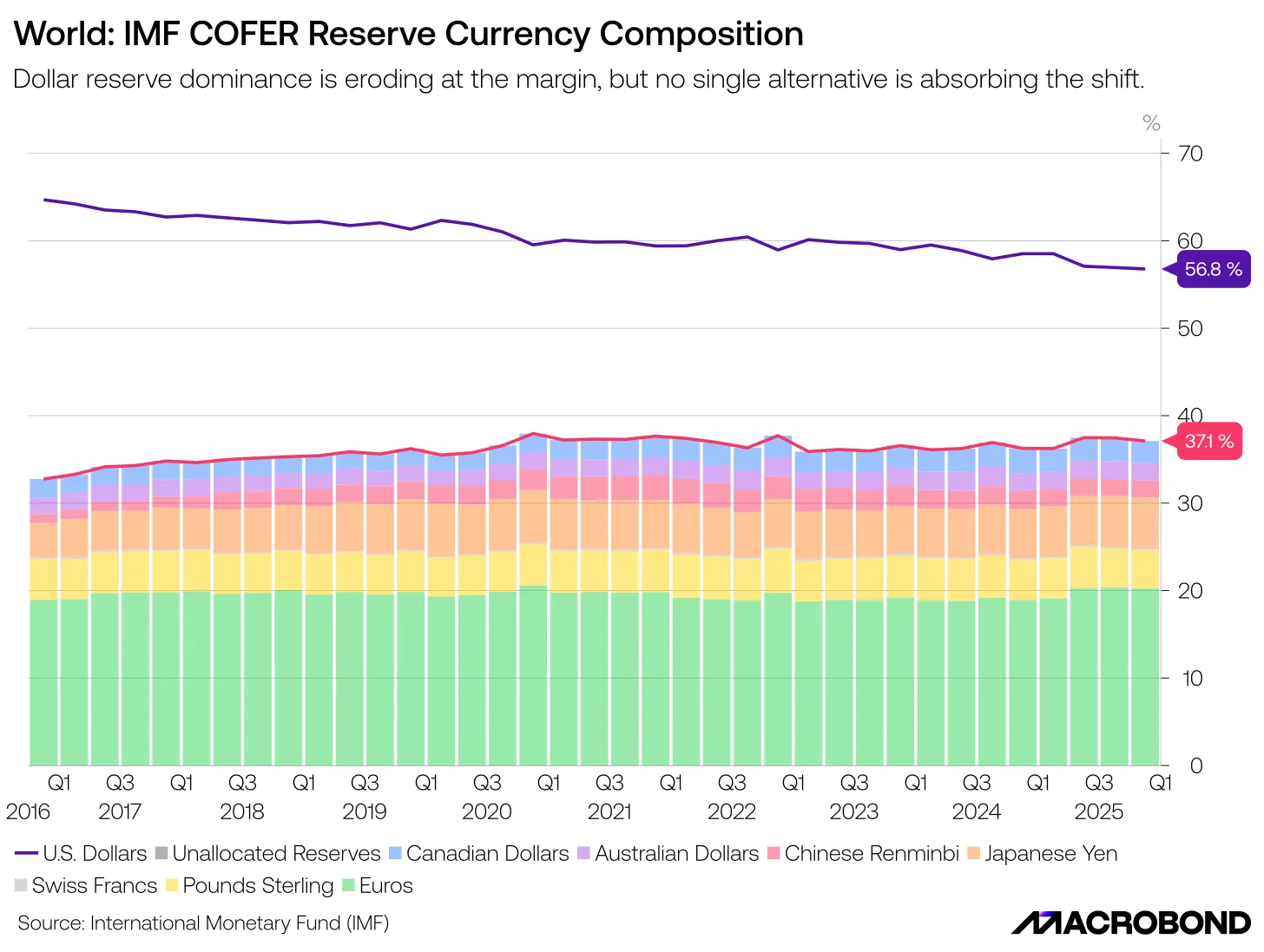

Chart 4: Reserve Currency Competition

The latest IMF COFER2 data shows the dollar’s share of allocated global reserves drifted down to 56.8% in the final quarter of 2025. This decline is a continuation of a long-term trend and the foundation for much of the bearish sentiment surrounding the dollar. However, the key detail is that currency reserves are being diversified across smaller alternative currencies rather than concentrated toward a single rival like the Chinese renminbi or the euro.

Capital exiting the dollar is scattering across minor alternatives instead of consolidating behind a single challenger. The euro remains the primary reserve alternative, but energy-driven inflation forces a costly trade-off for the European Central Bank: hike rates to fight inflation and suppress growth, or accept a weaker currency.

With growth in the Eurozone already weak, it’s a devil’s bargain.

Chart 5: Come Home to the Dollar(s)

Speculative positions confirm investors reluctance to flee the US dollar. Since October, investors have moved from a net-short to a net-long position, with the Australian dollar the only other major currency to see similar results.

De-dollarization remains a talking point rather than a trading strategy, even in today’s tense geopolitical environment.

In Summary

The slowly fragmenting currency reserves market isn’t causing an exodus from the US financial system, in part because US equity markets still offer substantial returns to investors on a relative basis.

Currency diversification may reduce dollar demand at the margin, but it doesn’t automatically create a replacement system capable of competing with the dollar. A viable global reserve currency requires deep liquidity, unmatched capital markets, and a strong business and regulatory environment.

Until a single rival pairs those traits, the dollar will remain the uncontested anchor of global finance. Nothing in the current shifts in the global monetary system points to the abandonment of the dollar.

Related: Stocks Keep Climbing as Bond Yields Flash Fresh Inflation Risks

1 The Taylor Rule provides a guideline for how central banks (like the Federal Reserve) should adjust short-term interest rates in response to inflation and economic growth. The rule oversimplifies the inputs for rate policy decisions which is why central banks do not follow it strictly.

2 IMF = International Monetary Fund; COFER = Currency Composition of Official Foreign Exchange Reserves