Trending

Written by: Caglasu Altunkopru

China’s economy has been recovering since its severe summer lockdowns, helped by modest policy support. But a strict zero-COVID policy and housing struggles have crimped economic growth and performance relative to developed markets. China’s policy machinery could kick into a higher gear after the 20th National Congress of the Chinese Communist Party (NCCCP), which convened this week.

Then: Favorable Outlook for China

Early in 2022, many investors expected emerging-market (EM) equities to outperform, aided by a recovery in China. Headwinds from policy interventions to support China’s “Common Prosperity” goals were expected to fade and give way to stimulus, while developed economies would be withdrawing fiscal and monetary policy support.

China was expected to continue its zero-COVID policies, but case numbers generally seemed under control—with fewer lockdowns. Equity valuations were generally attractive, especially in the wake of Common Prosperity actions that impacted broad swaths of the economy—including technology, education and property.

Now: Headwinds from Lockdowns, Housing and Modest Stimulus

Things have played out differently over the course of the year. Economic growth has been weighed down by continued deleveraging on the property market and more stringent COVID-19 lockdowns since the summer.

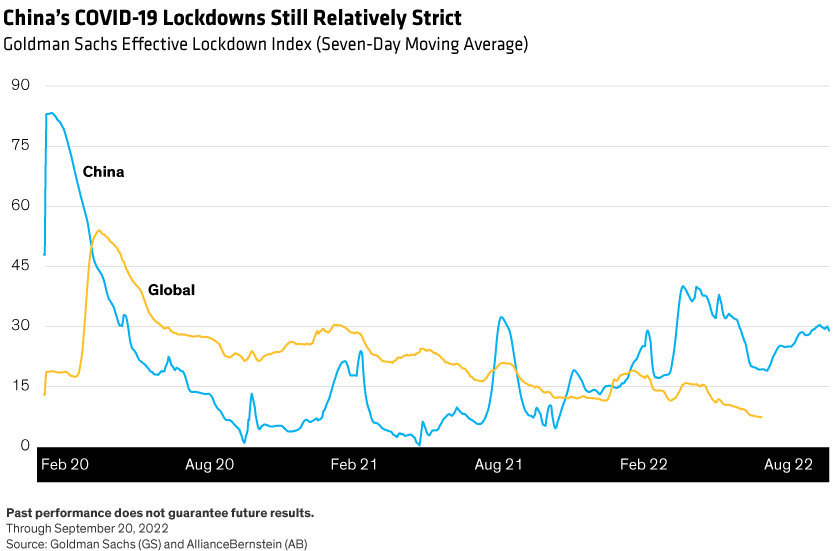

Intermittent spikes in cases from more transmissible variants have weighed heavily on economic activity since the beginning of the year, with severe lockdowns in Shanghai during the second quarter sapping domestic demand and straining global supply chains again. Overall case numbers have since declined, but lockdown measures are still stricter than those of other economies (Display).

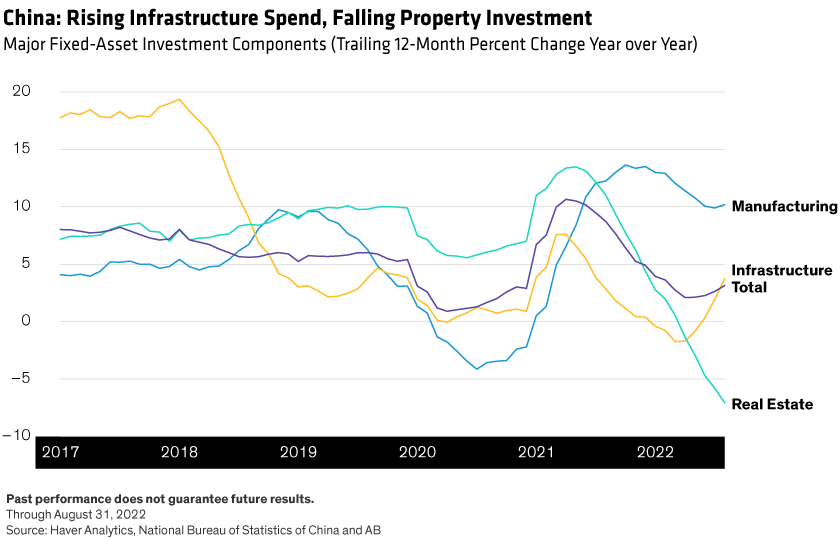

Real estate has been another drag on growth. The housing market continues to struggle, as evidenced by historically high credit spreads for debt issued by China’s property developers. Policy support so far has been rather localized and short of the comprehensive measures that could stabilize the market. As a result, real estate investment has declined sharply.

We saw the beginnings of a strong infrastructure investment cycle, as government stimulus started to come through, but it was fully offset by declining real estate investment. Total fixed-asset investment growth remained near historical lows (Display).

With household consumption still suppressed by lockdowns, it’s no surprise that 2022 is now expected to be the second-slowest growth year for China (after the pandemic year of 2020) in over 40 years. Heightened geopolitical tensions have also weighed on China equities. Through October 12, the MSCI China Index fell 30% this year, compared to the MSCI World Index, which is down 20%. Much of the underperformance is due to poor earnings, which reflect weak growth and profitability.

Chinese National Congress Could Unlock Policy

The conservative nature of recent policy choices is partly driven by the impending 20th National Congress of the Chinese Communist Party, which convenes this week. China’s hallmark political forum meets every five years to elect and appoint leaders and regroup on domestic and foreign policy agendas. With many senior officials expected to move into different roles or step down after the event, the inclination has been to leave major policymaking to the next government. This likely explains in part the absence of a more comprehensive response to the housing slump—a major drag on growth.

As for lockdowns, given how closely President Jinping Xi has been associated with the zero-COVID policy, it stands to reason that control measures remained stringent leading up to the Congress. Given the dramatic growth slowdown and rising social cost of the zero-COVID policy, we expect a gradual easing of current restrictions in the wake of the Congress. However, given China’s low vaccination rates among the elderly (just 67% of those over age 60 have had a third shot) and generally low virus exposure at the local level, we expect a cautious approach, at least at the outset. A renewed drive to boost vaccination levels is a wild card that could accelerate this process.

The Ripple Effect of Better China Growth for Multi-Asset Investors

Policies to stabilize the property sector, a gradual easing of COVID-19 restrictions and more infrastructure investment could lift growth from current lows, but we don’t expect a return to the investment-led boom of the 2000s. We expect the Common Prosperity theme to continue driving a shift from “growth at all costs” to an emphasis on more equitable growth. Real estate’s potential recovery will likely be very different relative to past cycles.

Accelerated renewables investment could be another important outcome post-Congress. China is among the countries that have suffered from extreme weather events, and it generates a significant share of global emissions. China already has significant investment in renewables technologies. For example, the country accounted for 53% of 2021 global electric vehicle sales. Specific policy actions will take time to play out after the Congress, but we expect China to see a recovery from 2022 in 2023. Investment growth has historically risen in the year following the NCCPC.

From a multi-asset perspective, the implications of improved growth in China’s economy extend well beyond its borders—lifting EM and potentially putting a floor under global economic growth. That could have meaningful implications for asset-allocation decisions.

Related: Will the Future Be More Volatile for Equity Investors?