Written by: David M. Lebovitz

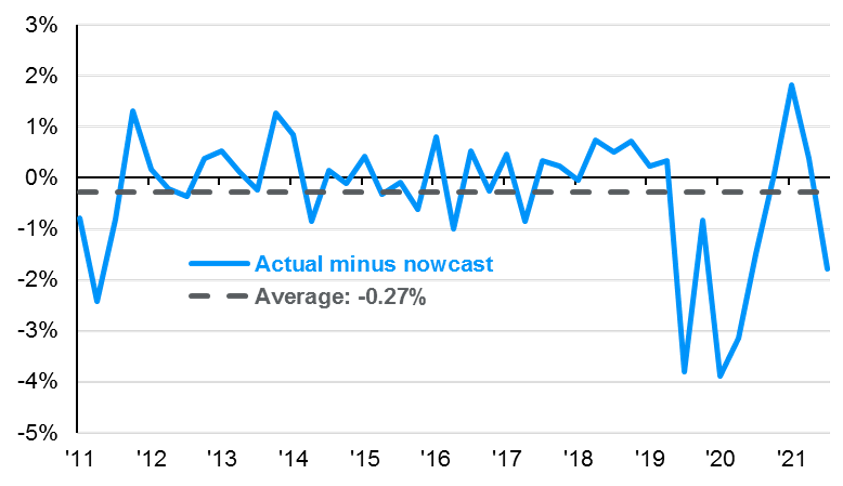

The first quarter saw the U.S. economy contract, as slower inventory growth and a growing trade deficit offset strength in consumption and investment. Recently, recession fears have bubbled to the surface, as the Federal Reserve Bank of Atlanta’s “nowcast” of economic growth now points to a contraction in 2Q22. This tracker – appropriately named GDPNow – is based on a series of rigorous mathematical techniques and uses appropriate reference data to compute weekly estimates of aggregate GDP’s 13 subcomponents. Real GDP growth is then calculated using a methodology similar to that of the U.S. Bureau of Economic Analysis.

The latest projection suggests that 2Q22 real GDP will decline 2.1% due to a significant slowdown in consumer spending and a contraction in private investment. This is in stark contrast to the Atlanta Fed’s maximum 2Q22 forecast of 2.5% in mid-May. The Atlanta Fed’s recent reading has garnered much attention, because, if realized, it would indicate that the U.S. economy has met the “back of the napkin” definition of recession – two consecutive quarters of negative economic growth. Importantly, however, this is a heuristic; the National Bureau of Economic Research (NBER) is the official scorekeeper of U.S. recessions.

Looking ahead, we recognize that recession risk has risen. That said, it seems premature to make a call that we are already in recession today. To start, the labor market remains robust, with job openings still elevated, wage growth solid, and payroll employment growing at a rapid clip. Furthermore, many of the pain points in the economy have begun to correct themselves – commodity prices have come off the boil, inflation looks to have peaked, and market expectations are now for the Federal Reserve to begin cutting rates in 2023.

For investors, it is important to remember that markets are forward looking. Put differently, the equity market tends to peak before a recession starts and trough before the economic data begins to improve. While risks to the outlook have risen, valuations have become more favorable and sentiment is beginning to look washed out; this is not an attempt to call the bottom, but rather a recognition that the outlook for risk assets is more favorable today than was the case at the start of the year.

Atlanta Fed GDPNow tends to over-estimate growth

BEA advance estimate less pre-announcement nowcast, %

Related: Does Investing in European Equities Still Make Sense?

Sources: Atlanta Fed, BEA, J.P. Morgan Asset Management.

Data are as of July 6, 2022.