Trending

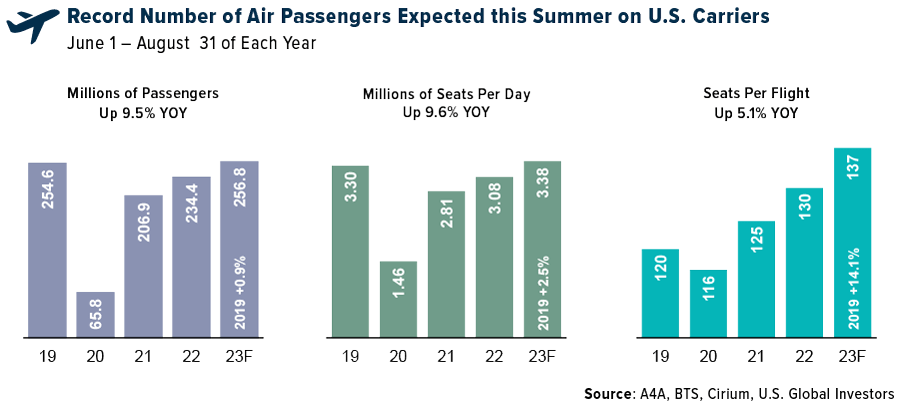

If current forecasts are accurate, this summer could mark a historic high in airline passenger volumes. The industry group Airlines for America (A4A) predicts that approximately 257 million people will travel on U.S. commercial airlines from June 1 to August 31, representing a 9.5% increase from the previous summer. That would also set a new record, as volumes are projected to surpass summer 2019 levels by around 2 million passengers.

To meet demand, airlines will employ larger aircraft and increase capacity by adding approximately 297,000 seats per day. Airlines for America (A4A) expects the daily average of seats this summer will reach nearly 3.4 million, an increase from 3.3 million per day during the summer of 2019. This translates to an estimated 137 seats per flight, representing a 14% rise compared to four years ago.

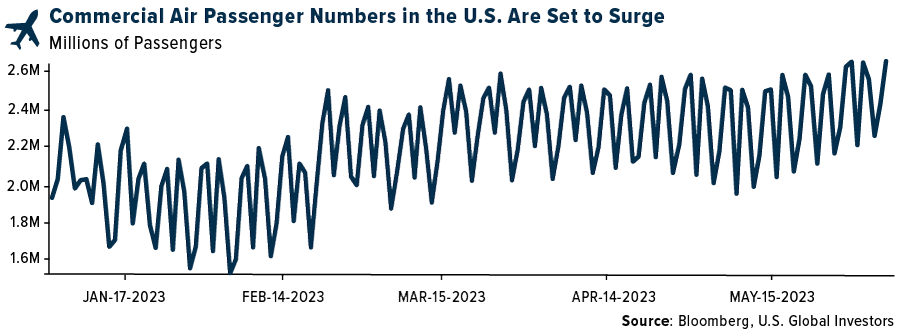

Memorial Day weekend is typically viewed as the informal launch of the busy summer travel season, and this year was no different. According to data from the Transportation Security Administration (TSA), some 9.8 million people flew on commercial airlines in the U.S. from Friday to Monday of the previous week. This figure is slightly higher than the 9.7 million who traveled during the same holiday weekend in 2019.

Rise In Leisure Travel Offsets Slow Recovery Of Business Travel

I should point out that we’re seeing these new record volumes despite the fact that business travel has yet to recover to pre-pandemic levels.

Leisure travel, though, is hot right now, even with recession storm clouds gathering over the horizon. A survey conducted in late April and early May by luxury retailer Saks found that more than three quarters (77%) of American adults had plans to book or had already booked a trip in the next three months. Of those, 74% said they would buy luxury items during their trip.

American Airlines Raises Q2 Guidance Amid Strong Demand And Lower Fuel Costs

American Airlines, the world’s largest airline by passengers carried, upgraded its guidance for the second quarter based on what it sees as “continued strength in the demand environment.” In a regulatory filing this week, American said it now forecasts quarterly earnings per share to fall within the $1.45 to $1.65 range, an increase from its previous estimate of $1.20 to $1.40 per share.

The revision is based on not only stronger-than-expected demand but also lower fuel costs. The carrier estimates it paid between $2.55 and $2.65 per gallon on average during the quarter, or $0.10 less per gallon than its initial forecast. Fuel consumption is also down compared to years past since American is flying larger aircraft that can accommodate more passengers per flight; this approach is more efficient than operating smaller jets with fewer passengers.

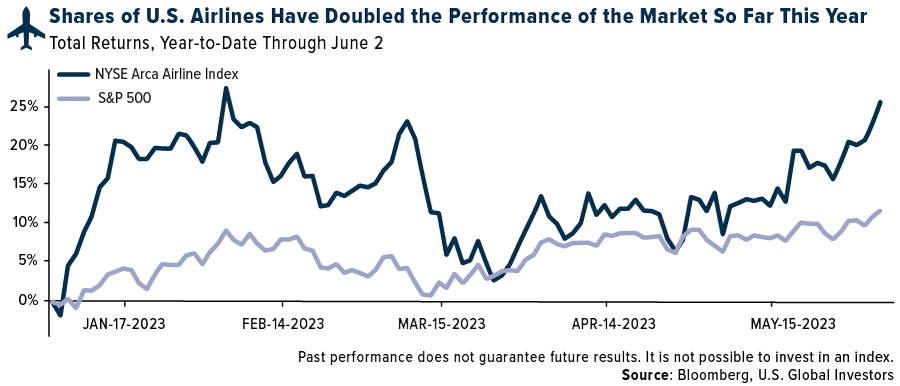

Investors appear to have recognized airlines’ versatility and ability to raise capacity to meet demand. Shares of U.S. airlines have soared more than 27% so far this year, more than double what the S&P 500 has returned. Standout performers include United Airlines, up 27% for the year, and American, up 17%. Among the Big Four carriers, Southwest Airlines is the only one to trade in the red, as it continues to face challenges after its network meltdown during Christmas 2022.

Depressed PMIs, Falling Commodity Prices And Election-Year Investment Prospects

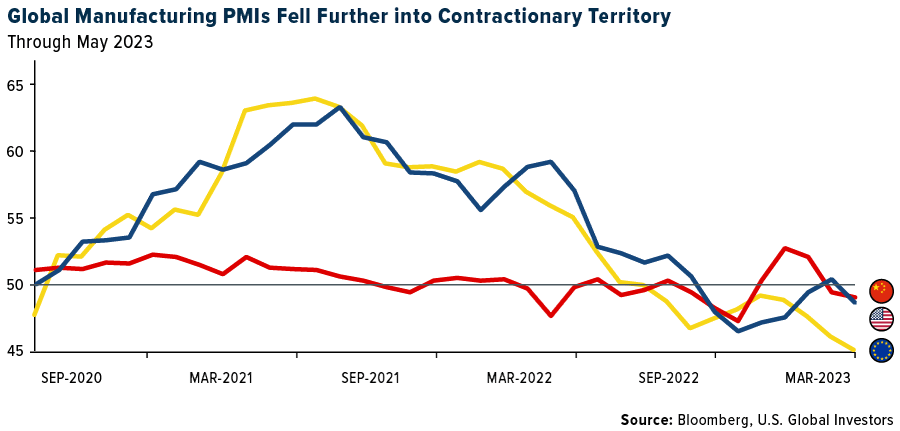

A possible headwind to continued economic growth could be the depressed purchasing manager’s indexes (PMIs). In May, the Eurozone Manufacturing PMI fell to 44.8 from 45.8 in April, the steepest contraction in three years. The U.S. Manufacturing PMI also shrank in May, sliding to 48.4 from a neutral 50.2 in April. The JPMorgan Global Manufacturing PMI recorded 49.6, just below the threshold and little changed from March to April.

China was the only major economy to report month-on-month expansion in its manufacturing sector. The Caixin PMI of private Chinese firms was 50.9 in May, marking the first positive reading in three months. (China’s official state-run PMI, however, fell to 48.8 in May.)

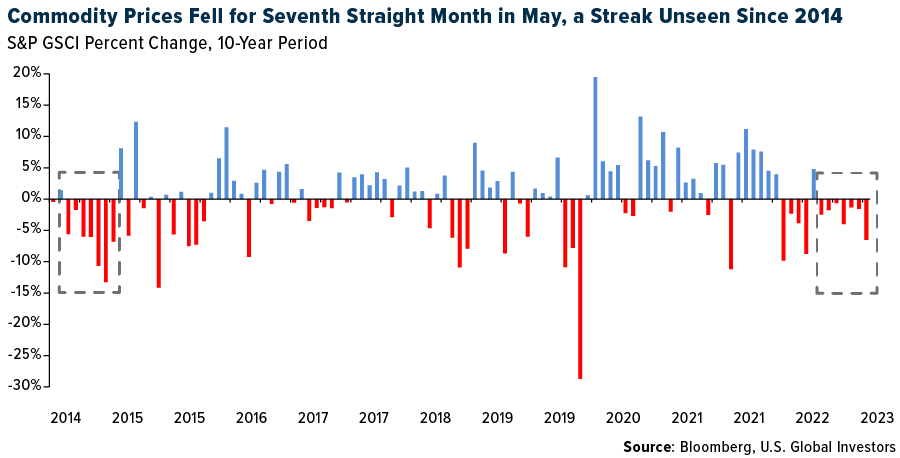

Widespread manufacturing weakness helps explain why commodity prices have plunged this year. The energy-heavy S&P GSCI lost ground for the seventh straight month in May, a streak we haven’t seen since 2014 when oil collapsed. Year-to-date, the index of raw materials is down nearly 12%.

The drop in commodity prices is obviously good for consumers as well as companies, particularly those involved in shipping and transportation.

I believe it could also be good for investors. The 2024 elections occur in 17 months. President Joe Biden’s approval rating currently stands in the high 30s and low 40s, and Congress’s is even lower at around 16%, according to the latest Gallup poll. To appeal to voters, elected officials may be more inclined to pass and enact legislation that would ignite growth and drive demand, which in turn would support asset prices.

Reflecting On Meritocracy: The U.S. Commitment To Rewarding Excellence

On a final note, I want to reflect on my admiration of the country and culture I’m privileged to call home. I don’t know how many of you tuned into the Scripps Spelling Bee, but it got me thinking about the United States and, more specifically, meritocracy.

Although many other countries have their own national spelling bees, I’m not sure if they’re broadcast or generate as much attention as the contest in the U.S. does. A lot of this has to do, I assume, with how notoriously difficult English words are to spell compared to other languages. But beyond that, America—more so than any country that I know of—rewards and recognizes merit, from superhuman athletes to skilled money managers to phenomenal spellers.

When a society is based on merit and persistence, as it is in the U.S., it creates an environment where competition and innovation can flourish. It’s no accident that, of the top 20 largest public companies by market cap, 15 are American.

Let’s hope that future generations remain committed to the principles of merit that have made the U.S. the greatest nation in history.

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.02%. The S&P 500 Stock Index rose 1.83%, while the Nasdaq Composite climbed 2.04%. The Russell 2000 small capitalization index gained 3.26% this week.

- The Hang Seng Composite was flat this week; while Taiwan was up 1.22% and the KOSPI rose 1.66%.

- The 10-year Treasury bond yield fell 11 basis points to 3.69%

Airlines And Shipping

Strengths:

- The best-performing airline stock this week was Azul, which increased by 20.56%. Chinese airlines observed robust domestic ticket pricing during the first half of May, a trend expected to persist in the coming months due to im0.proved industry rationality. Japan’s domestic travel also reported robust traffic for May, with ticket prices maintaining stability. Despite supply disruptions at Go First, Indian traffic in May was strong, with rival airlines likely to benefit from higher ticket prices and yields during the summer peak.

- Despite Russia’s supposed retaliation to sanctions and price caps imposed by the Group of Seven nations with a 500,000 barrel per day output cut, shipments of Russian crude oil have actually increased. Vessel tracking data monitored by Bloomberg reveals that crude shipments from Russian ports in the four weeks to May 21 were over 480,000 barrels per day higher than during the four weeks to February 26, the baseline month for the Russian production cut.

- Aircraft suppliers anticipate a 3% sequential upside in the second half of 2023 due to labor headwinds, compared to the first half of the year. In addition, the expected price escalation for the next six months has dropped to 4.2% (down from 5.7%), a positive development. While the near-term outlook for supplier production levels for Boeing 737 MAX and 787 has slightly declined, the outlook for 2024-2025 has stabilized, which is another positive.

Weaknesses:

- The worst-performing airline stock for the week was SATS, which decreased by 11.70%. airBaltic, the launch customer for the A220, has grounded 10 of its 41 A220s, citing insufficient engine availability through 2024. This announcement follows a comment made by Lufthansa in March that it grounded six of its 18 A220s, with the delay in engine supply expected to ease later in 2023.

- Global newbuild orders for April fell to 2.3 million tons, down 36% month-on-month, and 52% year-on-year, indicating weak order flows. Except for liquified petroleum gas (LPG) carriers and tankers, which saw growth in both month-on-month and year-on-year terms, all other vessel types, including container, liquified natural gas (LNG) and bulk, contracted by 40-80% year-on-year. Korean shipbuilders secured a 28% market share in April, while Chinese shipbuilders claimed a 65% share.

- Airline net sales fell by 3.5% compared to 2019 for the week, compared to a decrease of 0.4% in the previous week. While volumes and pricing both showed sequential deceleration, international sales remain stronger than domestic sales. Large corporate sales continue to lag and all sales channels slowed down this week. Even international bookings have started to dip.

Opportunities:

- Lufthansa announced plans to acquire a 41% stake in Italian airline ITA for €325 million, pending finalization. This will be in the form of a capital increase, and the Italian Ministry of Economy and Finance (MEF) will contribute €250 million in capital. Lufthansa will have the option to acquire the remaining stake, contingent on certain financial targets being met. No further financial details were provided.

- The tanker order book, currently at roughly 5% of the existing fleet, remains at a multi-decade low. This compares to a starting point of 20% in 2003, which marked the beginning of the best 5-year run for tanker rates (and stocks) in the last half-century. Although the order book has recently started to grow after a seven-year decline, it is still 75% lower than it was at the start of the aforementioned bull market.

- According to Cowen, summer 2023’s travel season, which kicks off this weekend, is expected to surpass 2019 levels. They predict that 275 million people will travel between Thursday, May 25, and Monday, September 4, marking a 19% increase from 2022’s 230.6 million and a 7.4% rise from 2019’s peak of 256 million.

Threats:

- Historically, year-over-year changes in fuel prices have proven to be the most influential leading indicator for year-over-year changes in unit revenue. The second quarter of 2023 is tracking a 40% year-over-year decrease in jet fuel prices, following a modest increase in Q1 2023 and increases throughout 2022. A fuel decline of this magnitude could pose a 5 to 6 percentage-point headwind to revenue growth (with a lag). Despite lower fuel costs, revenue outlooks for the near term (Q2) may be stickier for carriers with higher international/transatlantic routes. Lower fuel costs combined with assumed revenue towards the lower end of prior Q2 guides are likely to lead to higher earnings estimates, while valuations remain broadly depressed.

- World trade continues to languish, with U.S. imports trending 20% year-on-year lower due to ongoing inventory destocking. Container spot rates are expected to trend downwards, with the market struggling to replicate the success of recent rate hikes, given limited discipline (idling stands at just 1.3%). Transpacific contract repricing, which is done at or slightly below profit and loss break-even, is likely to put a damper on pricing in the coming months.

- Volaris employees have scheduled a strike for Friday, June 2, protesting against labor conditions of pilots, crew members, and other company employees. The employees have also accused the union of lacking support. If Volaris and its employees fail to reach an agreement concerning necessary changes, the company’s operations may halt at all its bases in Mexico, including Mexico City, Guadalajara, Tijuana, Cancun, Monterrey, Culiacán and León, according to Axis Negocios.

Luxury Goods And International Markets

Strengths

- Tema ETFs, a new investment platform, has introduced an actively managed luxury ETF, trading under the ticker symbol LUX US. This indicates a robust performance in the luxury sector and a rising interest among investors in this sector.

- FactSet’s Earnings Insight reveals that S&P 500 companies have delivered their strongest performance relative to expectations since Q4 2021. Both the number and magnitude of companies reporting positive earnings-per-share surprises surpass their 10-year averages. Furthermore, 43% of companies have revised their annual sales guidance upward, marking the second-highest proportion since 2015.

- Tesla was the best-performing S&P Global Luxury stock in the past five days, gaining 10.6%. Tesla will receive about $1.8 billion in production tax credits this year under the Inflation Reduction Act (IRA), according to forecasts from researcher Benchmark Mineral Intelligence, far exceeding an estimated $480 million tax credit for General Motors and LG Energy Solution. In the next few years, Tesla will be the biggest winner of the IRA Production Tax Credit. The company may receive $41 billion in credits by the end of 2032, far exceeding the tax credit benefits of its competition.

Weaknesses

- Bernard Arnault, owner of Louis Vuitton, was displaced as the world’s wealthiest individual by Tesla’s CEO Elon Musk on Wednesday. This occurred as Louis Vuitton shares took a dip while Tesla’s strengthened. Mr. Arnault plans to visit China, one of the world’s largest consumer markets, later this month, following Jamie Dimon, CEO of JPMorgan, and Musk.

- Recent manufacturing data suggests a possible recession or economic slowdown in global economies. The eurozone’s production activity index fell to 44.6 in May from 45.8 in April. Similarly, China’s Manufacturing PMI weakened to 48.8 in May from 49.2 in April. In the United States, the manufacturing index fell below the 50-mark, dropping to 48.5 from 50.2 in May.

- Lucid Group was the worst-performing S&P Global Luxury stock in the past five days, losing 16.2%. Shares declined after the company announced a $3 billion stock offering and private placement. Lucid said that it plans to issue 173.5 million shares with BofA Securities acting as sole underwriter. Separately, the company’s majority shareholder, the Ayar Third Investment Company, a unit of the Public Investment Fund, is planning to purchase 265.7 million shares in a private placement.

Opportunities

- The U.S. Senate voted to suspend the U.S. debt ceiling and enforce spending limits through the 2024 elections, staving off a potential default. This bill is now awaiting President Joe Biden’s signature, which caused global equities to rise on Friday.

- According to FactSet, casino revenue in Macau surged 366% year-over-year to $1.93 billion in May, marking the highest level since pre-COVID restrictions in January 2020. Despite a labor shortage, about 500,000 visitors arrived in Macau during the May holiday. The post-COVID travel rebound is expected to further boost the consumer sector.

- Inflation in Europe is decelerating. The CPI index in France slid to 5.1% YoY in May from 5.9% in April, while Germany’s index dropped to 6.1% from 7.2%. The aggregate Eurozone CPI index also fell to 6.1% in May from 7.0% in April. Mid-June will bring further CPI data from the U.S., with Bloomberg Economists predicting a further easing of YoY prices.

Threats

- The luxury sector might face additional correction, particularly after a strong year-to-date performance. The S&P Luxury Index gained 16% YTD, compared to the S&P 500 Index and Stoxx 600 Index, which returned 9.3% and 8.8%, respectively.

- The conflict in Europe has intensified, with reports of Ukraine deploying drones to strike residential buildings in Moscow. Several drones were downed over the Rublyovka district, a region housing Moscow’s political and business elites, located just miles from Vladimir Putin’s official Novo-Ogaryovo residence. This counterstrike by Ukraine followed Russia’s severe attack on Kyiv.

- Saks’ Luxury Pulse, a quarterly online survey that captures the attitudes of luxury consumers, indicates a growing inclination to save more, travel more and spend less on luxury goods. In the most recent survey, nearly half of the respondents (47%) indicated plans to reduce their spending on luxury items in the next three months. This compares to the previous survey in January when only 38% of respondents planned to cut back on luxury spending. Saks, operator of the luxury website Saks.com, concluded that luxury consumers are growing increasingly anxious about the overall economy in the United States.

Energy And Natural Resources

Strengths

- The best-performing commodity for the week was uranium, as bogged by the Sprott Physical Uranium Trust’s share price, rising 9.XX%. Uranium stocks surged around the world after the U.S. Senate Environment and Public Works Committee advanced a bill to aid the development of advanced nuclear reactors. The legislation, known as the ADVANCE Act, passed out of the EPW Committee by a vote of 16-3. Copper is experiencing a weekly gain, driven by the anticipation of a key U.S. jobs report and positive developments in China’s property market. The passage of legislation to suspend the U.S. debt ceiling and the potential measures by China to support the property market have improved the demand outlook for copper.

- The approval of Savannah Resources’ Barroso lithium mine in Portugal represents a significant step toward Europe’s goal of reducing dependence on China for lithium, a key raw material for electric vehicle batteries. Once operational, the mine is estimated to produce enough lithium to power 400,000 electric vehicles. The lengthy permitting and feasibility processes for new mines in Europe present a potential delay in the project’s timeline. However, the proposed Critical Raw Materials Act in the European Union aims to streamline permitting procedures and accelerate projects, which could mitigate some of the delays.

- Glencore’s potential increase in its bid for Teck Resources reflects its determination to resolve the battle over the Canadian miner’s future. A higher offer could put pressure on Teck’s board and shareholders to reconsider their opposition and engage in negotiations. The outcome of the bid will depend on various factors, including shareholder support, management’s stance and the influence of Norman Keevil, a key shareholder with veto power. The Canadian government’s stance on foreign acquisitions and the broader regulatory environment will also play a role. Investors should closely monitor the developments and assess the potential risks and rewards associated with the bid.

Weaknesses

- of cheap Russian oil have led to a decline in shipments from Saudi Arabia, crowding out the latter in the Indian market. The average cost of Russian crude imported by India is at its lowest level since the country started buying major volumes from Moscow. The shift in oil imports from Saudi Arabia to Russia indicates changing dynamics in the global oil market. It may impact Saudi Arabia’s market share and pricing power.

- Pakistan’s plan to import a significant portion of its oil needs from Russia raises concerns about diversification and potential geopolitical implications. The reliance on Russian oil imports could impact Pakistan’s energy security and vulnerability to supply disruptions. While importing oil from Russia may offer cost advantages, diversification of energy sources and suppliers is important for long-term energy security. Pakistan should consider a balanced approach that includes multiple sources and diversification of its energy mix.

Opportunities

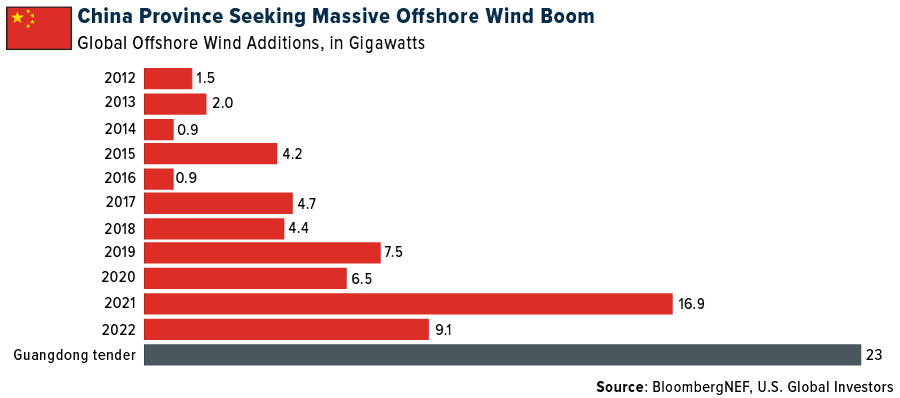

- Guangdong province in China is accepting bids to construct 23 gigawatts of offshore wind power, which is more than the world has ever built in a single year. The province aims to meet rising energy demand and address energy shortages caused by erratic hydropower supply. The significant investment in offshore wind power in Guangdong presents a promising opportunity for companies involved in the wind energy sector. The scale of the projects indicates the province’s commitment to renewable energy and the potential for long-term growth.

- Longi Green Energy Technology, the world’s largest solar manufacturer, has reduced wafer prices by up to 31%, aiming to stay competitive in the increasingly cost-competitive solar sector. The price reduction follows a decline in solar silicon prices and increasing production capacity in the industry. The price reduction in solar wafers by Longi indicates the ongoing cost competition in the solar industry. Lower costs for key components like wafers could lead to improved profitability and market positioning for solar manufacturers. However, investors should assess the impact on the company’s margins, demand dynamics, and the overall competitive landscape to make informed investment decisions in the solar sector.

- Mining companies, particularly those involved in copper, lithium and other metals essential for the energy transition, are facing challenges in attracting young workers. The industry is struggling to fill high-skilled roles such as engineers, exploration geologists and data analysts, potentially impacting expansion plans and growth. The recruitment challenges in the mining industry are hampered by some universities barring extractive industries from recruiting on campus property. Efforts to attract young talent, diversify the workforce, improve industry reputation and offer career development opportunities are very promising. However, the perception of mining in social media as a non-essential industry needs to be rebranded with the opportunities it presents as a critical tool for addressing climate change.

Threats

- The weak manufacturing and services data from China this week indicates a contraction in economic activity, raising concerns about the growth outlook. The risk of a downward spiral, particularly in the manufacturing sector, is becoming more real, which could have broader implications for the Chinese economy and global markets. The slowdown in China’s manufacturing sector poses a threat to companies operating in industries dependent on Chinese demand, such as raw materials and industrial goods. Mitigating factors could include policy measures taken by the Chinese central bank to stimulate the economy and boost confidence.

- Weaker-than-expected economic data from China, coupled with a stronger U.S. dollar, has added to concerns about oil demand, leading to a decline in oil prices. The combination of a sluggish Chinese economy and a potentially dampened global demand outlook presents a threat to the oil market.

- The significant decline in commodity prices, driven by factors such as weak global economic conditions, industrial slumps and China’s slower-than-expected recovery, indicates a disinflationary trend. While this brings relief to consumers, there are uncertainties about the duration and extent of the disinflationary pressures, as well as the transmission to retail prices. The commodity crash poses challenges for commodity producers and investors who were expecting a China recovery to aid world economic growth.

Bitcoin And Digital Assets

Strengths

- Among the cryptocurrencies monitored by CoinMarketCap, Injective was the top performer this week, gaining 22.25%.

- A crypto startup co-founded by OpenAI CEO Sam Altman raised additional funding to further its mission of creating a digital ID for every person on the planet. As reported by Bloomberg, the startup intends to generate distinct IDs for each individual, in part, by scanning their eyes.

- Galaxy Digital CEO Michael Novogratz, while acknowledging the recent low trading volume and range-bound behavior of Bitcoin and Ethereum, told Bloomberg that these are still “the best assets to invest in over two, three, and six years.”

Weaknesses

- Pep, among the cryptocurrencies monitored by CoinMarketCap, was the worst performer this week, depreciating 13.75%.

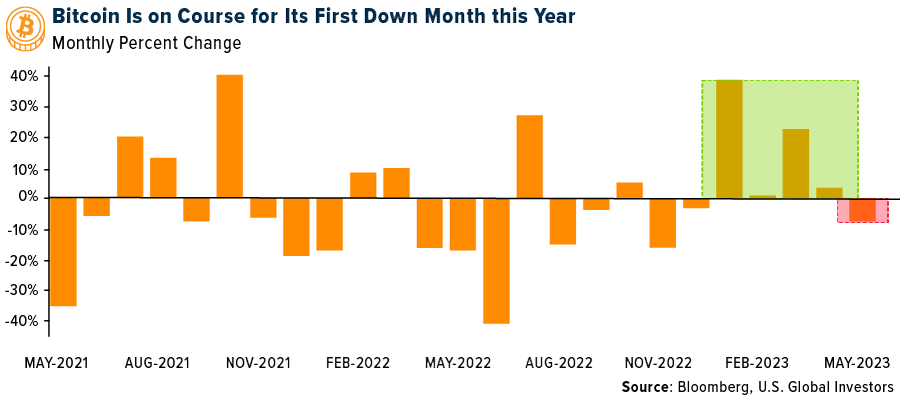

- The cryptocurrency rebound is losing momentum, causing Bitcoin to record its worst month since the FTX exchange collapse in November of the previous year. Bloomberg reports that Bitcoin’s roughly 7.6% drop in May was its first monthly decline of 2023.

- Binance, the world’s largest cryptocurrency exchange, has lost a quarter of its market share in the past three months due to an ongoing investigation by a U.S. watchdog for alleged violations of federal laws, as reported by Bloomberg.

Opportunities

- Bloomberg reports that Binance is considering a proposal to allow some institutional clients to keep their trading collateral in a bank instead of with the crypto platform. This step could potentially reduce counterparty risk.

- Bitcoin and other digital tokens were trading at a discount on Binance Australia compared to rival exchanges in the country. This situation arose as the platform is set to lose access to a key local currency withdrawal route.

- Avalanche, a layer 1 blockchain network, has surpassed 1 million monthly active users for the first time. Ava Labs, the creator of Avalanche, credits the recent launch of AvaCloud as a major contributor to this growth, according to Bloomberg.

Threats

- A crypto entrepreneur, whose business in China was disrupted by regulatory crackdowns, views his experience as a warning for companies attracted to Hong Kong’s initiative to establish a digital-asset hub. Bloomberg reports that crypto may not remain a long-term priority for Hong Kong, even though the city is currently focused on implementing new rules for the sector.

- Bitcoin mining difficulty experienced a 3.4% surge at block number 792,288, crossing the 50 trillion threshold for the first time, according to Bloomberg data.

- Binance, the crypto exchange, has reportedly received an order from one of Canada’s securities regulators to investigate whether the platform tried to bypass local regulations and compliance controls while seeking approvals in the country, as reported by Bloomberg.

Gold Market

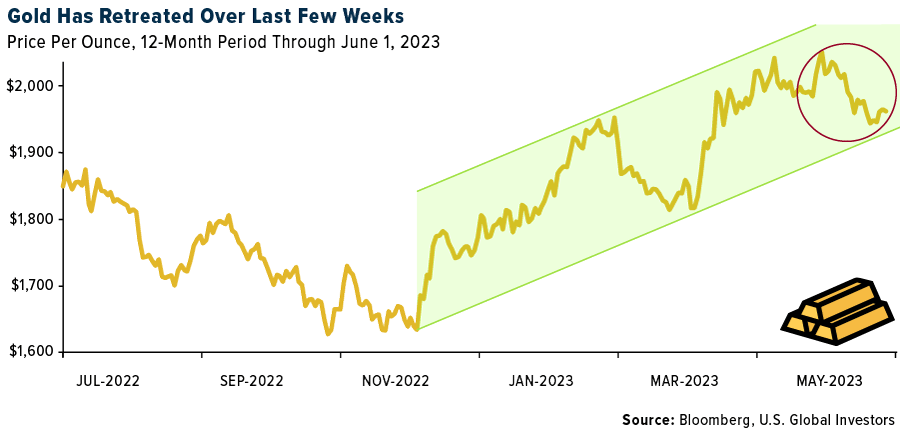

Gold futures closed the week at $1665., up $1.90 per ounce, or 0.10%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 3.73%. The S&P/TSX Venture Index came in up 0.83%. The U.S. Trade-Weighted Dollar fell 0.16%.

Strengths

- The best-performing precious metal for the week was silver, up 1.48%. snapping a three-week losing streak. Despite the decline in gold prices due to mixed U.S. jobs data and expectations of further interest rate hikes by the Federal Reserve in recent weeks, gold is still on track for a slight weekly gain of just 0.10%. This is supported by the potential easing of inflationary pressures indicated by U.S. manufacturing figures, which could lead to a pause in the Fed’s monetary tightening. Additionally, the resolution of the U.S. debt-ceiling deal reduces a major risk for financial markets and curbs demand for safe-haven assets like gold.

- The strategic investment by the European Bank for Reconstruction and Development (EBRD) in Eldorado Gold Corporation not only provides financial support to Eldorado Gold but also serves as an endorsement of the Skouries project and the company’s commitment to environmental and social standards. The investment strengthens Eldorado’s balance sheet and provides additional funding for growth initiatives across its global portfolio, enhancing its financial flexibility.

- Newmont plans to invest $540 million to extend the life of its Cerro Negro mine in Argentina. The investment is expected to boost production and provide a platform for further exploration and expansion. This demonstrates Newmont’s commitment to expanding its mining operations in Argentina, contributing to the country’s economy and showcasing the potential of its vast deposits. The investment strengthens Newmont’s position as the world’s largest gold producer and highlights its long-term growth strategy.

Weaknesses

- The worst-performing precious metal for the week was platinum, down 2.12% on little specific news. European mining stocks, represented by the Stoxx 600 Basic Resources, have underperformed, signaling a global economic slowdown. The declining prices of metals, lower profitability and reduced earnings expectations for mining companies indicate a weakening demand environment and potential challenges for the mining sector.

- The repeated attacks and ongoing security threats at Zijin Mining Group’s Buritica gold mine in Colombia present a significant weakness to their investment. The recent incidents, including the shooting of a worker and the destruction of vehicles, highlight the urgent need for intervention by the Colombian government. The escalating aggression of illegal mining activities using explosives and weapons adds to the operational and security risks, potentially impacting production and increasing costs.

- The pervasive issue of cable theft on South Africa’s Container Corridor, a crucial freight-rail line, poses a significant investment weakness for the country. The theft of copper electricity cables has resulted in severe disruptions and operational inefficiencies, hindering the transportation of imports and exports. The frequent theft incidents and subsequent delays highlight the need for increased security measures, which could incur additional costs for potential investors in the rail and logistics sectors.

Opportunities

- Aya Gold & Silver’s Zgounder mine in Morocco reported more multi-kilo high-grade silver mineralization intercepts discovered through exploration drilling. The significant assay results indicate the potential for expanding the mineralized footprint of the deposit. This exploration success may enhance the company’s resource base and future production prospects, making it an opportunity for investors interested in silver mining to consider.

- Iraq’s central bank has been steadily buying gold as part of its strategy to diversify its foreign assets but recently added 2% to its gold reserves in a single day. With geopolitical and economic risks escalating, central banks worldwide are expanding their gold holdings. Investors interested in gold may find this as an opportunity to consider the potential long-term value of gold and its role as a traditional haven during times of economic distress.

- Bloomberg reported hedge funds have a record short bet on long-dated treasuries. The investment opportunity presented in this story is the potential rush to gold if hedge funds unwind their extreme short positions on long-dated Treasury futures. Bloomberg Intelligence Senior Macro Strategist Mike McGlone sees the possibility of gold shooting as high as $3,000 an ounce in anticipation of a more dovish Federal Reserve and declining Treasury yields. The historical correlation between bearish Treasury bets and the rally in gold prices in recent years suggests that a reversal of this positioning could present an opportunity for gold investors.

Threats

- Pimco’s Greg Sharenow believes that gold still appears too expensive, particularly compared to inflation-linked government bonds (TIPs). The struggle of central banks to cut rates due to sticky inflation could diminish the demand for non-interest-bearing gold. Investors should consider the short-term risks of potential price declines and evaluate the comparative value of alternative assets in multi-asset portfolios. However, Sharenow noted that gold has long-term appeal given the threats on the horizon.

- The invasion of AngloGold Ashanti’s Obuasi mine by over 300 illegal miners highlights the security challenges and potential disruptions faced by mining operations in Africa. Illegal mining activities deprive African nations of revenue, fuel conflicts, and finance criminal and terrorist networks. Additionally, the prevalence of bullion smuggling may raise concerns about the transparency and sustainability of gold supply chains.

- Countries such as Brazil, China, India and Malaysia are seeking to bypass the dollar in their trade and investment transactions, while even traditional U.S. allies like France are completing transactions in other currencies like the yuan to avoid against the hegemony of the U.S. dollar. The perception is that the dollar is being weaponized by the U.S. to advance its foreign-policy priorities, which could lead to a decline in the dollar’s preeminent position and undermine U.S. economic power. A stronger gold price could be a benefit from a weaker dollar.

Related: NVIDIA Expected To Join the Trillion-Dollar-Valuation Club as AI Dominates