Trending

U.S. equities slipped this week as investors faced the familiar problem of strong fundamentals and thick levels of uncertainty. The Dow Jones Industrial Average declined 1.31% while the S&P 500 fell 0.44%, continuing a sideways trend that has defined large-cap stocks for months. Muted index performance and one of the narrowest trading ranges on record masked meaningful shifts in leadership beneath the surface.

Artificial intelligence remains the dominant market narrative, but the tone has clearly changed for the worse. NVIDIA delivered strong earnings, record revenue, and continued evidence of accelerating AI adoption, yet its shares still declined following the report. Markets appear less focused on the magnitude of AI demand and more fixated on hyperscaler profitability, economic collapse, or both.

One of the biggest stories of the week was Citrini Research’s “2028 GLOBAL INTELLIGENCE CRISIS,” which rocked the finance and technology world with a vision of a near-future AI dystopia. You know it’s a unique moment when Citadel is rebutting Substack articles.

The takeaway here is not that the AI momentum is fading, but it is certainly changing. Markets appear to be transitioning from outright excitement to skepticism and maybe a little fear. The absence of any euphoria suggests this market cycle is far from bubble territory, and the continued uncertainty leaves much to be desired performance-wise.

AI optimism meets investor skepticism

Semiconductor companies continue to benefit from heavy infrastructure spending, while software has struggled under fears that a steady stream of new AI tools could disrupt legacy business models. Software valuations have fallen sharply and violently, reflecting investor concern about future earnings pressure and automation risk.

However, evidence increasingly points toward integration or adaptation within the major software companies. Many AI platforms are being designed to integrate with existing enterprise tools, and those companies have the budgets and expertise to deploy them most effectively. Few software customers truly want to spin up and maintain their own versions of major software systems. Regardless of the cost savings this might offer, the legal and compliance risk is too great. When even Anthropic is hiring a Salesforce Administrator, it's natural to be skeptical of total enterprise software erasure.

The performance gap between semiconductors and software has become unusually wide, leaving room for a potential rebound in companies or whole industries that have been punished unnecessarily.

Economic crosscurrents cut both ways

Major economic data was thin this week, but what we did get mostly left a bad taste in my mouth. Producer price inflation accelerated more than expected, foreshadowing more inflation pressure in the future. The market sold off on Friday, leaving us limping into the weekend and with the first negative month for the S&P 500 since November.

The labor market might be the only bright spot as layoff anxiety tied to AI appears mostly overstated, and there are indications that conditions are improving. Initial jobless claims edged higher, but continuing claims fell. Both measures are comfortably within a normal range and below the averages for all of 2025.

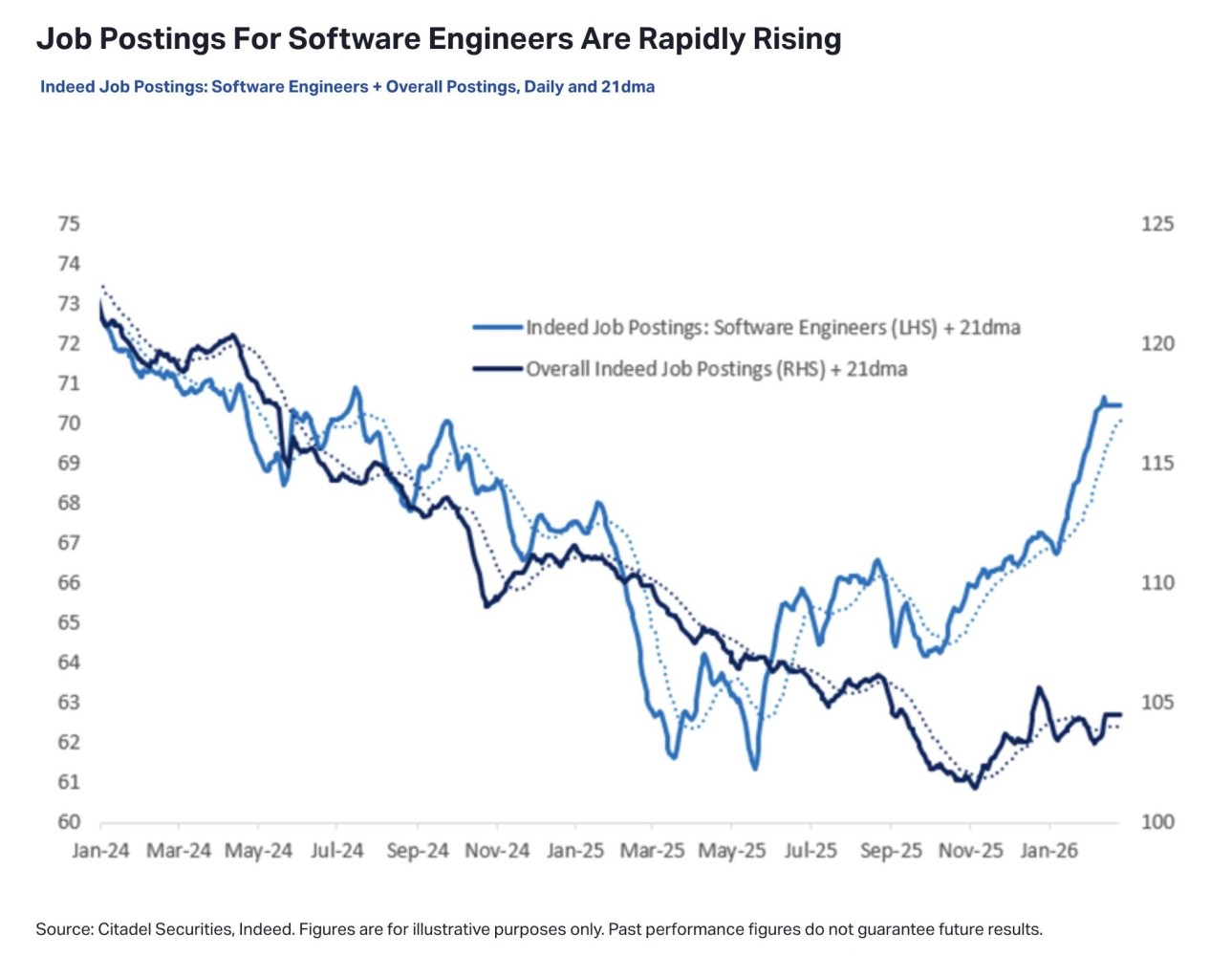

While layoffs have risen modestly in some technology roles, AI accounts for only a small share of announced job cuts. Additionally, Indeed.com data shows an uptick in software engineering roles in 2026. While this follows a lengthy depression in postings for these roles, it is an indication that AI is not even destroying the jobs it is most capable of replacing.

AI, economy-wide over hiring, job hopping, inflation, and rate hikes all happened within a 12–18-month window back in 2022. All of these factors contributed to the snapback in the labor market we are living through today. As it stands today, AI is the least likely to be the direct and primary cause of the weak labor market environment. The multiple economic dislocations and disruptions between 2020 and 2023 were naturally going to have ripple effects on society and the economy, both good and bad.

AI might get blamed for big layoff announcements (*cough*BLOCK*cough*), but overhiring, changing priorities, and poor management seem to be more likely culprits.

What this means for investors and what comes next

Sector performance reflected ongoing rotation within the market as investors are still trying to find their footing on the shifting sand. Commercial services and minerals led gains, but fewer sectors are holding onto their momentum. Gold and oil moved higher as Iran and other geopolitical issues stayed in the news throughout the week (air strikes in Iran were revealed on Saturday morning). Cryptocurrencies remained volatile after midweek swings.

U.S. stock market investors should anticipate more news- and rumor-based volatility that will be accompanied by some near-term negative performance. Especially after multiple double-digit growth years, intra-year weakness is normal. The pessimism is translating into selling, but that leaves markets with a wall of worry to climb. If stocks spend most of the year consolidating while maintaining strong earnings trends, P/E ratios will look much more welcoming within 6-12 months.

Source: Willie Delwiche & Hi Mount Research

The AI cycle may be maturing, even if investors aren’t. Earnings growth remains real, but expectations for the future are constantly being recalibrated, sometimes daily. AI capex spending alone doesn’t cut it anymore, and investors have shifted hard toward companies and industries that aren’t impacted by AI hype or disruption. With so much still unknown, predictable operations and durable earnings are receiving a healthy premium.

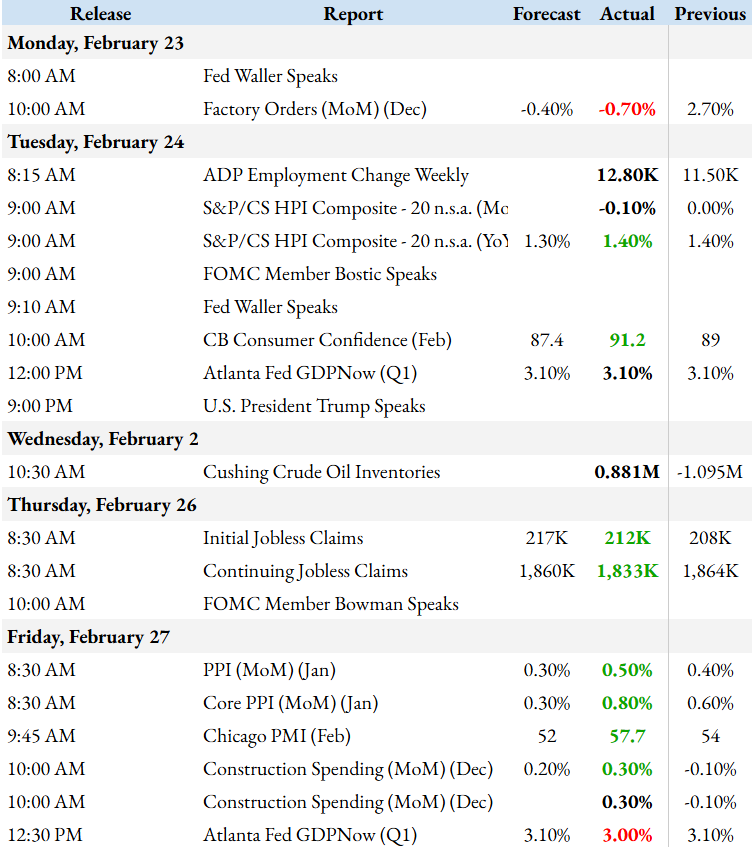

The coming weeks will be a tug of war between numerous labor market and inflation reports, and then capped off with the FOMC meeting on March 17-18.

- Friday, March 6th: Non-farm payrolls and unemployment

- Wednesday, March 11th: CPI

- Friday, March 13th: JOLTS, PCE, and Q4 GDP

- Wednesday, March 18th: FOMC meeting and release of the summary of economic projections

For investors, diversification continues to look like a necessary condition of success. There are too many unknowns to try to pick winners with any expectation of certainty. For the time being, the best way to build wealth is to avoid significant losses. Exposure across the full AI ecosystem, along with sectors positioned to benefit from both productivity gains and the fear of wipeout, may help balance opportunity with risk.

Economic Reports

Earnings Releases

Related: Stronger Jobs Cooling Inflation and an AI Jolt Rattle Stocks