Trending

I’ve talked much about the looming pension crisis lately .The bad news is that the problem is approaching a breaking point, and yet everyone seems to ignore it.The good news is we’re starting to get data that might shake people out of their denial.

Stress Testing Retirement Plans

A new Harvard study funded by Pew Charitable Trusts uses “stress test” analysis to see how retirement plans in 10 selected states would behave in adverse conditions. (It’s similar to what the Federal Reserve does for large banks.)The Harvard scholars looked at two economic scenarios, neither of which is as stressful as I expect the next downturn to be. But relative to what pension trustees and legislators assume now, they’re devastating. Scenario 1assumes fixed 5% investment returns for the next 30 years. Most plans now assume returns between 7% and 8%, so this is at least two percentage points lower. Over three decades, that makes a drastic difference. Scenario 2assumes an “asset shock” involving a 20% loss in year one, followed by a three-year recovery and then a 5% equity return for years five through year 30. So, no more recessions for the following 25 years. Exactly what fantasy world are we in?But these models are just that—models. Like central bank models, they don’t capture every possible factor and can be completely wrong. Whether they really help or not remains to be seen. Related: How to Use Business Analysis as a Growth ToolStates That Are Most Likely to Go Bankrupt

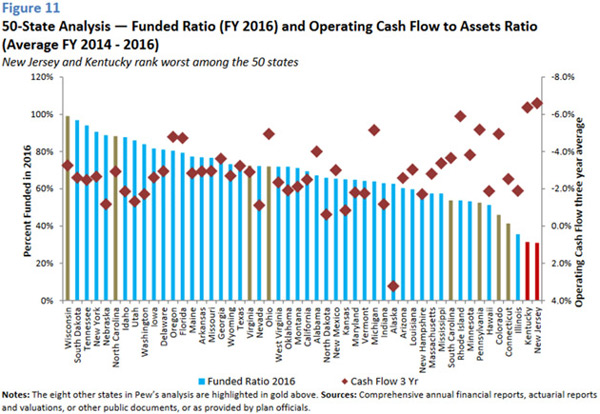

Crunching the numbers, the Pew study found the New Jersey and Kentucky state pension systems have the highest insolvency risk. Both were fully funded in 2000 but are now at only 31% of where they should be. Source: Harvard Kennedy SchoolOther states in shaky condition include Illinois, Connecticut, Colorado, Hawaii, Pennsylvania, Minnesota, Rhode Island, and South Carolina.If you are a current or retired employee of one of those states, I highly suggest you have a backup retirement plan. If you aren’t a state worker but simply live in one of those states, plan on higher taxes in the next decade.But that’s not all.Even if you are in one of the (few) states with stable pension plans, you’re still a federal taxpayer, and that’s who I think will end up bearing much of this debt. That’s right, it is simply debt. Related: When Will Policymakers Admit that Economics Isn’t a Hard Science?

Source: Harvard Kennedy SchoolOther states in shaky condition include Illinois, Connecticut, Colorado, Hawaii, Pennsylvania, Minnesota, Rhode Island, and South Carolina.If you are a current or retired employee of one of those states, I highly suggest you have a backup retirement plan. If you aren’t a state worker but simply live in one of those states, plan on higher taxes in the next decade.But that’s not all.Even if you are in one of the (few) states with stable pension plans, you’re still a federal taxpayer, and that’s who I think will end up bearing much of this debt. That’s right, it is simply debt. Related: When Will Policymakers Admit that Economics Isn’t a Hard Science?