May and June saw economic activity improve relative to the April lows, and we expect that economic growth will be positive in the back half of the year. However, with case growth reaccelerating across the United States, more and more clients have been asking whether or not we think the U.S. economy could get knocked back into recession. While this is not our base case, it is important to understand how it could occur, and what the implications would be for long-term investors.

In the most basic sense, the recession we are dealing with is a cash flow issue – consumers have no income, and businesses have no revenue. This is why reopening the economy is so important, but also, so difficult; if it is done too quickly, we risk seeing a material second wave of infection, but if it is done too slowly, businesses will permanently shut down, making it increasingly difficult to absorb the excess labor supply that was created in March and April. The policy response we have seen over the past few months has tried to address this, but there are limits to how long governments can pump money into the economy.

The risk is that we bring things back online too slowly, and workers have no place to work. This would lead the consumer to come under even more pressure, particularly if fiscal support begins to wane. In this environment, we could easily envision economic growth rolling over; however, any subsequent recession would likely be more structural in nature, and look very different than the sharp deceleration and bounce back seen over the past few months.

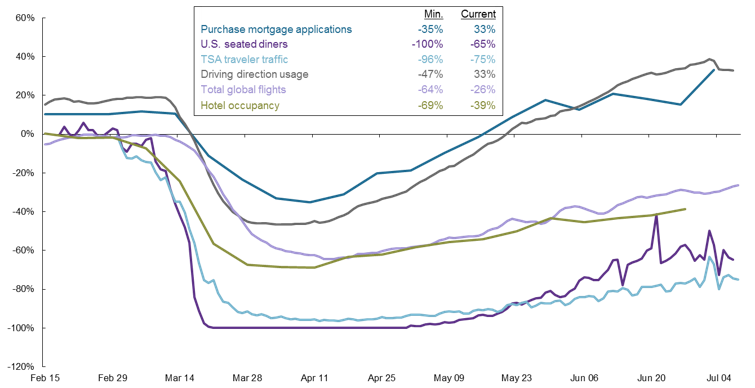

This tension between the health of the population and the health of the economy looks set to persist, and there is no clear answer as to what should be done. Monitoring high frequency economic data – like we show on page 21 of our Guide to the Markets – will be key in order to understand where things stand with respect to the recovery. In the interim, we continue to advocate for an investment approach that focuses on both quality and balance, as we believe this will be the best way to navigate volatility during the coming months.

It will be important to monitor the high frequency data

Year-over-year % change*

Source: Apple Inc., FlightRadar24, Mortgage Bankers Association (MBA), OpenTable, STR, Transportation Security Administration (TSA), J.P. Morgan Asset Management. *Driving directions and total global flights are 7-day moving averages and are compared to a pre-pandemic baseline. Guide to the Markets – U.S. Data are as of July 8, 2020.