Written by: Len Reininger | Advisor Asset Management

As the coronavirus spread throughout the world shutting down economies only to reopen in fits and starts, people’s behavior patterns are changing, especially as it relates to travel, buying/shopping, vacations, higher education, entertainment, overall health practices and consumer consumption. Many impacted sectors are suffering both in the municipal and corporate sectors. The airline sector, hotel sectors, vacation-related sectors, department stores, mass transit systems, toll roads, and others have essentially been dealt a body blow. Most assumptions are that these will be short lived as the impact from the coronavirus wanes, oil prices strengthen with the end of the recession, and a vaccine is found.

But what if behavioral changes are not so quick to return to what they were before the virus and the changes are permanent? What if this causes long-term shocks to certain corporate sectors or governments for which there is no recovery, while strengthening others? What if the inevitable recovery occurs in a way that nobody, or very few, expect?

What if….

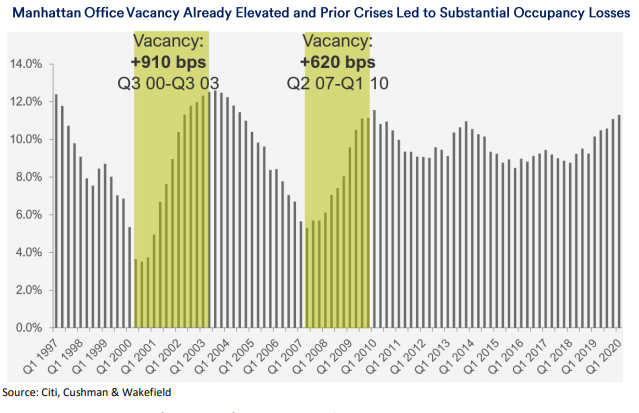

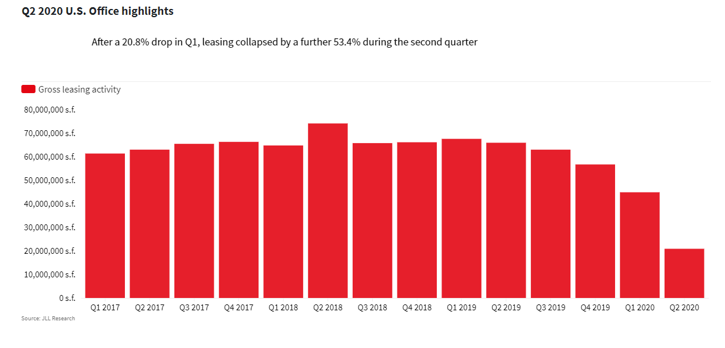

…companies learn that it is not essential for all employees to be at their desk five days a week, eight hours a day. That working from home is a viable cost-effective option which suits employers and employees, not to mention leading to improved health and safety on a permanent basis. Office property values would inevitably decline as would vacancies and rental payments. Moody’s Analytics sees New York City’s Manhattan vacancy rates exceeding 20% in 2021, with rents in New York City plummeting 25%. Additionally, a significant portion of New York City office rents and value is derived from street retail businesses at the base of these assets. Given the multitude of issues with brick and mortar retail tenants, this real estate is likely to see outsized rent and value deterioration. This is not confined to New York City, as major city central business districts throughout the country are experiencing similar trends.

While in the past these trends always recovered, the past has never witnessed the combination of COVID-19 and technology that has made working at home a necessity (at least for now) and viable now and in the future. What if the post-COVID-19 “new normal” reflects a lower need for office space?

What if this pattern is not merely transient? Not only will this likely adversely impact citywide tax revenues, but the impact on mass transit would be profound as commuting becomes a less essential component of full-time employment. Already in New York City, subway ridership is down 77% as of August 3, 2020 compared to 2019 (bus ridership down 42% and Railroad ridership down near 80%), forcing a financial squeeze and begging the federal government for more funds. San Francisco is reporting a ridership drop of 89% as of August 3, 2020, below “baseline.” All over the country, severe declines in transit ridership and revenues due to coronavirus pandemic are being reported with between 70%-90% drops amid efforts at social distancing, a widespread shift to telecommuting, and shelter-in-place orders. What if this represents a blip that isn’t temporary? It would potentially necessitate a permanent change in the funding dynamics away from farebox revenues toward taxes at a time when these very trends would adversely impact the tax base of the major cities and states.

What if…

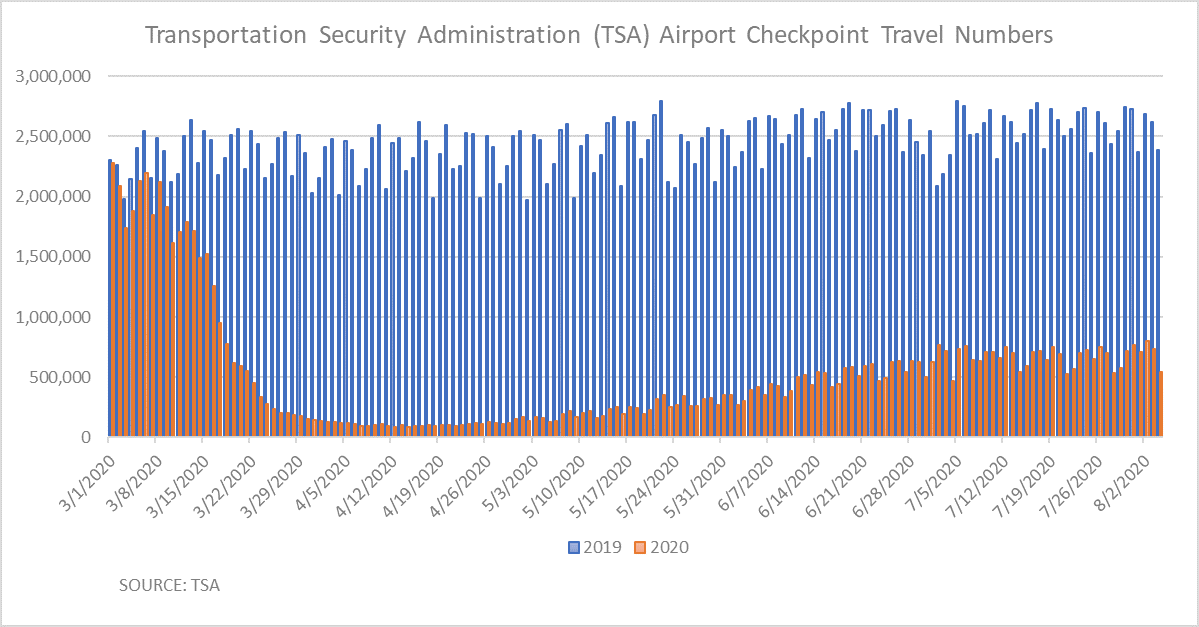

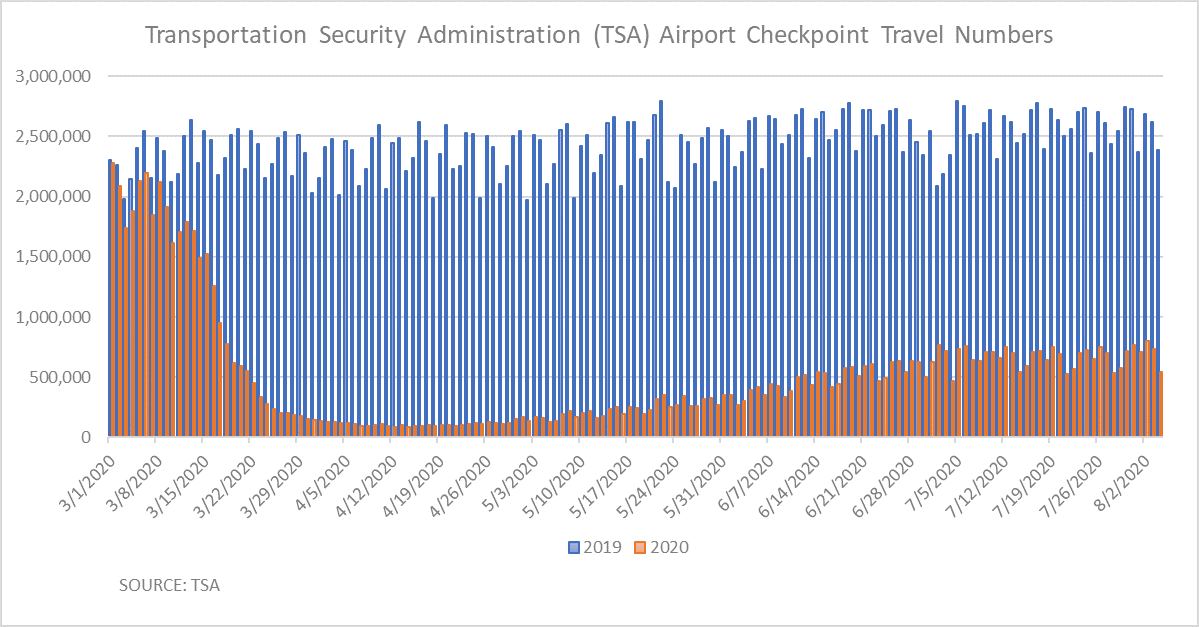

…the severe drop in airline passenger traffic does not recover to pre-pandemic levels. Airline passenger travel is down severely across the board. According to the Transportation Security Administration (TSA), total airport traveler throughput in August (through August 4) is down 72% from 2019 and down 74% for the month of July.

Some airlines believe that a full recovery is not possible until there is a widely disseminated COVID-19 vaccine. Corporate traffic was down 96% in June and all passenger revenue metrics off by 90%. While passenger loads improved since the end of the second quarter, these results appeared to have stagnated and stabilized as COVID-19 infections re-accelerate. The International Air Transport Association believes that airline traffic will not recover from COVID-19 until 2024 but leaves a wide range of uncertainty. What if reduced airline traffic becomes a permanent fixture in air travel and a vaccine is not a panacea for air traffic recovery? Bear in mind corporate travel budgets are expected to be very constrained as companies continue to be under financial pressure even as the economy improves. In addition, while historically GDP growth and air travel have been highly correlated, surveys suggest this link has weakened, particularly for business travel as video conferencing appears to have made significant inroads as a substitute for in-person meetings. According to Finances Online, in a normalized environment, business travelers make up 12% of airline passengers, but they represent as much as 75% of the profit. What if businesses realize that given technological improvements, air travel for personal business meetings and conventions are no longer a priority, cost effective, or even necessary, even in a post-pandemic world (the “new normal”)? Given the probability that U.S. Government assistance will not last forever, serious business model revisions and/or sector restructuring may be necessary, especially as these airlines have significantly increased leverage to boost liquidity. While airports are well capitalized and continue to receive government support, in the longer term, can this situation continue in the face of weakened airlines and passenger levels?

What if…

…the aforementioned reduction in business travel comes to fruition and leaves hotels and convention facilities at greatly reduced occupancy and activity levels? The introduction of COVID-19's "social distancing," cancelations of events and conferences, disruptions in local commerce, and material declines in business and leisure travel have and, per S&P, “will continue to negatively affect convention center...revenue streams.” This, in turn, has led to significant deterioration in hospitality-related revenues such as hotel taxes and other special taxes leading to a deterioration in budgets, reduction in debt service coverage, and weakened local economies. To date authorities have made adjustments to stabilize operations – including reducing budgets, readying available liquidity, furloughing staff, retiring debt in advance of scheduled maturities, and holding off on new debt or capital plans. However, despite these adjustments, there is potential for steep pledged-revenue declines and likely an unstable revenue climate for many years beyond 2021, per S&P. Many of these facilities are supported by pledges to appropriate debt service by the local government. What if these facilities become a cash drain on already seriously strapped governments? What if these facilities become even less essential that they were per COVID? Will appropriations remain safe? For those facilities not reliant on appropriations, but whose debt is supported by special taxes and where the operating risk is associated with the particular convention center or sports authority, S&P has already begun taking negative rating actions since May 22, 2020.

Since mid-March, the U.S. lodging, leisure, and gaming sectors have faced unprecedented declines in revenue and cash flow due to travel bans and restricted consumer activity. As of mid-year, S&P reports that 4% of the sector has defaulted. As of the week ended July 25, 2020, per STR, nationwide hotel occupancy stood at 48.1% with revenue per available room down 54.8% from 2019. The top 25 markets showed lower occupancy of 40.8%. Oahu, Hawaii (22.7%), New Orleans (28.3%) and Miami (30.7%) had the lowest occupancies, with New York City at 36.3%.

What if the supply-and-demand dynamics of group activities are poised for change? Providing safe travel and entertainment outside the home may become more costly and the shifts in consumer and business behavior that occurred during the pandemic may be long lasting. Major resort hotels have reported serious revenue declines. Since the pandemic began in the U.S., economy, midscale, and extended-stay segments have outperformed the industry, and upper upscale and luxury full-service segments have underperformed. Convention centers are at a complete shutdown according to AIPC (International Association of Convention Centers). Given the possibility of a secular shift in business travel, the outlook for convention centers, their operators, and associated hotels remains highly uncertain at this time.

What if…

…the rapid changes in the entertainment sector are not temporary. Video content providers are reporting accelerated subscriber growth and improving margins as consumers are spending more time at home due to the COVID-19 pandemic, resulting in increased engagement with video content. This trend benefits the overall streaming video industry. These services are investing heavily in content and marketing to increase subscribers possible at the expense of traditional movie theaters that are still struggling to re-open. This occurs as studios begin to release films direct to subscription video on demand (SVOD). Will the SVOD companies permanently supplant movie theaters?

What if…

…the feared enrollment drops at the nation’s colleges and universities materialize? Already this year, the higher education sector experienced an unprecedented loss of revenue due to early school closings resulting in some refunds and the loss of auxiliary revenues (dormitory, books, food, fees, parking, athletics, etc.). These losses are material for many institutions. For schools with health care systems, lost revenue from canceled elective surgical procedures could also be significant. If on-campus classes don't resume in fall 2020, and even if they partially re-open, the U.S. higher education sector could continue to face great pressure. Even if enrollment returns, much will be online involving increased instruction costs, and lowered revenue from auxiliary sources. The University of Connecticut is the first major U.S. college to cancel its football season. For many schools, athletics is a major source of revenue. What if recessionary pressures make the high cost of a private education unaffordable, shifting student demand to lower cost institutions? What if auxiliary revenues are shut down or reduced? Even if overall enrollment grows, net tuition and other student revenue will likely fall as the mix of more students attending lower-priced colleges and households struggling to pay for higher education could lead to a decline in key student revenue streams even if enrollment increases. Four-year public and private universities with strong brands, healthy endowments/liquidity, and historically strong application/acceptance/matriculation trends, should hold their own in terms of student demand and net tuition revenue. Difficulties could accelerate for higher-priced colleges heavily dependent on tuition revenue with less recognized brands. Some colleges will likely benefit from students wishing to stay closer to home in light of the pandemic but, higher education bonds secured by auxiliary revenues are something to be watched, in our opinion.

What if…

…the apparel retail sector continues its transition from traditional mall shopping to specialty stores and online shopping? 2020 is on track to have the highest number of retail bankruptcies in a decade, according to S&P Global Market Intelligence. Forty-three retailers have filed for bankruptcy so far this year, including many companies saddled with debt or struggling to resonate with shoppers before the pandemic, per S&P Global Market Intelligence. Essentially, those companies that had trouble reaching customers online as e-commerce brands won more of young shoppers’ attention and dollars, while those saddled with debt, or those with limited liquidity, are in the greatest danger. Those retailers that were already weak had the bankruptcy process accelerated for them by the pandemic. The temporary shuttering of stores for weeks forced American’s spending habits to change as people coped with pay cuts and job losses or had less of an appetite for new clothing because of working from home and attending few social gatherings. They also aggressively took up online shopping and delivery. Traditional back-to-school shopping for apparel retailers could also be in jeopardy. Families’ shopping lists for clothing could be shorter minimal as this could give sway to other kinds of items, such as laptops and headphones, as school districts plan for staggered schedules or remote learning. If the company is heavily indebted, a mall-based property, or not an essential retailer, there is increased risk. Retail does not appear dead as there was a pickup as the economy started reopening, but it is changing along with new spending patterns.

The sudden and severe disruptive effects of coronavirus lockdowns and social distancing have led to a massive change in households' discretionary and non-discretionary consumption patterns in the U.S. While some may reverse back after health-related fears abate, many could become permanent as consumers favor the convenience, efficiency or cost effectiveness of new types of consumption. Three behavioral shifts could drive the long-lasting changes in consumption: accelerated digitalization, a greater share of time and consumption spent at home, and a transformation of travel, entertainment and leisure activity. This may lead to a “new normal” from which many sectors may not survive in a recognizable form.

Related: Why Emerging Markets Now?