Trending

Holiday-style trade, narrow ranges, and low volatility have been this week’s theme in the S&P 500 thus far. What is the slow chug leading up to, with Friday's BIG Jobs Number?

It seems like we just got the last jobs number yesterday, but here we are again awaiting the big data drop on Friday at 8:30 AM ET. The market consensus seems to be for 700K jobs added during the month of June, with some consensus indicators showing 690K. The expectations have seemed to increase over the last week, as expectations have risen from ~ 660K.

Last month, the Non-Farm Payroll number missed expectations; printing at 559K versus 645K expected, and the US Equity and bond markets did not care, as both marched higher.

But that was so last month. How could the markets behave on Friday’s data release?

I tend to avoid having leveraged open positions heading into big data releases like NFP and CPI. Longer-term swing trades and position trades are just fine to hold onto, however.

There is some seasonality for the S&P 500 to move higher heading into the 4th of July. Some analysis shows getting long 2 days prior to the release yields certain results over X amount over a number of years, and other analysis seems to show getting long the day before is good too. You can read about what veteran Trader Larry Williams had to say about this last year.

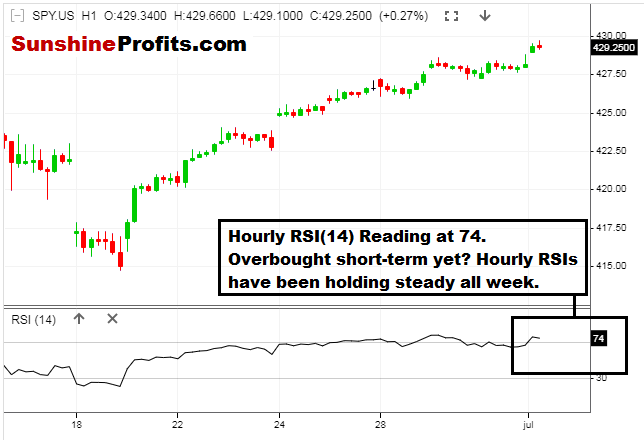

Analyzing the SPY today for the ETF Traders out there:

Figure 1 - SPDR S&P 500 ETF February 18, 2021 - July 1, 2021, 10:20 AM, Daily Candles Source stockcharts.com

Looking at the SPY, we have been higher eight out of the last nine trading sessions! That is a rare feat in the index. Given the recent selloff to the 50-day moving average that we were waiting for, it does make sense that we have continued higher, but eight out of the last nine sessions is rare. This is just some food for thought. In addition, we are seeing Daily RSI(14) at 67, which could indicate the SPY approaching short-term technically overbought levels in the trading days ahead. It is not all that often where the SPY will hold an RSI(14) Daily level above 70 for a lengthy period.

Drilling down further to the hourly candles, I notice some indications of short-term overbought levels (well, we have been higher in eight of the last nine trading sessions, after all!).

Figure 2 - SPDR S&P 500 ETF June 15, 2021 - July 1, 2021, 10:45 AM, Hourly Candles Source stooq.com

There aren’t too many surprises here when looking at the hourly chart. The S&P 500 has been moving higher steadily, and it feels like we are headed for a short-term volatility spat (either higher or lower) with the NFP data release on Friday.

Let’s keep in mind that this is a Holiday week in the US. Trading volumes tend to dry up, and slow moves higher can be a prevailing theme during holiday-style trading. US equity markets are closed on Monday, July 5th in observance of Independence Day in the US. Some futures products will trade on July 5th with abbreviated trading sessions. You can see the Holiday trading hours for the CME here. Be sure to know the holiday trading hours for your product!

Heading into Friday, I am not expecting much in the way of market fireworks before the NFP data release. The slow grind higher has been the theme as market participants await the big NFP jobs data.

Let’s recap the markets we are following and see if there are any key levels or developments in each for Premium Subscribers.

Not a Premium subscriber yet? Go Premium and receive my Stock Trading Alerts that include the full analysis and key price levels.

Thanks for reading today’s article. Have a great Independence Day Weekend!

Related: VIX at Pre-Pandemic Levels, Summertime Volatility Possible?

The views and opinions expressed in this article are those of the contributor, and do not represent the views of IRIS Media Works and Advisorpedia. Readers should not consider statements made by the contributor as formal recommendations and should consult their financial advisor before making any investment decisions. To read our full disclosure, please click here.