Written by: Meera Pandit

While markets are likely to experience volatility in the lead up to and the aftermath of the election, ultimately, it’s policy, not politics, that matter most for the economy and markets in the long run. One policy proposal that has garnered the attention of most is an increase in the corporate tax rate.

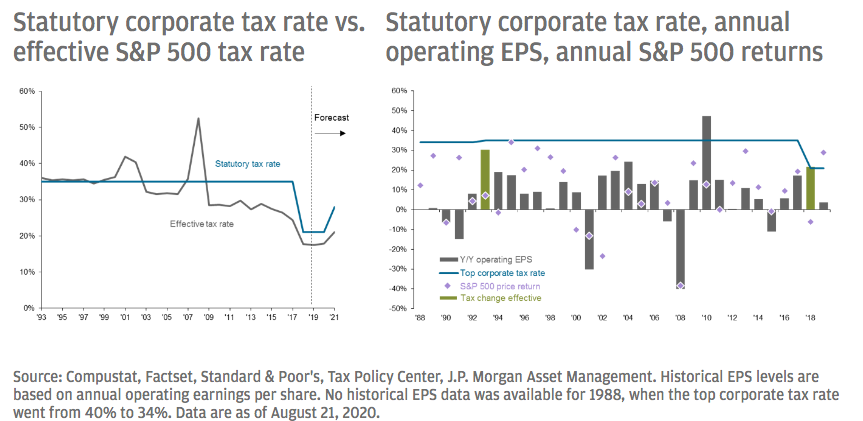

From 1993-2017 the top corporate tax rate was 35%, until the 2017 Tax Cut and Jobs Act (TCJA) reduced it to 21%. Democratic nominee Joe Biden has proposed to partially reverse this cut, increasing the top corporate tax rate from 21% to 28%. This would bring it in line with the OECD GDP-weighted average of 26.53%. However, most companies do not pay this top rate, and the effective tax rate is typically below it. In 2019 it was 17.5%, and based on the relationship between top rates, effective rates and nominal GDP over time, we estimate it could be north of 21% with a partial tax hike. This could reduce S&P 500 operating earnings per share by roughly 7 USD, disrupting, but not reversing the fragile profits recovery. This compares to the 12 USD boost in operating earnings per share attributable to tax cuts in 2018, the first year the TCJA was in effect.

Biden has not suggested a firm timeline on a corporate tax hike and, if elected, he would, of course need the cooperation of Congress to pass one. Moreover, even if Democrats were to gain control of the White House and both houses of Congress in November, they might delay any tax hike until 2022, when the economy should be on a firmer footing and financial markets begin to focus on the need to address the sharp deterioration in public finances.

However, it should be noted that a corporate tax hike alone would not have a meaningful impact on federal deficits and debt. In 2019, corporate taxes only accounted for 7% of federal government revenues, while individual income taxes raised 50% according to the CBO. The Tax Foundation estimates that the proposed corporate tax hike could raise 1.3 trillion USD over a decade, but the budget deficit is already 2.8 trillion USD for just the first 10 months of fiscal year 2020. Therefore, to have a meaningful impact on improving federal finances, a corporate tax hike would likely be part of a broader tax package.

While a hike in the corporate tax rate would be painful for companies, it would not be catastrophic. After all, 28% is still below the top rate of 35% it was from 1993-2017, and before 2018, the top rate had not been as low as 28% since 1940. Companies have proven to be able to be profitable in this tax environment for decades. The last corporate tax hike was in August 1993, when the rate was raised modestly from 34% to 35%. In 1993, operating EPS grew 30.3% y/y, and another 19.1% y/y in 1994.

A corporate tax hike too soon could hurt the nascent profits recovery, but eventually it does seem likely to be part of a broader tax package to tackle the deterioration in public finances. However, tax hikes coinciding with an upswing in economic growth and stabilizing profits could minimize the damage to both.