Trending

Written by: Jack Manley

In recent months, the prospects of higher inflation has become front of mind for many investors. The enormity of the fiscal and monetary response to COVID-19 means that, for the first time in decades, the U.S. may experience a more robust inflation backdrop than has been observed in recent years; and with the Federal Reserve adopting an average inflation targeting framework for future policy decisions, this inflation may be tolerated for longer than would have otherwise been the case.

Of course, with unemployment still severely elevated and GDP depressed, the threat of rising inflation is not an immediate one. However, if inflation does materialize during or after the economic recovery, investors will want to know the implications for portfolio construction.

There are a number of different assets that could hedge against – or even benefit from – rising inflation. Gold, and commodities more broadly, have served as a strong hedge against inflation, with a 1% increase in CPI historically translating into a 10% increase in the price of a basket of commodities. For investors with an appropriate risk tolerance and sufficient capital, direct investments in real estate typically generate an income stream that keeps pace with inflation, because inflationary pressures can be directly passed on to renters. An investment in infrastructure will function similarly for similar reasons, with the ROE of regulated utilities typically linked to inflation. Finally, inflation-linked bonds see the principal indexed directly to inflation, and as a result, the coupon payment will rise if inflation picks up. However, investors should be aware that if interest rates rise for reasons other than inflation, these bonds will underperform.

In this vein, it is perhaps of equal importance to know what will perform poorly in an inflationary environment – namely, higher duration fixed income. If inflation – or inflation expectations – start to rise, bond yields will likely rise contemporaneously. This means that while investors may find some comfort in duration over the short-term as a hedge against equity market volatility in uncertain times, longer-term investors should recognize that duration may work against them should inflation rear its ugly head once more.

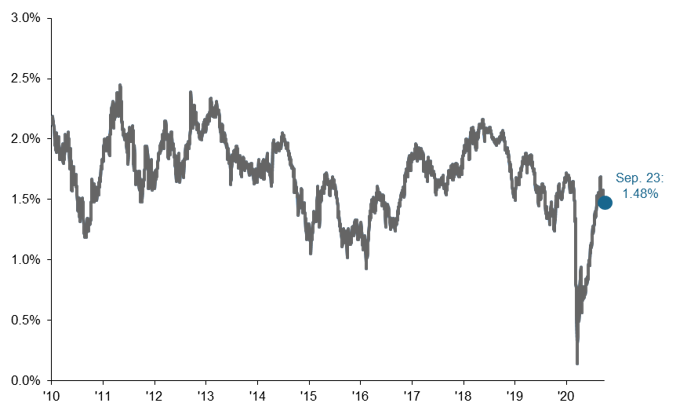

5-Year breakeven inflation rate

Percent, not seasonally adjusted