Trending

Written by: Brian Clark | Knowledge Leaders Capital

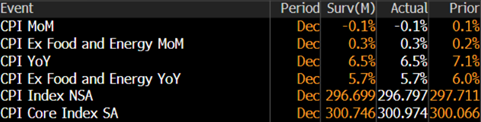

The December U.S. Bureau of Labor Statistics’ Consumer Price Index came in exactly as expected according to Bloomberg’s survey of economists. Headline CPI came in at -0.1% month over month and 6.5% year over year, and Core (CPI Ex Food and Energy) came in at 0.3% month over month and 5.7% year over year respectively, the lowest rate of inflation since October 2021.

This is a good report that represents real progress in stemming the tide of inflation and comes on the heels of recent reports that showed inflation cooling from its peak in 2022 (9.1% year-over-year Headline and 6.6% year-over-year Core). Below, I look at how inflation has changed recently.

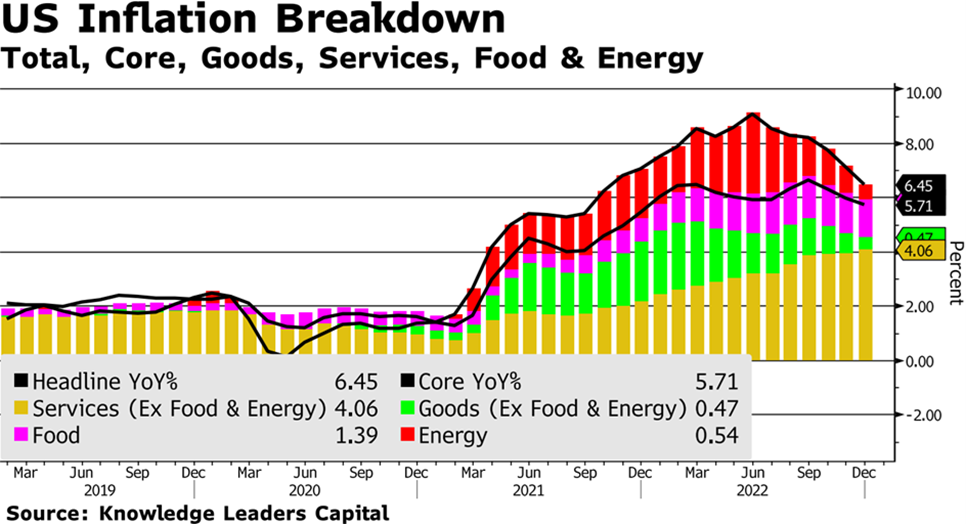

Inflation overall is coming down steadily led by energy and goods (ex food and energy) prices. Current inflation figures have come down considerably over the last several months.

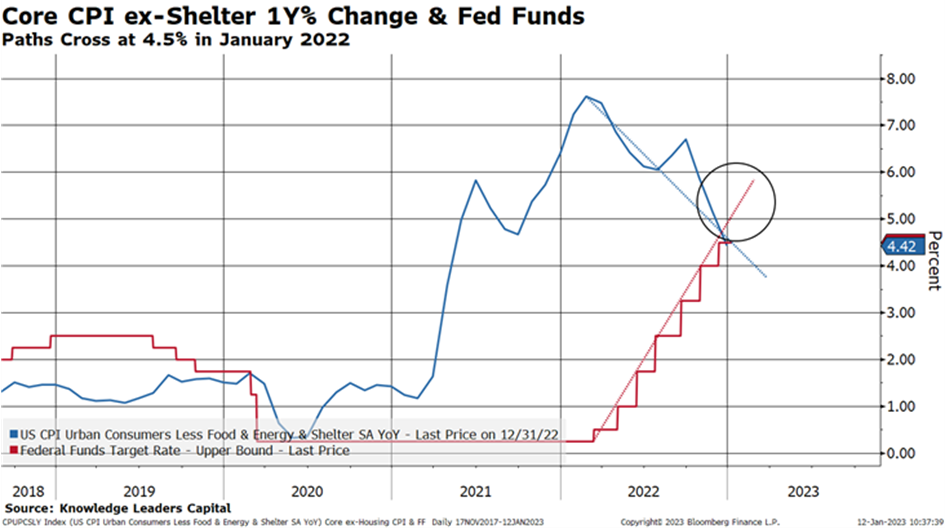

While there are multiple ways to measure inflation, the one that the Federal Reserve says its cares about more than headline CPI is Core CPI ex Shelter. This measure of inflation has come down so much recently that it is now below the Fed’s primary policy tool, the Federal Funds Rate. This means that the Fed has met one of its criteria for pausing: rates are above inflation.

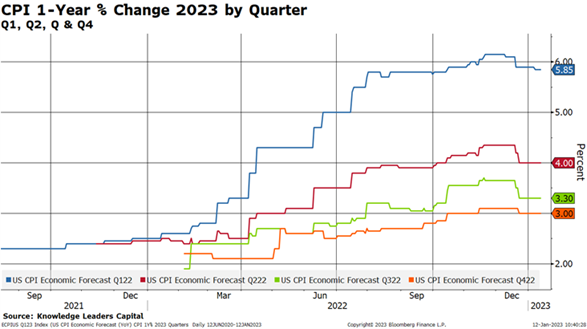

Suggesting that the Fed has entered restrictive enough territory to ease inflation down in 2023, the glide path as shown by economists’ forecasts for CPI is for inflation to be down each quarter and down to 3% (annualized rate) by the end of 2023.

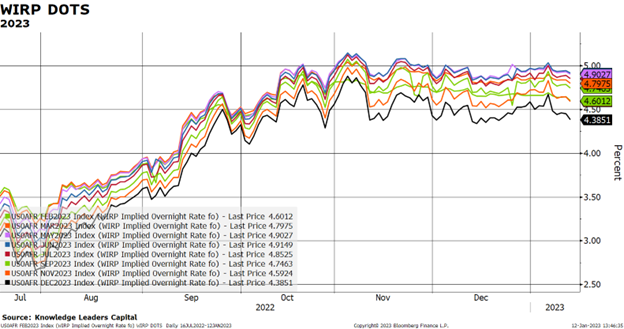

Looking at OIS-based interest probabilities, the market sees a 40% chance the Fed raises 25bps in February, but a 100% chance they go 25bps by March 2023. In addition, the market has priced a 66% probability of another 25bps rate hike by May 2023 and then only a 64% probability of a 25bps rate increase by June. The likelihood the Fed takes rates to 5% by May is about 80%–still high but well down from the 85% chance the market was pricing in a cumulative 75bps rate hike by May.

Further, recent comments by Philadelphia Fed President Patrick Harker and Boston Fed President Susan Collins that they favor 25 basis point hikes going forward suggest a plateauing of rates sooner rather than later. Hence, the market is convinced the Fed has overtalked the likelihood of getting the terminal rate over 5%, and rhetoric of 5.5% seems to be in direct odds to the market. Incidentally, analysts noticed that Fed Chair Powell didn’t avail himself the opportunity to talk down the market at a recent speaking engagement on Central Bank Independence in Stockholm this week.

This all suggests that since November the market has lowered its expectations for rate hikes that are likely in the next few meetings. This may be the strongest leg of the argument that risky assets are rising for good reason.