Trending

Written by: Jordan Jackson

As widely anticipated, the Federal Open Market Committee (FOMC) voted to leave the Federal funds rate unchanged at a target range of 5.25%-5.50%. The statement language was largely unchanged from September, though language around data were firmer. The description of recent economic activity was upgraded from “solid” to “strong” and the pace of job gains improved from “slowed” to “moderated”, reflecting the strong 3Q GDP print and uptick in hiring in recent months. Moreover, the statement maintained the language in “determining the extent of additional policy firming that may be appropriate”, allowing for some flexibility to tighten further.

During the press conference, Chairman Powell remained well balanced. On a few occasions, Powell suggested that risks were now more two-sided i.e., the Fed remains concerned about inflation though given the lags in monetary policy and the broader tightening in financial conditions, this should lead to a period of sub-trend growth and allow inflation to come down without further action. Of course, he emphasized the need to see a trend in the data to feel confident the labor market is headed further into balance and inflation is continuing toward their 2% objective. However, he made clear that committee is not thinking about rate cuts, suggesting the “higher for longer” mantra remains intact.

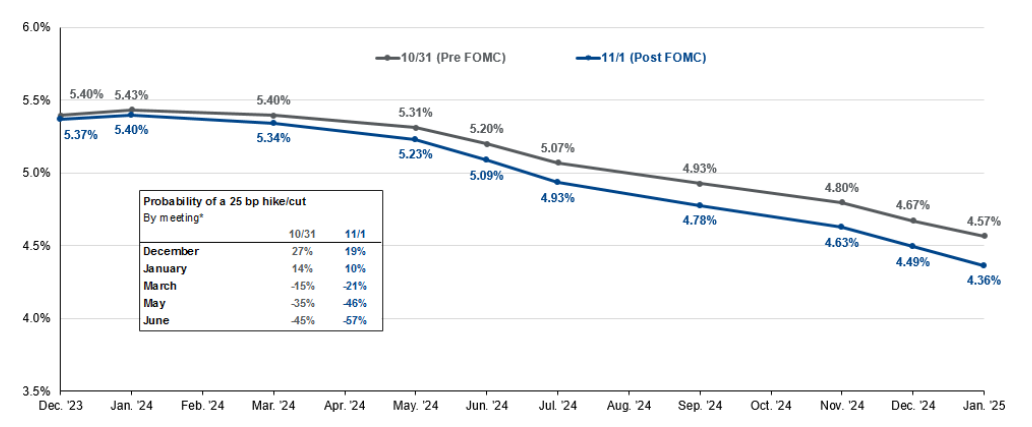

Chairman Powell’s comments during the press conference appear to be viewed as slightly dovish given market reaction. Equities rallied and yields fell following the Chair’s comments. The market is now pricing in a peak terminal rate of 5.40% in January, implying a 29% chance of another hike this cycle, and now three full cuts by year-end 2024 with a ~62% chance of a fourth. The Fed will remain data dependent going forward, and having now paused hiking rates for two consecutive meetings this suggests they are willing to exercise patience and proceed carefully. While a reacceleration in growth and/or inflation could prompt another rate hike either in December or early next year, short-term bumps in a downward trending economy likely keep the Fed on hold well into 2024.

U.S. implied policy rates

Federal funds futures

Source: Bloomberg, J.P. Morgan Asset Management.