Trending

Written by: Hitendra D Varsani and Waman Virgankar | MSCI

- Global equities continued to rally in Q4 2020. Many regions reached all-time highs, as high-beta and value factors and cyclical sectors outperformed. For USD and EUR investment-grade corporate bonds, it was carry and value.

- We revisit factor selection for different macroeconomic regimes to indicate potential scenarios for 2021. Historically, recovery in economic indicators has been positive for low-size and value exposures.

- As we enter 2021, MSCI’s adaptive multi-factor model pointed to an overweight of low size and value, an underweight of quality and low volatility and neutral on momentum and yield relative to an equally weighted factor mix.

In this two-year-anniversary edition of Factors in Focus, we reflect on the historical relationships between factor returns and macro cycles, which have provided useful information for investors looking to take an active stance on factor exposures based on their outlook. Before we present our findings, however, we highlight recent pure-factor performance from the MSCI Global Equity Market Long-Term (GEMLT) risk model, single-factor index performance, followed by sector performance. We find indexes and sectors that had positive exposure to value and negative exposure to momentum outperformed.

Q4 Finished a Tumultuous Year with a High-Beta Rally

Equities worldwide rallied in the last quarter of 2020, amid hopeful news of effective COVID-19 vaccines. Also in the fourth quarter, Joe Biden won the U.S. presidential election and the U.K. exited the European Union. The MSCI ACWI Index was up 14.8% for the quarter, reaching an all-time high on Dec. 31 and finishing 2020 up 16.8%.

While equity markets demonstrated resilience during a period of high economic uncertainty, factor rotation intensified in Q4. Momentum, which had stretched valuations at the end of Q3, pulled back; and book-to-price, which had underperformed for a majority of the year, added gains. Investors favored high-beta stocks over low-beta stocks.

Pure-Factor Performance in Q4 — Technical Factors Pulled Back

Factor performance of the MSCI Global Equity Model (GEM+ESG) pure factors from Sept. 30, 2020, to Dec. 31, 2020.

A Boost for Value and Low-Size Factor Indexes

Value-factor indexes across global, regional and international markets were given a boost, alongside cyclicals, as investors increased their expectations for higher growth and a recovery in businesses hardest hit by the pandemic. The scale of the value rotation was sharp: the seventh-highest quarterly active return (7.3%) since 1997, and comparable to the value recovery in Q2 2009 (8.3%). Within developed markets, large-cap stocks that had dominated for much of 2020 took a step back, and low-size stocks outperformed in Q4 (up 2.9% vs ACWI). The small-over-large outperformance was most pronounced among small caps (the MSCI ACWI Small Cap Index’s active return was 9.0%).

International equities (represented by the MSCI World ex USA Index) outpaced U.S. equities (represented by the MSCI USA Index) by 280 basis points (bps). While high dividend yield underperformed within U.S. stocks (-360 bps), among international equities it delivered an active return of 90 bps.

Speaking of income, the MSCI USD and EUR Investment Grade (IG) Corporate Bond Indexes continued their rally from last quarter, supported by 4.6% and 2.2% respective spread returns (i.e., in excess of their duration-matched U.S. Treasury/German bund returns). Among excess returns in corporate-bond factor indexes, carry within USD corporate bonds outperformed by 590 bps compared to a relatively moderate 80 bps in EUR.

Finding Value in Sectors Through MSCI FaCS

The strong quarterly performance of global cyclical sectors — namely, financials, materials and industrials, alongside energy — might indicate investors were increasingly confident of a synchronized global recovery in 2021. Viewed through the lens of MSCI FaCSTM, these sectors, with the exception of industrials, also had high exposure to the value factor. In other words, not only did value stocks outperform within sectors, but so did value sectors outperform other sectors, identified by the green color-coded positive value exposure in the exhibit below.

MSCI ACWI GICS Sector FaCS Exposures

Q4 Special Focus: Factor Performance and the Economic Cycle

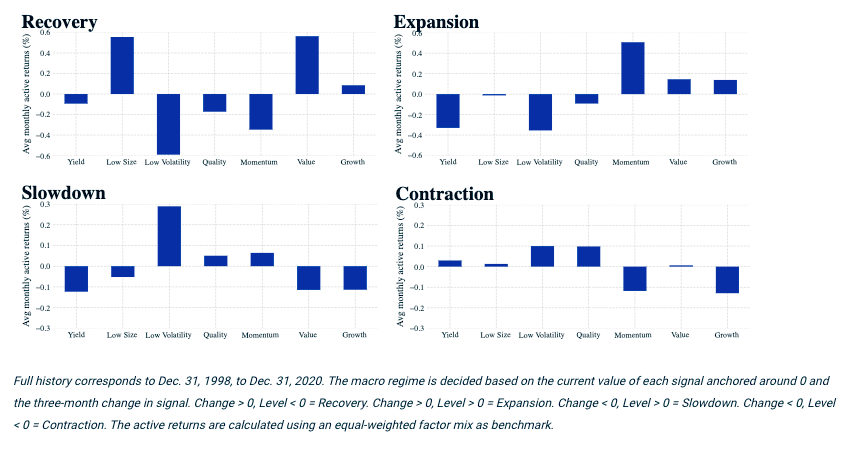

One key lesson from 2020 was that managing factor exposures during the sharp deterioration and recovery in economic activity was more important than selecting stocks, as pointed out in our “Five lessons for investors from the COVID-19 crisis” blog post. While 2021 may return to a more normal environment, we know from history that changes in the economic cycle have had a significant impact on factor performance. In last quarter’s Factors in Focus, we showed the impact of inflation and real rates on factors: Notably, higher inflation and/or higher real rates had a positive relationship with active value returns. In this edition, we revisit macro-conditioned factor performance based on economic indicators.

We use three indicators to measure the state of the macroeconomic cycle — the Chicago Fed National Activity Index (CFNAI), Federal Reserve Bank of Philadelphia’s ADS Index and Institute for Supply Management’s PMI. For each of the indicators, we calculate the average one-month active forward return (with respect to an equal-weighted factor mix) for each factor in each state and then average over all three indicators. These average returns are plotted in the exhibit below.

In short, we see that low size and value outperformed in recovery, momentum in expansion, low volatility in slowdown and low volatility/quality during contraction.

What Do Economic Indicators Tell Us About Factor Returns over the Subsequent Month?

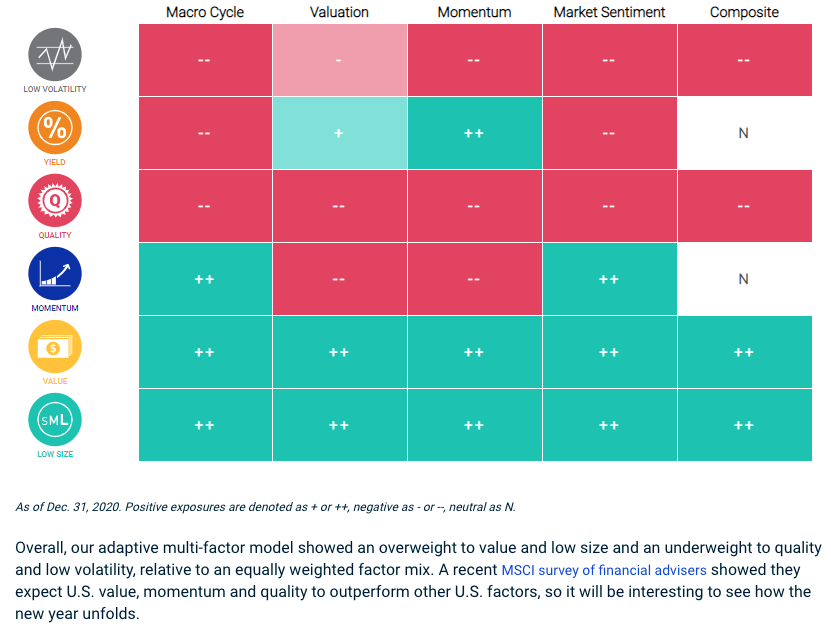

MSCI’s Adaptive Multi-Factor Allocation Model

Our adaptive multi-factor framework is a model designed to analyze decisions about tilting toward factors. Our research has shown that factors were sensitive to changing market conditions and suggests there is value in taking a holistic approach to factor assessment that encompasses not only the macroeconomic environment as shown above but also factor valuations, recent performance trends and risk sentiment.

As of Dec. 31, 2020, our adaptive multi-factor model showed the following exposures across the four pillars: .

- The macro-cycle pillar indicated an expansion and thus overweighted value, low size and momentum, based on the CFNAI, Federal Reserve Bank of Philadelphia’s ADS Index and PMI.

- The valuation pillar overweighted value, low size and yield, based on the valuation gap compared to an equal-weighted factor mix in the context of nearly 30 years of a factor’s history.

- The momentum pillar selected value, yield and low size, based on the last three months’ relative performance.

- The market-sentiment pillar showed a risk-on environment, based on the Cboe Volatility Index® (VIX) term structure and credit spreads, resulting in an underweight to low volatility, yield and quality and overweight to momentum, value and low size.

Exposures from MSCI’s Adaptive Multi-Factor Allocation Model