Trending

Written by: Taymour Tamaddon | T. Rowe Price

Returning to a “normalized” environment could take longer than many anticipate.

Key Insights

- With so much uncertainty still surrounding the coronavirus pandemic, necessitating ongoing social distancing, it is difficult to gauge just how long this acute economic disruption might last.

- We believe current consensus expectations may be overestimating the trajectory for improvement and that the time frame for returning to a “normalized” environment could be longer than anticipated.

- It is difficult to determine exactly when we might emerge from the current crisis, as a range of potential best, worst, and base case scenarios remain in play, but how quickly this happens and when we can get to a normal recessionary environment is crucial in our view.

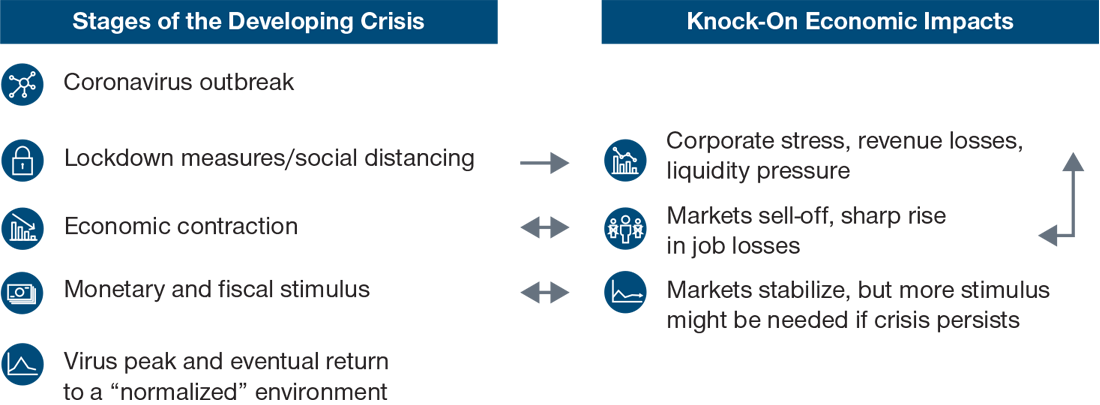

The severe threat posed by the novel coronavirus to public health and the drastic measures taken by governments to contain its spread have had a significant knock‑on impact on the U.S. and global economies. With so much uncertainty still surrounding the pandemic, necessitating ongoing social distancing measures, it is difficult to gauge just how long this acute economic disruption might last. Accordingly, we believe that current consensus expectations may be overestimating the trajectory for improvement and that the time frame for returning to a “normalized” environment will potentially take longer than is currently anticipated.

Social Distancing Is Central to the Near‑Term Outlook

Trying to determine when a potential peak in the crisis might occur and how long it might take until we get to a normalized environment is highly dependent on how long social distancing measures remain in place, both in the U.S. and globally. While the impact of these measures on containing the outbreak in certain cities like New York has clearly been felt, the same success cannot necessarily be assumed for the rest of the country. Each state has taken its own approach to social distancing, implementing it at different times and with varying levels of support and adherence by the public. Therefore, it is difficult to get an accurate sense of how effective these measures will prove at a nationwide level.

The “Best‑Case” Scenario—Peak in Mid‑May

Given this uncertain picture, near‑term consensus expectations appear overly optimistic in our view. Currently, the market is anticipating a peak in the number of new coronavirus cases being reached around mid‑May 2020, after which the number of new cases is expected to rapidly decline, with a return to a more “normal” market environment anticipated by early June 2020.

Our view is that this is a likely best‑case scenario, with around a 15%–20% chance of playing out. Our main concern is that the market appears to be looking toward countries like China, Korea, and Singapore, and the effectiveness that social distancing efforts have had in these countries, and automatically assuming that this success will be replicated in the U.S. We are less optimistic about the near‑term effectiveness of social distancing efforts across the U.S., and so we are also less optimistic about the expected time frame for a return to a normalized environment.

The “Base Case” Scenario—Peak in Late May/Early June

A more reasonable base case scenario, in our view, one that we put at around a 60% chance of playing out, is that we see a peak in new cases in late May/early June and start to return to a more normal environment somewhere around mid‑ to late July. This normalcy is likely to last until around mid‑December 2020. However, around this time, during the northern hemisphere winter, there is a risk that the coronavirus could migrate back from the southern hemisphere, so we see social distancing programs potentially becoming relevant again, perhaps not nationwide, but as and when required, to avoid a second wave of the coronavirus taking hold. This environment is likely to continue until around the end of March 2021, in our view.

The “Worst‑Case” Scenario— a Longer Recovery Period

A potential worst‑case scenario would be one in which a peak in new coronavirus cases is reached at some point, but the number of new cases does not come down to a low enough level to give people the confidence to begin returning to work, going to restaurants, traveling again, etc. At this stage, we do not have any clarity on what an acceptable level of new cases might be for people before they feel confident to return to work in a significant way. This is the most negative scenario in our view, and we attach a roughly 15%–20% chance to this potential outcome. If this were to play out, the environment would not be as bad as the acute economic disruption we are currently in, but it would ensure that we remain anchored in a severe economic downturn for at least the next nine months.

Getting to the Other Side of the Crisis Is What Matters Most

In the absence of a coordinated, nationwide testing program, with an effective, widely available treatment still some way off and with social distancing measures still in place, there is still much uncertainty surrounding the coronavirus pandemic and its economic impact.

One key aspect that we are spending a lot of time trying to understand is just how quickly we might be able to get to a normal recession. As strange as this might sound, it is one of the most important questions to answer. We are currently in such an acute economic downdraft that the shape of a potential recovery—whether it is “V” or “U” or any other—is not the most pressing issue in the here and now.

We are clearly heading into a recession on the other side of the crisis. Just how quickly we can get to this normalized environment and through the current period of extreme economic dislocation is crucial.

WHAT WE’RE WATCHING NEXT

We are spending a lot of time talking to management teams about company budgets, and information technology (IT) budgets, in particular. This tends to be one of the first areas to be cut in a downturn, so understanding the likely magnitude of cuts, overall, as well as any specific areas of focus within IT, will help to ensure that we are favorably positioned in companies that are less vulnerable to budget cuts while avoiding those that appear most exposed.