Trending

260 Fed meetings will occur between the issuance and maturity of a 30-year Treasury bond. There will be 260 times when the Fed raises, lowers, or does nothing with Fed Funds. In that perspective, why should a bondholder care what the Fed does or doesn’t do at the next few meetings? We ask the question because we get many questions from potential bond investors on whether they should buy bills, notes, or bonds based solely on expected Fed policy.

Many inquiries are concerned about buying bonds too soon because they fear the Fed may still raise rates once or twice. While the Fed is an important variable in the performance of all bills, notes, and bonds, its actions significantly impact shorter-term bills and have less influence on longer-term notes and bonds.

To better appreciate what drives yields across the spectrum of Treasury securities, we share some evidence on what factors influence bill, note, and bond yields. This exercise will help better assess which maturity bond may best serve your needs while effectively reflecting your economic and Fed outlook.

For a refresher on bond basics, we recommend reading our article Treasury Bonds FAQ. Additionally, watch our YouTube appearance, Bonds Explained Simply, with Adam Taggart of Wealthion.

Bond Market Lingo

Before moving on, it’s worth a quick review of what constitutes bills, notes, and bonds.

Bills encompass all securities issued with a maturity of one year or less. They are sold at a discount to par and do not pay a coupon. Bill investors instead receive the difference between the purchase price and par at maturity.

Notes and bonds pay coupons and are initially auctioned at or very close to par. Bonds include all maturities of more than ten years, while notes include anything between one year and ten years.

Short-Term Bills Are Bets on the Fed

The shorter the bond term, the greater its yield is influenced by the Federal Reserve. Therefore, the most significant factor is the Federal Reserve if you are considering anything between a one-month and six-month bill. Of course, what the Fed does or doesn’t do depends on economic data and the financial markets.

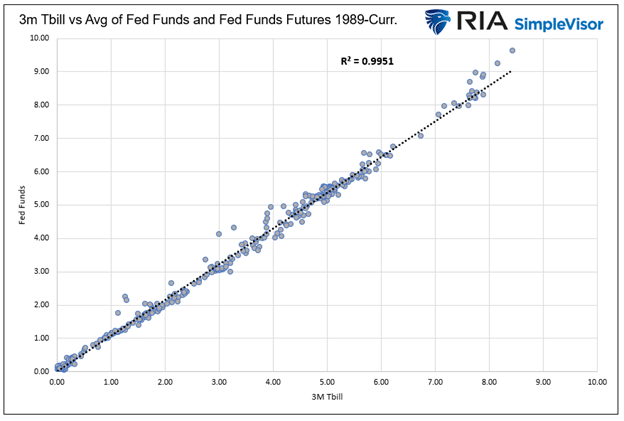

The graph below shows that 3-month Treasury bill yields are nearly perfectly correlated with the average of Fed Funds and the market implied forward Fed Funds rate (rolling three months Fed Funds futures contract).

For short-term bill investors, the most critical factor in deciding which maturity bill to buy is your expectation of monetary policy in the coming meeting or two.

If you think future expectations for the Fed Funds rate are too high, you are best served to lock in the longer six-month yield. Conversely, if you think they are too low, buy a shorter three-month bill and another three-month one in three months. If you are correct, your combined return will exceed the six-month yield.

The equation below closely approximates the market’s future yield expectation. In the example, we solve for rate A (a 3-month yield, three months from now). We assume a 5.00% 3-month bill and a 5.20% 6-month bill:

(3 X 5%) + (3 X A%) = (6 X 5.2%)

15 + 3 X A = 31.2

3 X A = 31.2-15 = 16.2

A = 16.2/3 = 5.40%

If the future 3-month bill yields 5.41% or more, you are better off buying the 3-month bill and buying a second one when it matures. If not, the six-month bill is the better decision.

Long-Term Notes and Bonds

Unlike bills, notes and bonds better reflect longer-term economic and inflation expectations.

Treasury investors, like all investors, strive to earn a positive real return. Such means they should buy assets that provide a positive return after subtracting inflation. They want to increase, not decrease, their purchasing power.

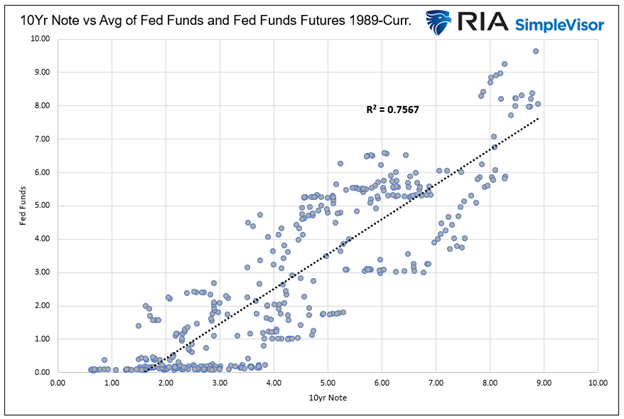

Given what longer-term bond investors seek, they tend to focus more on the economy and inflation and less on what the Fed will do at the next one or two meetings. That said, Fed Funds are still a significant factor, as shown below. The graph below plots ten-year notes versus Fed Funds.

The R-squared (.75) is statically high but far from the near-perfect correlation we showed with 3-month bills. While the relationship is strong, there is a wide variance in the instances versus the trend line. If you recall, there was minimal variance in the 3-month bill vs. Fed Funds plot.

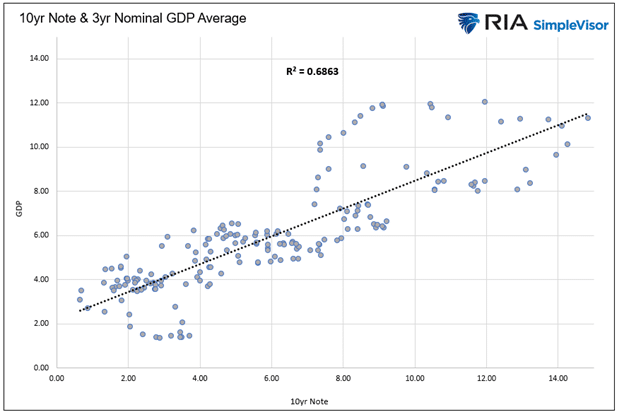

The following two plots show that ten-year yields have near equally strong relationships with three-year GDP and inflation trends.

Yield Curves

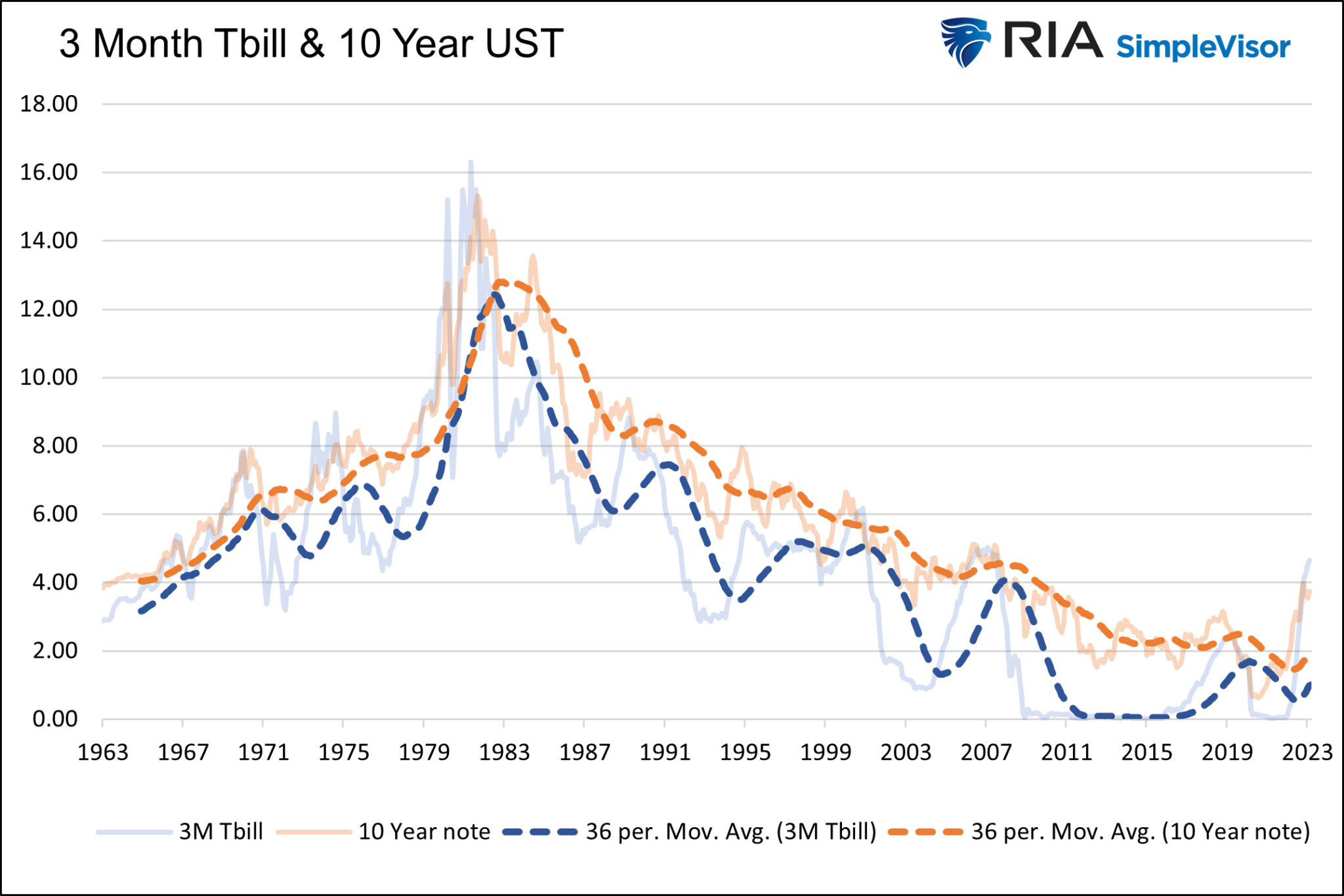

The graph below compares the 3-month T-bill and 10-year note yields and their moving averages.

While both securities trend in the same direction, the change in the yield difference over time is volatile. To highlight better, we show below the 3-month bill/ 10-year note yield curve. The curve is the difference between the two yields.

We hope this is your aha moment. When buying a bill, note, or bond, the bet is on the Fed. But note and bond investors, unlike bill investors, also care about future economic trends. The sharp gyrations in the graph above make that abundantly clear. It also those gyrations that dictate relative returns for bills, notes, and bondholders.

Current Situation

The yield curve is currently inverted by 1.47%. Ten-year investors are willing to sacrifice one and a half percent versus what they could earn in a three-month bill. They make such an investment because, in time, they believe economic growth and inflation will be slower than they are today. As such, they are comfortable locking in 3.35% for ten years and passing on the opportunity to buy bills and make more for the next few months but possibly a lot less for the next nine years.

Further, if long-term bond investors are correct, the price of notes and bonds will appreciate much more than shorter-term notes and bills. If the two-year and ten-year note rates decline by 2%, the two-year note investor could see their price rise by about 3.75%. Ten-year investors should expect a 17% gain. For more on bond math and the potential gains of losses associated with yield changes, please read our article, Treasury Bond FAQ.

Summary- The Case for Long Bonds

We think the economy and inflation will revert to pre-pandemic trends. Such means GDP and CPI will be at or below 2%. As a result, Treasury note and bond yields will likely fall to similar levels. We like locking yields well above those rates for ten or more years. If correct, we may monetize the yield decline and re-invest the funds in riskier bonds, stocks, or another asset class offering higher returns when the time is right. The timing of such a trade may not be perfect. Still, in a disinflationary and slow economic growth environment, the long-term benefits of owning notes or bonds versus bills outweigh short-term price volatility and the opportunity cost of higher bill yields for another quarter or two.

Today, the Fed risks aggravating the banking crisis and a recession because they may have already raised rates too far. It is quite possible that even if the Fed hikes rates more, notes and bonds may fall in yield. Bond investors are looking ahead and realizing the higher the Fed goes, the more crippling the effects on the economy and inflation.