Written by: Michelle Dunstan

Environmental, social and governance (ESG) ratings are a popular way to search for companies that meet specific criteria in a responsible investing agenda. But third-party ratings don’t tell the whole story for investors seeking a comprehensive view of how ESG issues affect return potential—or how companies may improve their ESG performance in future.

Creating a scoring system can help bring rigor and precision to investment analysis for asset managers across the industry. But the apparent authority of third-party ESG scores may mask their limitations. We believe third-party ESG services (such as climate data and portfolio-level ESG calculation tools) can be used as part of an investing toolkit, knowing that even as providers continue to refine their modeling and ingest more data, their ratings remain imperfect and provide only a partial solution.

In our view, there’s no substitute for integrating consideration of ESG factors into fundamental security analysis. Rather than outsource ESG assessments to third-party providers, investors and analysts must conduct in-depth, hands-on research and engage actively with issuers. That approach enables investors to achieve real insight into a business and its activities, and to get a proper understanding of its future prospects as well as its past.

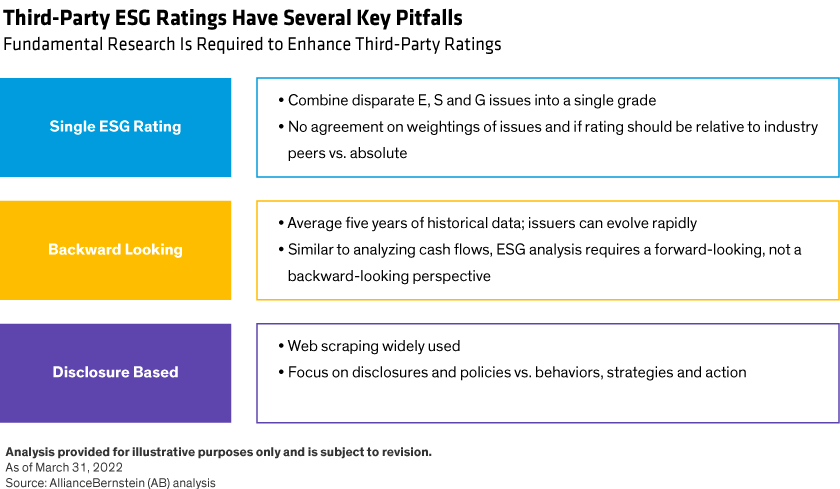

Issues with Third-Party Ratings

Today, third-party ESG ratings represent a static look in the rearview mirror: they don’t reflect a company’s potential for improvement or its vulnerability to possible future risks. These ratings rely partly on nonfinancial information that is self-reported, so scores are based on what a company says, rather than what it’s done. They also draw heavily on automated tools that extract data from websites (“web scraping”). This information may not be wholly reliable, or may even have been planted by companies together with key words that are readily recognized by search bots.

What’s more, large companies that can afford to collect and translate all the necessary data to achieve a rating tend to get awarded higher scores. And in emerging debt markets, where many companies are private, data transparency can be materially weaker than that of public companies, and coverage by ESG data providers often doesn’t exist.

Crucially, corporate ESG ratings do not necessarily measure a company’s impact on the Earth and society. Rather, some simply assess the way a company manages current ESG risks and opportunities in terms of impact on its bottom line. This rating approach focuses on whether a company is protecting its financials, as opposed to taking substantive steps to creating a greener and better world. (By contrast, ESG datapoints such as carbon metrics are already governed by independent standards like those of the Task Force on Climate-Related Financial Disclosures.)

Rating services’ coverage varies across asset classes, criteria, rigor and output. There are no current industry or regulator standards for algorithms, metrics, data sources or results. Each provider effectively has its own black box that boils massive amounts of data into a single rating per company. The result? ESG ratings can vary wildly across providers: whereas the positive correlation for credit ratings is high at 0.9, ESG rating correlations are less than 0.5.

Regulatory oversight for ESG data and ratings may be on the horizon, starting in Europe. Eurosif is studying the role of ESG ratings and data providers with an eye toward future regulations—tacit recognition of current shortcomings. European authorities are concerned because many smaller investors and passive portfolio managers rely on these ratings for their ESG insight.

We believe third-party ESG ratings are a starting point for research into existing material issues that they unearth. Greater transparency of data and scores would help providers improve their product. For example, reporting scores for each of the three ESG segments would give investors better insights than just a single ESG score.

ESG Assessments Must Look to the Future

The limitations of backward-looking ESG ratings have become clearer recently. The COVID-19 pandemic triggered urgent questions about companies’ preparedness: were they ready for the unexpected, able to adapt to ensure sustainable growth and committed to looking after their employees and customers? These are ESG issues, but they’re also financial issues.

Consider climate change. Governments are committed to a lower carbon future, which will have far-reaching impacts: it’s critical to understand how future carbon taxes or lower carbon alternatives will impact each portfolio investment.

By its nature, ESG assessment requires a forward-looking approach that static metrics may miss. What’s accepted practice today may be considered unacceptable tomorrow, as rules, regulations and popular opinion continue to evolve.

ESG Integration Drives Returns

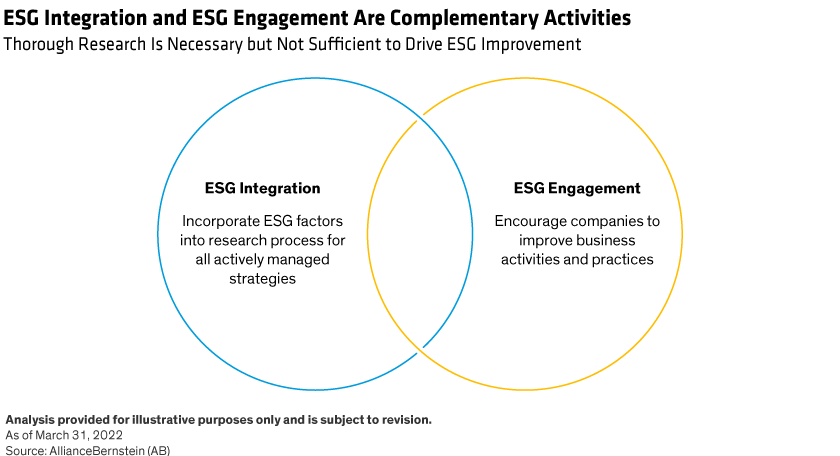

In a fast-changing world, capturing ESG benefits and identifying risks requires an integrated approach. In our view, proprietary research and industry insights are the source of alpha in investment portfolios. Similarly, we believe ESG views shouldn’t be outsourced to third-party providers since these too are a key driver of risk-adjusted returns. Our portfolio managers and fundamental analysts, who are specialists within their coverage areas, work together with responsible investing specialists to properly assess material ESG risks and opportunities in light of the company and industry affected.

Many ESG issues are current or future risks that historically haven’t been appreciated by the market. Yet, behind every high-profile corporate scandal is a catastrophic failure in understanding and managing E, S or G risks. By fully integrating ESG issues in an investment process, investors can recognize risks before making an investment—and while holding that position. This approach also helps investors identify sources of return potential in ESG leaders, for example, companies providing solutions to environmental challenges.

Engagement Is Key to ESG Assessments

Third-party ESG data and ratings are no substitute for independent fieldwork to develop a complete picture of corporate behavior. That requires engagement with management, visiting facilities and understanding the ecosystem in which a firm operates.

It also needs sufficient analyst coverage and the ability to do exhaustive fundamental homework and to validate data. Broad assumptions about industries, countries and risks can lead to suboptimal conclusions, improperly understood risks or missed opportunities. Investors that rely purely on third-party ESG data and ratings forego the opportunity to drive change, and overlook one of the key levers to improve corporate performance—engagement for action.

Companies that are behind the curve on ESG but striving to improve can present profitable opportunities—even though surface-level scores might be subpar. We’ve seen companies with poor environmental ratings make a concerted effort to upgrade to more environmentally friendly equipment. Such improvements often lead to higher ratings that boost the share price, delivering returns to investors who spot the trend early. Investing in and engaging with improvers can also lead to some of the biggest ESG benefits, for instance in carbon reduction.

Rigorous ESG assessments are too complex to be represented by a single score. Asset managers who are responsible stewards of clients’ capital have a fiduciary duty to encourage companies to improve their business activities and practices. While a third-party rating may be useful to begin a conversation with company management, it takes persistent engagement supported by in-depth research to create the conditions for a successful outcome.

Related: For Advisors, ESG Is Rich with Client Relationship Opportunities